There is a version of this story that most analysts missed - not because the data wasn't there, but because it required sitting with an uncomfortable truth: the EQT you're looking at today is not the company it was eighteen months ago. The Equitrans acquisition, closed in July 2024, was not just a midstream bolt-on. It was a structural transformation that collapsed gathering costs from $0.58 to $0.09 per Mcfe in a single quarter, dropped the company's unlevered breakeven to $2.03/Mcfe (the Q4 2024 unlevered cash operating cost - EQT's purest measure of production efficiency, excluding interest and midstream capital), and created the only vertically integrated dry-gas producer in the Appalachian basin with preferential access to its own takeaway pipe - the Mountain Valley Pipeline. A note on breakeven metrics used throughout this tip: EQT reports several distinct breakeven figures. The unlevered cash cost ($2.03/Mcfe) reflects pure operating efficiency for Q4; the unlevered maintenance breakeven ($2.08/Mcfe) is the full-year 2025 equivalent on a maintenance free cash flow basis; the all-in free cash flow breakeven ($2.28/Mcfe) incorporates interest expense and sustaining capex for the full year; and the Q4 all-in FCF breakeven ($2.43/Mcfe) is the most conservative single-quarter measure. Each figure is labelled at its point of use below.

Since that acquisition closed, EQT has rallied 37.6% - outperforming the XOP (S&P Oil & Gas E&P ETF) by over 43 percentage points. That kind of spread between a single name and its sector benchmark doesn't happen on sentiment alone. It happens when the fundamentals are moving faster than the consensus can update its models. And yet, even after that move, EQT remains roughly the 360th largest S&P 500 component by market cap. Under the radar. Below institutional allocation thresholds. Priced like a commodity producer in a world where it has quietly become something closer to a vertically integrated infrastructure-plus-production platform.

This note lays out why I think the market hasn't fully re-rated EQT's cost profile yet, and why the combination of free cash flow, rapid deleveraging, differentiated well performance, an innovative Blackstone midstream structure, and an improving gas backdrop makes this one of the cleaner asymmetric setups in energy right now. Entry $XX-$XX. Target $XX-$XX over 9-12 months.

In the commodity business, people talk about price. But the producers who survive across full cycles - and who generate real shareholder value - are the ones obsessed with cost. It is a game of pennies. It does not take too many additional pennies saved per unit of production to begin to materially outperform the industry, and conversely, a few pennies too many can make the difference between profitability and losses in a downturn.

When EQT completed the Equitrans acquisition, it did something that doesn't happen often in commodity businesses: it fundamentally changed what it costs to produce a unit of gas, not by squeezing on the margin, but by removing an entire cost layer from the P&L. Before the deal, EQT paid Equitrans - as an external midstream operator - gathering fees of $0.58 per Mcfe. These flowed out of EQT's income statement as cash costs every quarter, regardless of where gas prices were. After the acquisition, that gathering charge effectively becomes an intra-company transfer. The cost plummeted to $0.09 per Mcfe - a reduction of 84% in a single line item. The residual $0.09/Mcfe represents third-party interconnect fees and state-regulated pipeline tariffs that persist even within the consolidated structure - costs that cannot be eliminated through vertical integration alone. The commercially controllable gathering spread has been internalised; only the regulatory floor remains.

For a company producing over 2,200 Bcfe a year, that is roughly $1.1 billion in annual savings that the market is still digesting. And unlike a one-time efficiency programme or a hedging gain that washes out next quarter, this is structural. The midstream is now inside the company. The gathering cost doesn't come back. What the Equitrans integration did was permanently lower the floor under EQT's economics - and the proof showed up immediately in the operating data.

