The market has spent last eighteen months pricing Hims & Hers as a regulatory accident waiting to happen - a telehealth company making aggressive bets on compounded GLP-1 drugs while the FDA circled overhead. That thesis is now structurally broken. The March 2026 partnership with Novo Nordisk didn't just remove the overhang. It flipped the narrative entirely. Hims moved from being a disruptor fighting pharma to pharma's distribution channel.

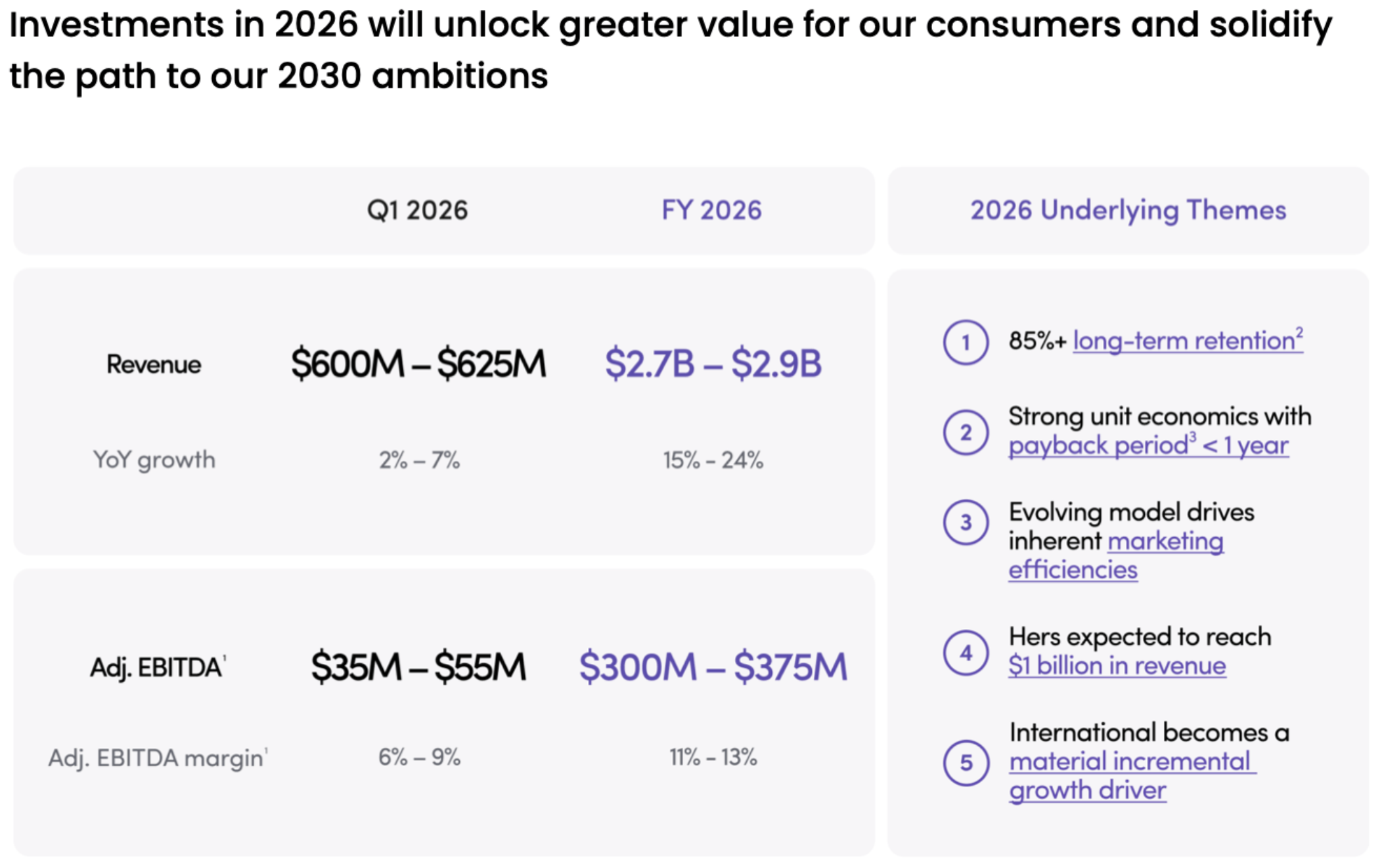

What I find most interesting is what the market still refuses to price in: a $2.35 billion revenue platform growing 59% year-over-year, with 2.5 million subscribers, $83 average monthly revenue per user, and a management team that just presented Wall Street $2.7-$2.9 billion in 2026 guidance. The stock trades at roughly 1.6x forward sales. For a company growing above 25% with visible margin expansion ahead that multiple, I do not see a premium, I see a discount.

Hims & Hers at a Glance

Andrew Dudum founded Hims & Hers in 2017 with a simple bet...that most people would rather manage their health from a phone than sit in a waiting room. Hair loss treatment was the entry point. A clean brand, affordable pricing, direct-to-consumer subscriptions. Skeptics called it a vanity play. They were wrong.

