Two data events in the same week can do remarkable damage to a stock, especially when the narrative around that stock was already stretched. First came the bone mineral density scare: a Cantor Fitzgerald analyst flagging a 4% BMD decline from Phase I data published eight months earlier, data that Amgen's own management had previously acknowledged and dismissed. Then came the Phase II MariTide readout itself, up to 20% average weight loss at 52 weeks, a genuinely impressive clinical result that the Street had nonetheless priced for something bigger. AMGN fell nearly 20% from its 2024 highs. The market delivered its verdict swiftly.

But markets often get the sentiment right and the analysis wrong. At $XXX–$XXX, you are buying a company generating $8.5 billion in quarterly revenue, growing 23% year-over-year, with 33% net margins, 12 consecutive years of dividend increases, and a forward P/E of 14.3x. The GLP-1 option value is free. The question is not whether MariTide will be perfect. The question is whether the bar for "good enough to compete" in a market where Eli Lilly and Novo Nordisk together command $1.18 trillion in combined market cap is actually as high as the current share price implies.

This note walks through the core business Amgen has quietly been building, the Phase II data without the noise of the stock price reaction, the structural dynamics of a market large enough to absorb multiple winners, and the scenarios that define this position's risk-reward. The thesis is not that MariTide will win. The thesis is that Amgen wins even in most of the losing scenarios, and the upside of even partial success has not been captured in the current price.

The Core Machine: What 23% Growth Actually Looks Like

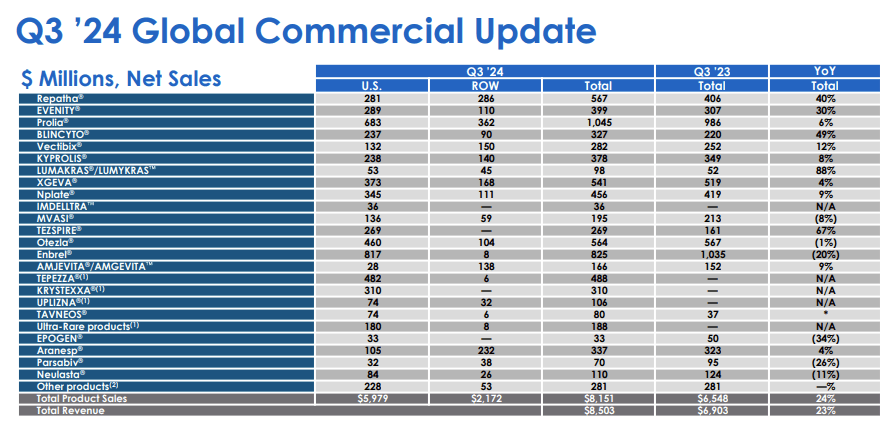

The noise around MariTide has obscured something important: Amgen's underlying commercial franchise is performing at a level few of its peers can match. In Q3 2024, total revenues hit $8.5 billion, up 23% year-over-year. Ten drugs posted double-digit sales growth in that single quarter. This is not a company running on fumes while it waits for a pipeline win.

The growth engine has several distinct components. Repatha, the PCSK9 inhibitor for cardiovascular risk, grew 25% year-over-year in Q3 driven by 46% volume expansion, partially offset by lower net prices under managed care agreements. Evenity, the bone-building drug for osteoporosis, grew 39%. Blincyto, the leukemia treatment and the clearest example of Amgen's BiTE antibody platform delivering, grew 28%. Tezspire, the anti-TSLP biologic developed with AstraZeneca for severe asthma, grew 76% year-over-year to $234 million in a single quarter. These are not rounding errors in a financial model. They represent genuine volume growth across multiple therapeutic areas.

The Horizon Therapeutics acquisition, completed in October 2023 for approximately $28 billion, is also beginning to show its strategic value. Horizon products added $1.1 billion in revenue for Q3 alone. Tepezza, the thyroid eye disease drug, grew 8% year-over-year with a Japan launch targeting early 2025. Krystexxa for uncontrolled gout generated $294 million. Tavneos, which Amgen acquired separately through ChemoCentryx, grew 137% year-over-year, and the number of patients prescribed it has more than doubled since the acquisition. The integration has gone well, and what looked to some analysts like an expensive empire-building exercise is proving its commercial logic.

