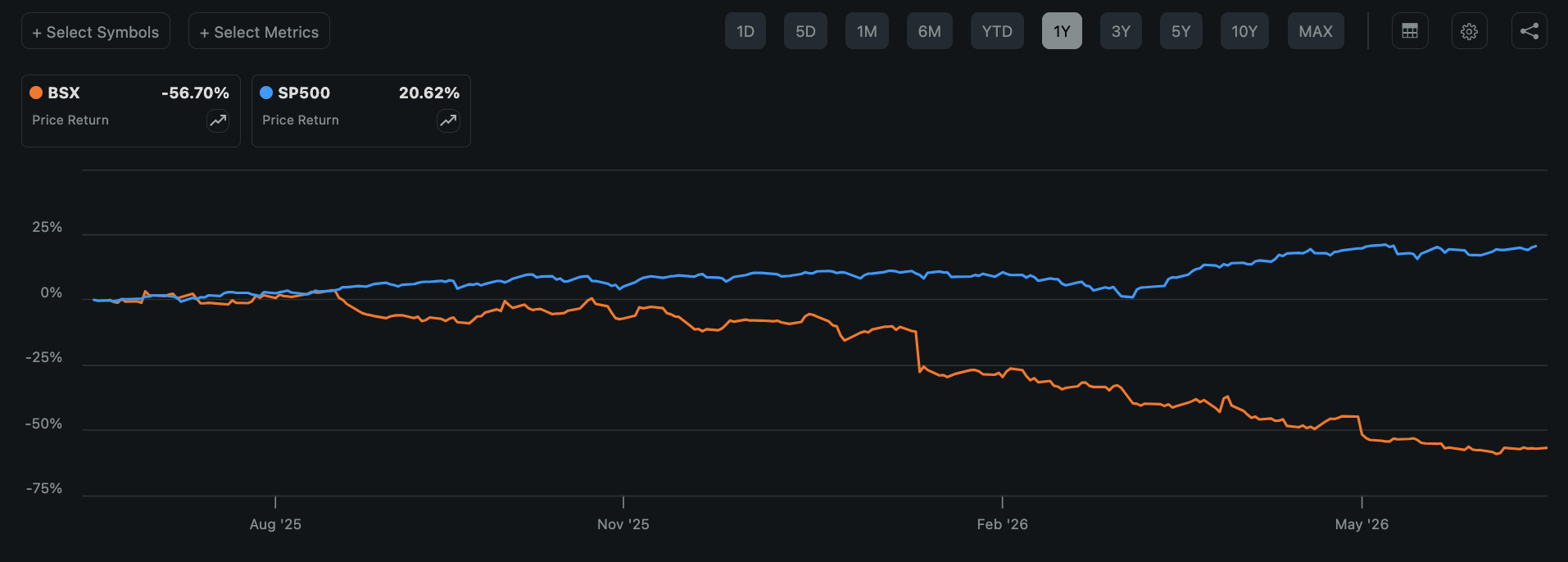

Boston Scientific spent a decade earning a premium. It was a medtech that grew mid-teens, expanded margins, and beat its guide every single quarter. Investors paid roughly thirty times forward earnings for that reliability. For years it showed up. Then, on February 4th, management guided 2026 below plan. On April 22nd it cut guidance again. In five months a $109.50 stock became a $43 stock, a decline of more than 60% in a year S&P 500 rose more than twenty percent. Wall Street decided a great compounder was suddenly finished.

Set the sentiment aside and weigh the actual change. Full-year adjusted EPS guidance moved from $3.43-$3.49 to $3.34-$3.41, a cut of about two and a half percent. Organic growth guidance came down from 10-11% to 6.5-8%, a genuine slowdown, yet management still expects double-digit adjusted EPS growth, 50-75 basis points of margin expansion, and roughly $4 billion of free cash flow this year. A business earning 70.5% gross margins, converting nine cents on every dollar into cash, and compounding earnings at ten percent does not deserve to lose more than half its multiple. Earnings barely moved. Sentiment collapsed. That mismatch is the whole idea.