Eight years later, Hims runs one of the largest telehealth platforms in the United States. Company operates across sexual health, dermatology, mental health, weight management, hormone optimization, and - as of late 2025 - its own diagnostics lab infrastructure. It ended FY2025 with over 2.5 million subscribers and generated $2.35 billion in revenue, up 59% year-over-year. From startup to full stack platform.

But you wouldn't know that from the stock price.

What management has been saying openly, the numbers show. In latest shareholder letter, they put the FY2026 outlook front and center. Here is exactly what they guided the market to expect.

The Platform Nobody Wants to Understand

I keep coming back to one thing when I look at Hims. The market doesn't understand what this company actually is. Or maybe it does, but it's choosing not to price it.

Most analysts still categorize HIMS as a telehealth company. That was accurate in 2020. It is not in 2026. What Hims has built, while GLP-1 noise consumed every headline, is a consumer health subscription platform with expanding lifetime value and declining marginal acquisition costs. That distinction matters enormously for valuation.

Here is what I mean. A user comes to Hims for finasteride - hair loss. The acquisition cost is paid once. That user then discovers the platform offers testosterone therapy, or dermatology consultations, or mental health prescriptions, or weight management. Each additional service increases revenue per user without increasing the acquisition cost. Average monthly revenue per subscriber hit $83 in Q4 2025, up meaningfully from prior years. 65% of subscribers are now on personalized treatment plans. That is a multi-product regimens that lock in higher ARPU and lower churn.

This is brand new healthcare company, much closer to a subscription-based consumer platform with healthcare as the vertical. Think of it this way: Netflix acquired you for one show, then kept you for the library. Hims acquires you for one condition, then keeps you for the platform.

"Over 65% of our subscribers are now on personalized solutions. These are multi-condition, multi-product treatment plans that drive significantly higher lifetime value and meaningfully lower churn rates."

- Andrew Dudum, CEO, Q4 2025 Earnings Call (Feb 23, 2026)Core Health Categories

Weight Management

Emerging Verticals

What CEO Andrew Dudum described at the Morgan Stanley TMT Conference in March 2026 is a company that selects new categories with surgical precision. Criteria? The condition must be chronic (recurring revenue), underserved by the existing healthcare system (demand pull), and treatable through a combination of telehealth and pharmacy fulfillment (operational leverage). Every new vertical that meets these criteria expands the platform without expanding the cost base proportionally.

2030 targets tell the story management is building toward: $6.5 billion in revenue, $1.3 billion in adjusted EBITDA, and a 20% EBITDA margin. Those are ambitious numbers. But they are not fantasy, they are math. If ARPU continues rising and subscriber growth holds in the mid-teens, compounding does the work.

The Novo Nordisk Pivot - From Adversary to Ally

Let me be direct with you. The Novo Nordisk partnership is the single most important event in the history of this company. Not just because of the immediate revenue impact, that will take quarters to fully materialize. But mainly because it fundamentally changes what kind of company Hims is.

For the last year, conversation around HIMS has been dominated by one question: can this company survive the regulatory crackdown on compounded GLP-1 drugs? FDA was circling. Novo Nordisk had filed lawsuits. Compounding pharmacies that supplied Hims with semaglutide were operating in a gray zone that could close at any moment. It was, frankly, the most legitimate bear case against the stock.

That bear case is now dead.

In March 2026, Hims and Novo Nordisk announced a partnership under which Hims will become an authorized distributor of branded Wegovy and Ozempic. Lawsuits were dropped. The compounded products will be discontinued. Hims transitions from a regulatory target to a pharmaceutical distribution partner.

Stock moved 40% in a single session. That tells you how much overhang was embedded in the price.

But here is what I think most people are missing. Financial impact of this deal is secondary to the psychological and strategic impact. Why would Novo Nordisk - a $400 billion pharmaceutical company - partner with a firm it was actively suing? Answer is simple: because Hims has something Novo wants. Distribution. Access. A direct-to-consumer platform with 2.5 million engaged health subscribers.

Novo isn't doing Hims a favor. Novo is solving its own problem. GLP-1 demand is supply-constrained, and Novo needs every distribution channel it can get. Hims offers something traditional pharmacy chains don't...a digitally native customer base that is already engaged in health management, already providing data, already subscribing monthly.

Margin profile changes, yes. Distributing branded Wegovy is less profitable per unit than selling compounded semaglutide. But trade-off is sustainability over margin. A regulatory-proof revenue stream replacing a regulatory-fragile one. For a long-term investor, that is the right trade every single time.

"This partnership represents the natural evolution of our platform. We built the consumer relationship, the clinical infrastructure, and the fulfillment capability. Now we're pairing that with the world's leading branded GLP-1 therapies."

- Andrew Dudum, CEO, on the Novo Nordisk Partnership Announcement (March 2026)Important Disclaimer

This content is for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy, sell, or hold any security. All investments carry risk, including the potential loss of principal. Past performance does not guarantee future results. The scenarios, price targets, and probabilities presented reflect the author's analysis and opinion at the time of publication and are subject to change without notice. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Bellwether Research and its contributors may hold positions in the securities discussed.