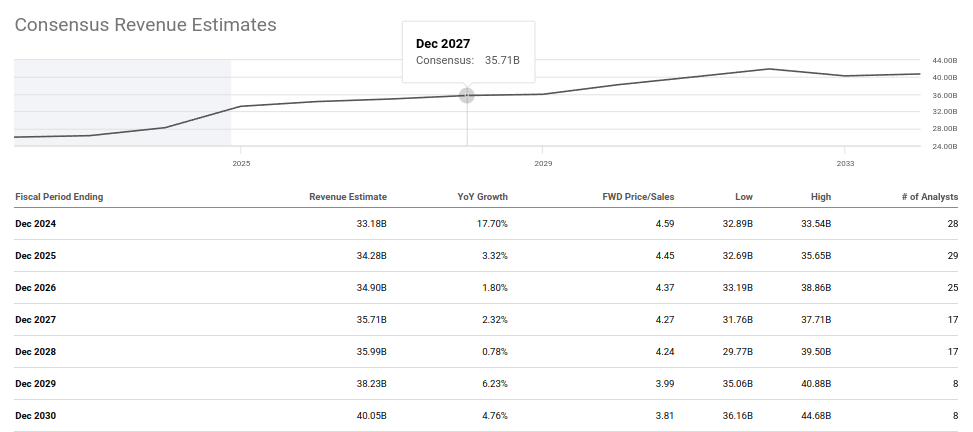

Looking at the forward picture, consensus estimates project revenues growing from $33.18 billion in 2024 to $40.05 billion by 2030. That 20.7% revenue growth is expected to translate into 43.6% EPS expansion, from $19.57 per share to $28.10 per share, because of operating leverage and Amgen's sustained share buyback program. The share count has already been reduced 25.7% between 2017 and 2023, from 720.6 million shares to 535.9 million. That trajectory, if continued, means EPS growth will almost certainly outpace the consensus model.

The critical observation here is that these consensus revenue estimates were built largely before MariTide was a serious commercial factor. They model organic growth from the existing portfolio. That means the $33B-to-$40B trajectory represents a floor, not a ceiling. A successful MariTide adds on top. An unsuccessful MariTide leaves the model largely unchanged. At 14.3x forward earnings, even the floor looks undervalued.

Reading MariTide Phase II Without the Stock Price

The standard advice in clinical-stage investing is to analyze data before looking at the stock price reaction. In practice, almost nobody does this. The price is there, it moved violently, and it shapes how every subsequent data point is processed. Let me try to do the exercise properly.

MariTide (maridebart cafraglutide, AMG 133) is a novel bispecific molecule that works via two distinct mechanisms: it activates the GLP-1 receptor, the same target as semaglutide and tirzepatide, and it simultaneously inhibits the GIP receptor (GIPR). The genetic rationale for the GIPR inhibition is that people with naturally reduced GIPR signaling show protection against obesity and related metabolic conditions. This dual mechanism is what Amgen has consistently presented as MariTide's differentiation: not just a "me-too" GLP-1 agonist, but a fundamentally different intervention in the obesity biology.