So markets price a broken machine while the machine keeps running. At the lower band of the entry zone you pay about twelve times this year's earnings and under eleven times next year's, cheapest quality large-cap in the entire device group, below Medtronic and Abbott, two-thirds of Stryker's multiple and about half of Edwards', for a business that has out-grown all of them over five years. People closest to it are voting with capital: board authorized $5 billion of buybacks and is deploying $2 billion now, a director bought shares personally near $57, and Steve Cohen's Point72 raised its position by half while trimming Nvidia and Amazon. Every sell-side desk still rates it a Buy, even the bears.

Two things have to be true for this to work. I will argue both. First, this guidance cut is trough of the news, not a first step down. Easier back-half comparisons plus a deep 2027 launch cadence let growth stabilize. Second, chart is no longer a falling knife but a base: on the weekly frame BSX sits on a shelf that capped it for years, momentum at multi-year exhaustion, with recent months looking like accumulation rather than distribution. You are buying a double-digit compounder at a mid-single-digit multiple discount to its own history, into a technical bottom, while insiders buy alongside you. That is the trade.

What Boston Scientific Actually Is

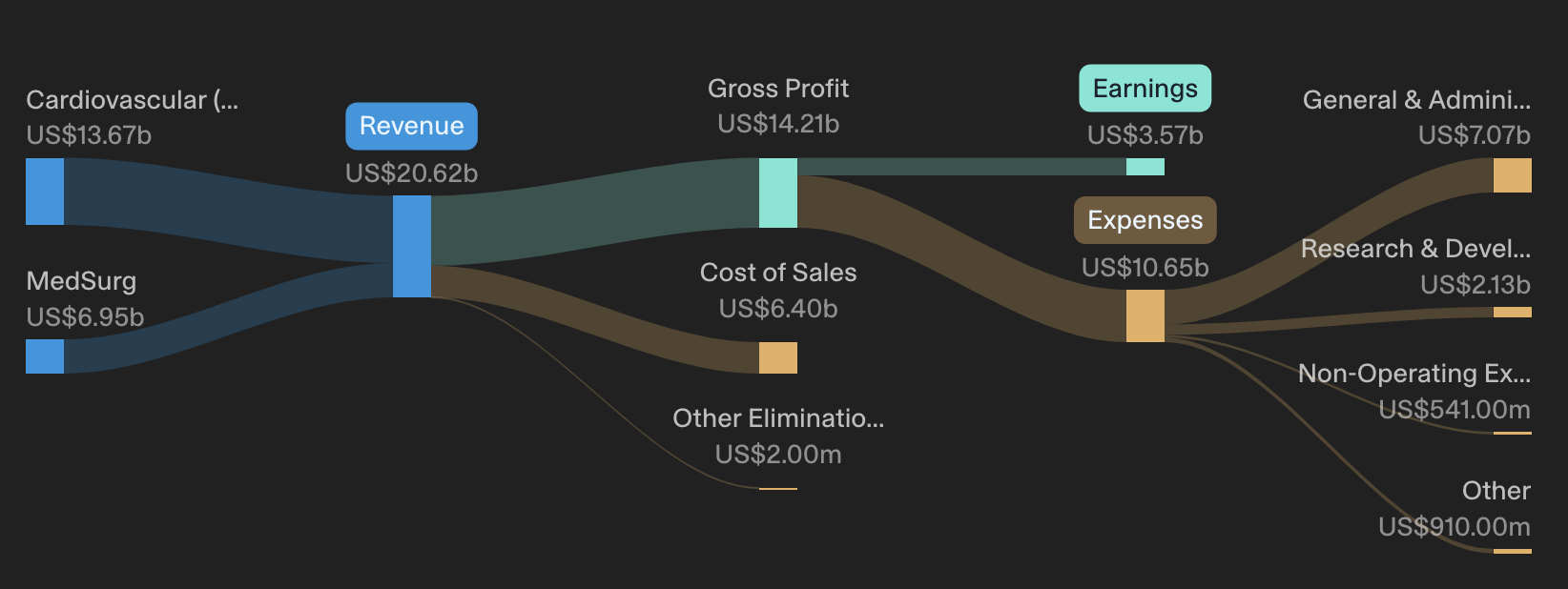

Before the fall, the company. Founded in 1979 and run since 2011 by Mike Mahoney, Boston Scientific is a $20 billion-a-year maker of the tools interventional physicians reach for when they would rather not cut a patient open. It reports in two segments. Cardiovascular, about 67% of revenue, spans interventional cardiology, structural heart, electrophysiology, cardiac rhythm management, and interventional oncology. MedSurg, the other 33%, covers endoscopy, urology, and neuromodulation. Geographically it is 64% United States, 17% Europe-Middle East-Africa, 15% Asia-Pacific, and the balance in Latin America, so revenue rides global procedure volumes rather than any one payer system.