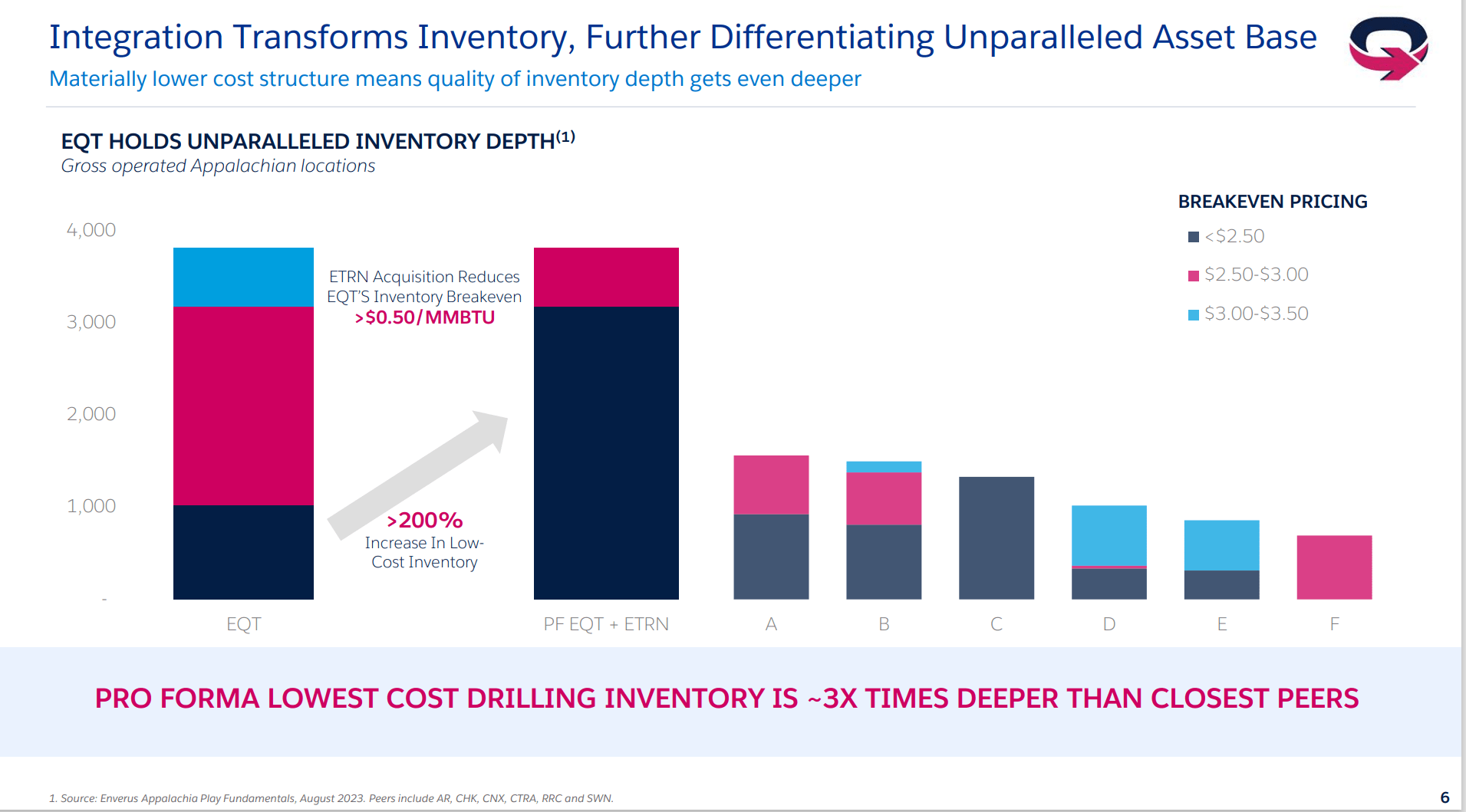

The inventory chart above makes the structural case visually. EQT + Equitrans has moved more than 3,000 locations into the sub-$2.50 breakeven tier - roughly three times the depth of its closest Appalachian peer. That is not just a current-quarter advantage. It defines EQT's cost position for the next decade of drilling. The pro forma low-cost inventory is approximately three times deeper than any competitor in the basin - Antero Resources, CNX Resources, Coterra Energy, Range Resources - none come close. And this depth of inventory at this breakeven means EQT can maintain production levels and generate free cash flow even in price environments that would force peers into curtailment.

There is a subtlety here worth emphasising. The integration didn't just lower gathering costs. It gave EQT operational control over the entire midstream network that connects its wells to market. That means the upstream and midstream operations can be coordinated to maximise joint profitability - something that was never possible when the gathering system was run by a separate public company with its own shareholders and incentives. As one analyst observed, the midstream may turn out to be "unusually profitable" precisely because of this close coordination - an outcome that independent midstream operators, by structural design, cannot replicate.

One thing I look for in an operator is whether results tell the same story as management's tone. In EQT's case, Q4 2024 was consistent in both: the company beat guidance across essentially every line item, and the nature of the beat was operationally genuine rather than accounting-driven. This is a management team - the Rice Brothers, who won the proxy fight and took control - that has developed a pattern of under-promising and over-delivering. It's not a coincidence. It's a strategy.