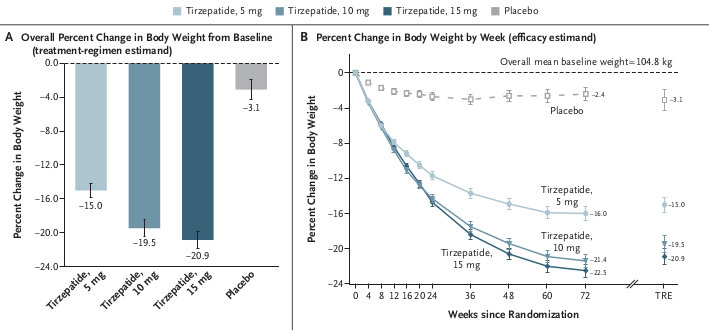

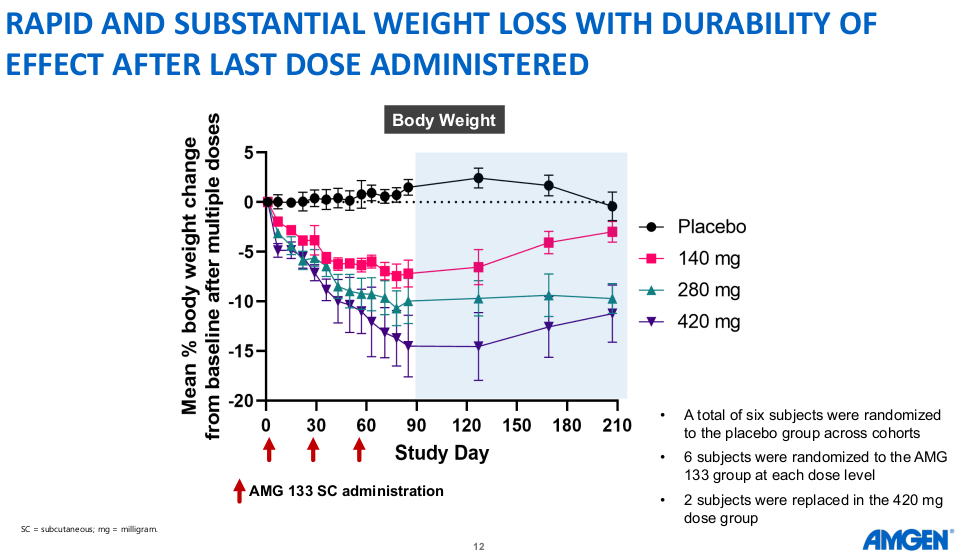

The Phase II study enrolled 592 participants in total, with 465 in the obesity cohort. Patients were divided across dose arms of 140mg, 280mg, and 420mg, administered monthly via subcutaneous injection, against a placebo arm. The key efficacy result: up to 20% average weight loss at 52 weeks, without a plateau.

The "disappointment" narrative requires a benchmark. The most relevant comparison is tirzepatide (Zepbound/Mounjaro), Eli Lilly's current standard-bearer, whose Phase III SURMOUNT-1 trial reported 20.9% weight loss at 72 weeks for the highest dose. MariTide delivered 20% at 52 weeks. That is 20 fewer weeks of treatment. An apples-to-apples comparison, extrapolating the MariTide curve to 72 weeks without a plateau, would put MariTide in a directly competitive weight-loss range with tirzepatide, somewhere in the 22% to 23% territory.

A one-year study stopping before the curve plateaus is a structural advantage for the Phase III narrative, not a weakness. Ninety percent of Phase II patients elected to continue for a second year. That is not the behavior of patients experiencing unacceptable side effects or unsatisfying weight loss. That is a retention signal.

This trajectory was not a surprise to Amgen's team. Phase I repeated-dosing data had already shown a consistent downward weight curve with no sign of flattening at the final measured time-point. That early kinetic profile is what informed the Phase II design decision to run the trial to 52 weeks rather than a shorter window, and it is precisely why the absence of a plateau in Phase II carries such weight: the same pattern was visible from the very first human dosing studies.

On safety, three specific concerns dominated the market reaction and are worth addressing individually.

Bone mineral density: The Cantor Fitzgerald analyst raised this based on Phase I data published in February showing a 4% BMD decline at the highest dose. The Phase II data definitively resolved this: no adverse impacts on bone mineral density were observed in the 52-week trial. The concern was a false alarm based on preliminary data.