What holds that portfolio together is a flywheel most rivals cannot copy - clinical evidence, physician relationships, and relentless tuck-in M&A. This is a company that runs large randomized trials, publishes them in the New England Journal of Medicine, and uses that data to move products from niche to standard of care. It buys adjacent innovators (Axonics in incontinence, Nalu in pain, Valencia's eCoin this quarter) and plugs them into a distribution machine already sitting in tens of thousands of cath labs and operating rooms. Its footprint is deliberately global, too: R&D hubs in Shanghai, Gurugram, Heredia and Galway, physician-training institutes across several continents, and manufacturing anchored by a large Penang site, with roughly twenty targeted emerging markets a standing growth vector, on display this quarter as Asia-Pacific grew 12% behind Japan and China. Five-year revenue compound growth of 15.1% dwarfs Medtronic's 4.9% and Edwards' 6.7%; three-year free-cash-flow growth of 41% dwarfs both. A slower 2026 does not un-build that engine. It only resets the price you pay to own it.

Keep two facts from this section in mind as the rest unfolds. Margins are elite...70.5% adjusted gross, 28% adjusted operating, among the best in devices. And growth, even after being marked down, still runs well ahead of the peer group. Hold onto both. Everything that follows is an argument that a business with those two properties has been priced as though it had neither.

Metrics at a Glance

Read that dashboard as a clinician reads a monitor: no single number is alarming. Several are enviable. A 70.5% gross margin and a 28% operating margin sit in the top tier of device makers. Roughly $4 billion of free cash flow against a $63.7 billion market value is a 6% cash yield, unusual for a business still filed under "growth." Leverage of 1.8x with interest covered more than twelve times over is not a balance sheet under strain. Nothing here reads like a company in structural decline.

One line does the damage. It is the smallest change on the page. Adjusted EPS guidance came down about two and a half percent, from a $3.46 midpoint to $3.375. Against that, shares lost more than half their value and shed roughly a hundred billion dollars of market capitalization from the 2025 peak. When a price reaction runs twenty times the size of an estimate revision, the move is about the multiple investors will pay, not the earnings they expect to receive. That distinction is what this study takes apart, across the next three sections...what slowed, how it fell, and why the fall overshot.

Three Culprits, Read Honestly

Mahoney named three drivers of the guide-down without hedging: WATCHMAN, electrophysiology, and urology. A thesis that only quotes the bull case is worthless, so let me take each on its own terms, including where a bear has a real point.

WATCHMAN. Boston Scientific's left-atrial-appendage-closure device reduces stroke risk in atrial-fibrillation patients. It grew almost 30% in 2025. In Q1'26 it grew 19%, below plan, with softness appearing abruptly in mid-February. Underneath that headline is a nuance that matters: demand for the "concomitant" procedure, where WATCHMAN goes in at the same time as an ablation, is strong and growing, while standalone cases decelerated as referrals shifted toward electrophysiologists, hospital capacity tightened, and a reimbursement change bit. Roughly 25% of WATCHMAN cases are concomitant today; management expects 50% over the plan. Read honestly, mix is shifting faster than expected and the standalone leg stalled; the addressable market did not shrink. About five million patients are indicated today. CHAMPION-AF, which hit every endpoint, is the lever to expand that pool.

Electrophysiology. FARAPULSE, the pulsed-field-ablation platform, grew 22% globally in Q1, 18% in the United States and 30% internationally. Boston Scientific remains the PFA market leader. Its problem is that three larger competitors, Medtronic, Johnson & Johnson, and Abbott, are all now in the market. BSX conceded more share than it had modelled. Management now guides US EP to mid-single-digit growth, implying roughly flat sequential US revenue through year-end. This is a bear's strongest card. I grant it: competition in EP is structural, not a one-quarter blip. BSX's own answers (FARAWAVE Ultra, a Faraflex mapping-ablation catheter, a differentiated ICE platform) mostly arrive in 2027 and beyond. There is a real timing lag. Offsetting it, the company defends from leadership rather than chasing from behind, still growing a fast-growing market at twenty-plus percent internationally.