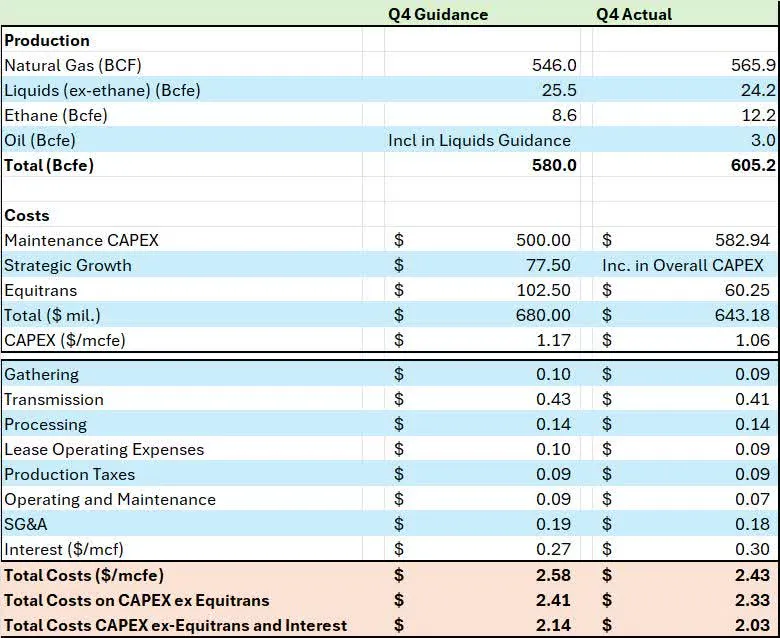

Production came in at 605.2 Bcfe against a guidance midpoint of 580 - above even the top of the guidance range. Natural gas alone was 565.9 BCF versus 546 BCF guided. Management attributed the entire beat to operational efficiency and strong well performance, not pulled-forward well timing. Capital intensity dropped to $1.06/Mcfe versus the $1.17 guidance midpoint. The result: an all-in free cash flow breakeven of $2.43/Mcfe (Q4 all-in FCF breakeven - the most conservative measure, including interest and sustaining capex), meaningfully better than the $2.58 flagged just three months prior. The unlevered breakeven excluding Equitrans came in at $2.03/Mcfe (Q4 unlevered cash operating cost) versus $2.14 guided - one of the lowest breakeven cost structures of any natural gas E&P operating in the United States today.

The per-unit cost table is where the full story hides. Walk through the line items:

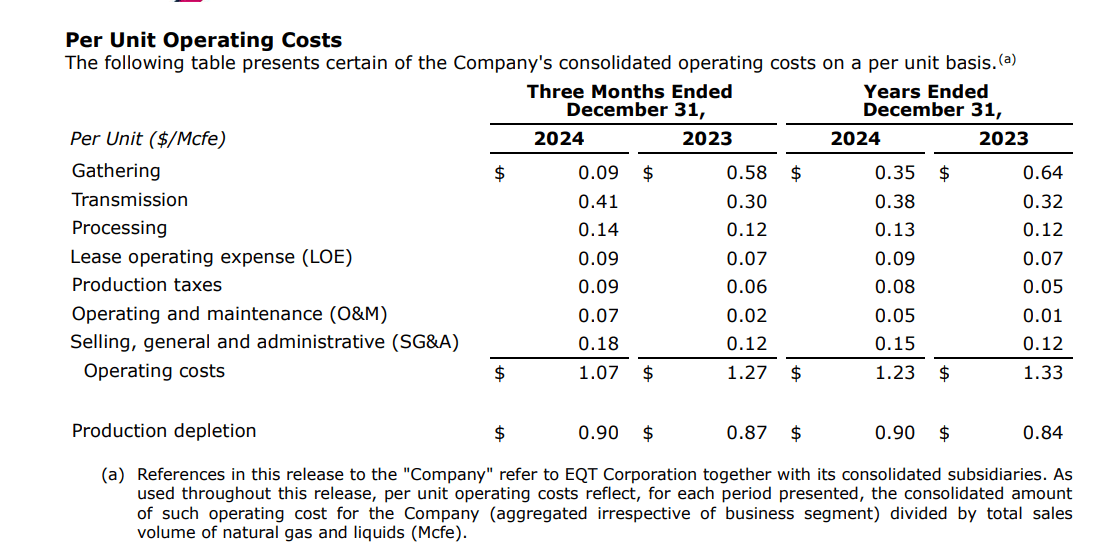

Walk through the line items and the story becomes clear. Gathering: $0.58 down to $0.09 - the Equitrans effect. Processing: $0.12 to $0.14 - essentially flat. LOE: $0.07 to $0.09 - marginal increase. Production taxes: $0.06 to $0.09 - higher because realised prices were higher (a good problem). SG&A: $0.12 to $0.18 - the only meaningful increase, reflecting the larger combined entity's overhead. The one number bears point to is transmission, which rose from $0.30 to $0.41/Mcfe - a direct consequence of the Mountain Valley Pipeline ramp. That increase is real, but it is also the cost of accessing premium pricing at the Gulf Coast rather than selling at depressed in-basin rates. It's a cost that pays for itself through better realisations.

The cash flow statement tells the operational story even more directly. Q4 free cash flow came in at $580 million - up from $229 million in Q4 2023. Full-year adjusted operating cash flow was $3.1 billion versus $2.8 billion the prior year, despite 2024 including hundreds of millions in one-time merger transaction costs. Strip out those merger costs and the underlying cash generation machine is running well above what the stock price implies.

The average realised price in Q4 2024 was $3.01/MCF - well above the depressed levels of the prior year. With EQT's Q4 all-in FCF breakeven at $2.43/Mcfe (the most conservative measure, including interest and sustaining capex), every incremental dollar of gas price above breakeven flows almost entirely to free cash flow. That is the definition of operating leverage.