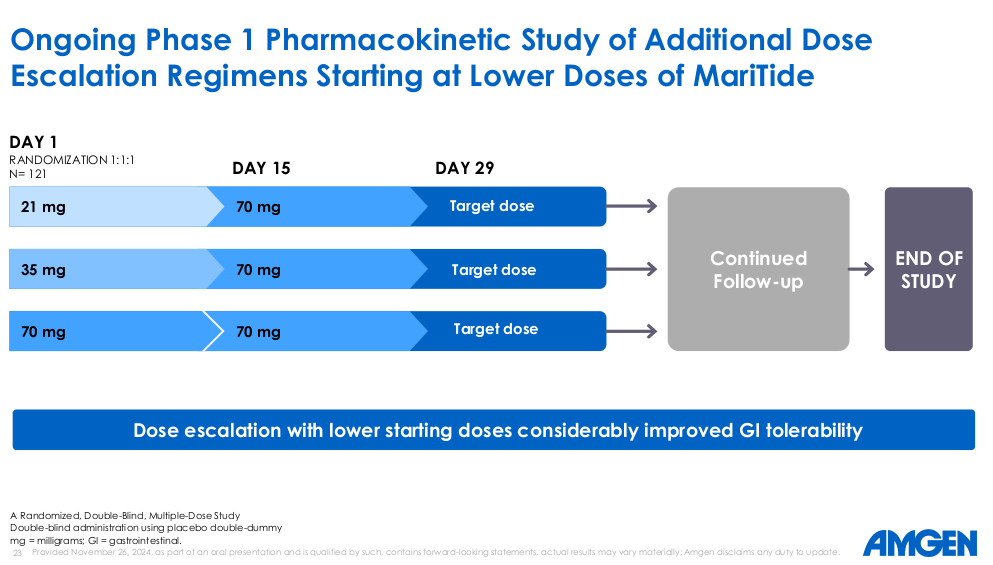

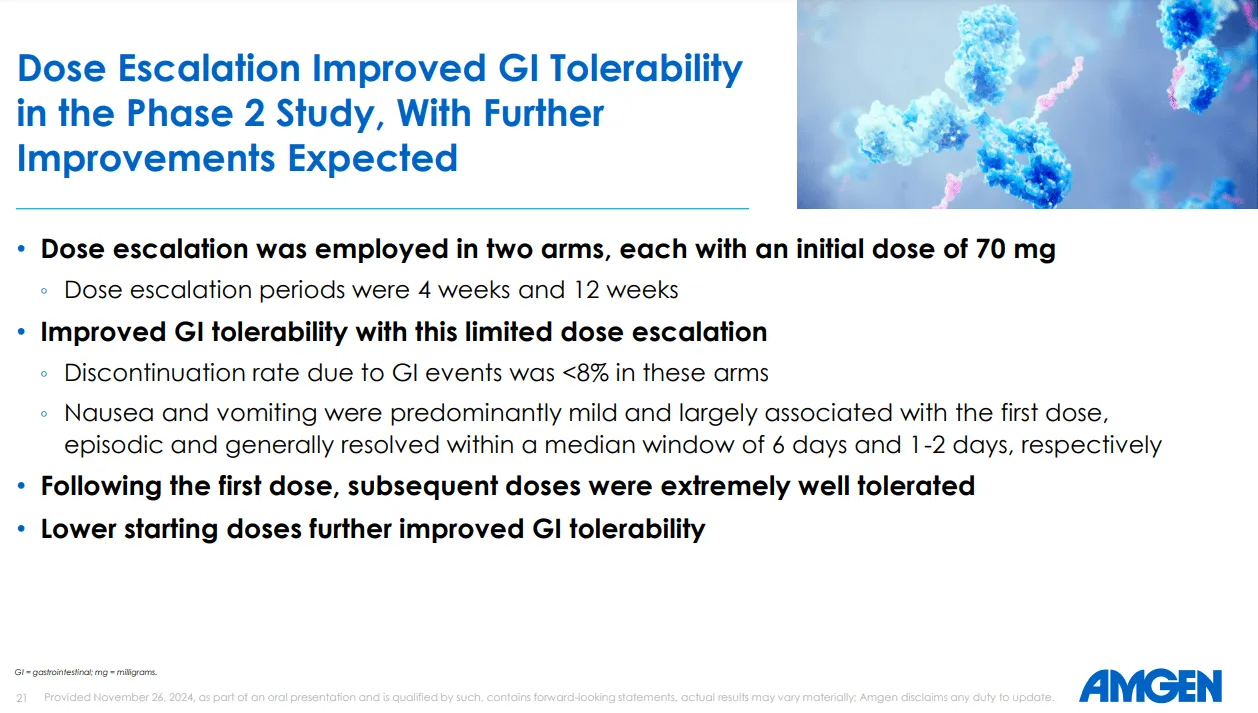

GI side effects: The discontinuation rate in dose-escalation arms was approximately 11% for any adverse event, with less than 8% for GI-specific events. This compares unfavorably to tirzepatide's Phase III, where the highest discontinuation rate for adverse events was 7.1%. However, context matters. In the MariTide arms employing an escalation strategy starting from 70mg, nausea rates fell below 50% and vomiting below 20% by day 43. More importantly, 90% of patients completing the year elected to continue. Amgen explicitly states that GI events were "predominantly mild to moderate, transient, and primarily associated with the first dose" and that "subsequent doses were extremely well tolerated."

Discontinuation rate uncertainty: The market reacted negatively to limited data granularity around which patients discontinued and at which dose. The intriguing observation is that the 280mg cohort showed comparable or slightly superior efficacy to the 420mg cohort. This raises the possibility that the FDA-approved dose in Phase III may not be 420mg at all, which would naturally improve the safety profile while preserving the efficacy. The dose escalation strategies being explored are compelling and suggest Amgen's team is thinking clearly about the commercial rollout.

The conclusion from a cold reading of the Phase II data: this is not a drug in trouble. This is a drug that showed competitive weight loss efficacy at half the duration of the benchmark, maintained a 90% continuation rate, resolved its bone density concern, and has a clearly identifiable tolerability strategy for Phase III. One analyst, who covered MariTide Phase I closely, raised his estimated probability of MariTide becoming a commercial drug from 60% to approximately 80% following Phase II. That upward revision after the data that "disappointed" the market is worth pausing on.

"We are fully confident that MariTide's differentiated profile can contribute meaningfully to addressing the epidemic of obesity, the burden of type 2 diabetes, and other serious obesity-related conditions."

Jay Bradner, Executive VP of R&D and Chief Scientific Officer, Amgen - Phase II Update, November 26, 2024The Obesity Race: Why the Market Is Large Enough for a Third Player