Urology. Plus one percent organic. Nobody inside the company pretended to be happy about it. Stone management lost ground to China volume-based procurement and to genuine holes in the portfolio, while sacral neuromodulation is still digesting heavy sales-force turnover from the Axonics integration. This is the most fixable of the three and the least structural: management has hired and is training nearly a hundred new reps, holds FDA clearance for the Asurys fluid-management system, and just closed Valencia's eCoin to broaden the incontinence menu. Urology should be a below-market year and a much better 2027. It is an execution pothole, not a moat problem.

Net it out and a pattern holds: one mix shift (WATCHMAN), one competitive squeeze that is real but bounded (EP), and one self-inflicted operational stumble already being repaired (Urology). None of them is a thesis-killer alone. Markets treated all three as permanent at once. That is the overreaction entry price captures. From here, study turns from the company to the stock.

Anatomy of a 60% Fall

Declines this violent are rarely one event. Boston Scientific de-rated across a chain of five, each landing on a market that had already lost patience with the last. Laid out in sequence, the damage tells you something important: almost none of it was a cash-flow miss; the biggest single-day drop came on a day with no new bad news at all.

| Date | Event | 1-Day Move | Close |

|---|---|---|---|

| Jan 15, 2026 | $14.5B Penumbra acquisition announced | ~-4% | $90.03 |

| Feb 4, 2026 | Q4'25 print, first weak FY26 guide | -17.6% | $75.50 |

| Mar 30, 2026 | CHAMPION-AF hits all endpoints, called "not the home run" | -9.0% | $62.93 |

| Apr 22, 2026 | Q1 beat plus guidance cut, briefly read as a clearing event | +9.0% | $64.87 |

| May 27, 2026 | Bernstein conference, guidance merely reaffirmed | -12.5% | $50.46 |

Source: Company disclosures, market data

Sit with May 27th line, because it is the tell. Management said nothing new at the Bernstein conference. It reaffirmed a guide already given a month earlier and noted WATCHMAN was tracking flat sequentially. On that non-news the stock fell 12.5% to $50.46. Selling that severe on the absence of a fresh catalyst is what capitulation looks like: the last holders of a broken thesis giving up on despair rather than on data. Historically, that kind of flush sits closer to an inflection than to a new leg down.

After May 27th drift continued for a duller, more mechanical reason. On June 30th, in the annual index reconstitution, Boston Scientific was removed from Russell 3000 Growth benchmark. A stock that de-rates from thirty times to thirteen no longer screens as "growth," so growth-index funds required to hold it become required to sell it, regardless of value. That forced, price-insensitive selling is now essentially complete. It pushed shares final leg from the low fifties to $45 and removed a natural buyer while doing so, which is exactly the sort of technical overhang that clears and then reverses. A separate, minor headline in late June, a recall of single-use Orca air-and-water valves used in endoscopy, added noise - a disposable accessory rather than an implant, immaterial to the thesis, but it fed a crowd already primed to sell.

Add it up and this was a de-rating in search of a reason, not an earnings collapse chasing a number. Those reasons were real. I will not wave them away. But each was a downgrade to the growth rate, not a break in the cash flows. When selling is driven by multiple compression, guilt-by-index-classification, and exhausted sentiment, recovery does not need a heroic beat. It needs the news to stop getting worse.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Boston Scientific Corporation (NYSE: BSX) is subject to significant risks including: competition in electrophysiology from Medtronic, Johnson & Johnson and Abbott; deceleration or reversal of WATCHMAN growth and uncertainty over label, guideline and national coverage determinations; execution risk in the Urology and Cardiac Rhythm Management franchises; integration and leverage risk associated with the pending Penumbra acquisition and the MiRus investment; tariff and supply-chain cost pressure; foreign-exchange exposure; and the risk of further guidance revisions. Technical analysis presented reflects historical price and volume data and is not a guarantee of future movements; RSI, moving-average, Ichimoku and channel signals are lagging or interpretive indicators with well-documented limitations. Scenario analysis, price targets and fair-value estimates are based on publicly available information, independent modelling and analyst-consensus data as of July 2026; actual results may differ materially. Entry, target and stop levels reflect scenario-based analysis, not price predictions. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision. Position-sizing guidelines are general in nature and do not account for individual circumstances, tax situations or risk tolerance.