The framing of GLP-1 as a winner-take-all competition is a narrative convenience, not a medical reality. Consider how the precedents actually played out in comparable market categories. Statins did not produce one winner. Antihypertensives did not produce one winner. Biologics for rheumatoid arthritis, where Humira, Enbrel, Remicade, and Xeljanz all coexisted at multi-billion-dollar scale, is perhaps the most instructive parallel. The obesity market at $500 billion-plus in addressable potential by the end of the decade is not a niche. It is an expansion of a metabolic disease category that will require multiple treatment approaches, patient populations with different tolerability profiles, and healthcare systems with different reimbursement frameworks.

Where specifically does MariTide compete? The dosing frequency argument is compelling and underappreciated. Both semaglutide and tirzepatide are administered weekly. GLP-1 users have high discontinuation rates in the real world, often 30% to 50% within the first year of treatment, particularly because the weekly injection routine combined with persistent GI side effects creates patient fatigue. Monthly dosing, or even quarterly dosing (which Amgen is exploring in a Phase II sub-study), is not just a convenience feature. It is a fundamental change in the patient experience that could drive materially higher adherence rates in a market where adherence is currently the biggest commercial risk for existing products.

The manufacturing angle is also worth taking seriously. Lilly and Novo Nordisk have both faced significant supply shortages of Zepbound and Ozempic/Wegovy. These shortages are structural: tirzepatide and semaglutide are peptide-based medicines that require specialized manufacturing capacity with long lead times. MariTide, by contrast, is built on a monoclonal antibody backbone that fits directly into Amgen's existing manufacturing network. Amgen's CFO Peter Griffith flagged this explicitly on the Q3 call: "yield is really important, and we've got a really strong history in that." The R&D budget is being stretched to prepare: Q3 R&D spend was up 35% versus the prior year quarter, and up over 25% for full-year 2024. The Phase III MARITIME program has been launched, and Amgen is investing at scale to be ready.

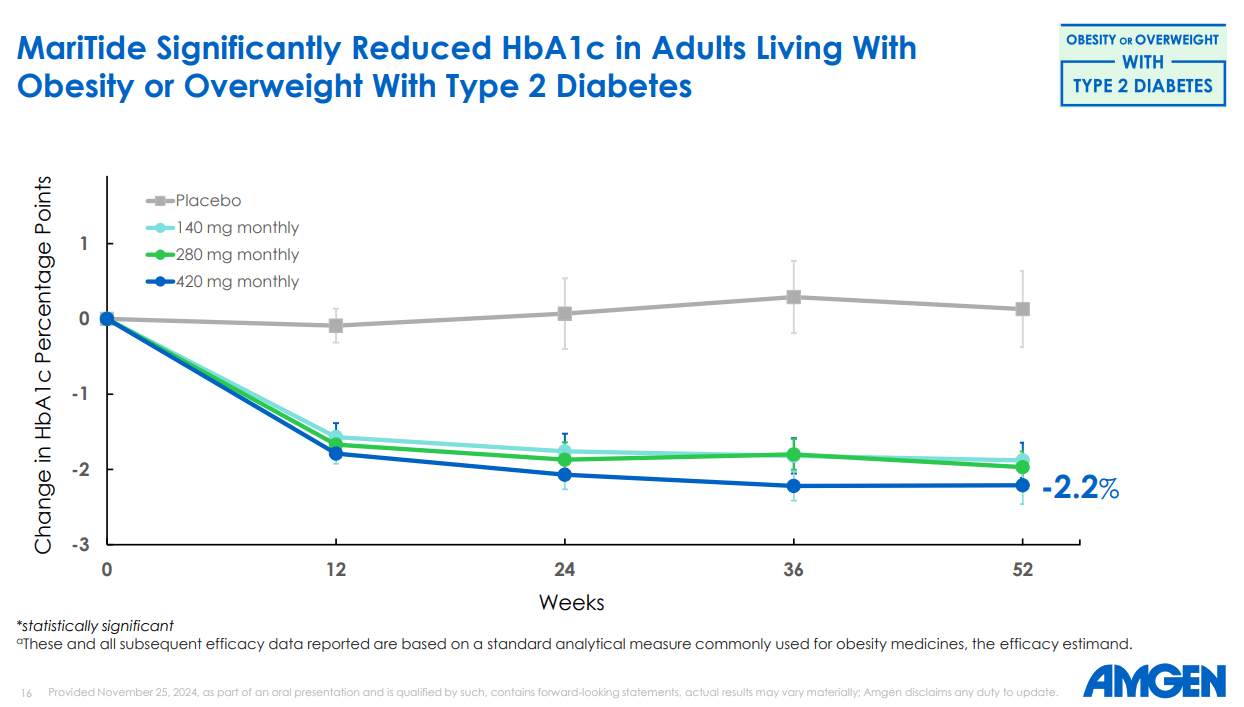

Then there is the type 2 diabetes angle, which most market commentary has underweighted. In the T2D cohort of the Phase II study, MariTide delivered 17% weight loss at 52 weeks alongside a 2.2 percentage point reduction in HbA1c, clinically meaningful improvements in systolic blood pressure, triglycerides, and hs-CRP. The HbA1c reduction is within the range of what CagriSema, Novo Nordisk's next-generation candidate, achieved in its Phase II. And MariTide has a monthly dosing advantage there too. As Susan Sweeney, Amgen's Executive VP of Obesity, put it on the Phase II call: MariTide has "the potential to be the first and only monthly treatment option" for type 2 diabetes, "a long-standing goal in the field."

Morningstar estimated MariTide's addressable market at $8 billion annually by 2033, with a 60% approval probability before the Phase II data. With Phase II having confirmed competitive efficacy and resolved the bone density concern, that probability estimate has moved upward. Zooming out to the broader obesity treatment landscape - estimated to reach $500 billion annually at full market maturity - even a 5% share would represent approximately $25 billion in annual revenue within a decade, against Amgen's current total annual revenue of $33 billion. Partial success in GLP-1 changes the company's growth trajectory irreversibly.