Five years ago, Robinhood was that company. The one that halted GameStop trading. The one hauled before Congress. The one whose stock fell from $85 to $7.70 while retail traders seethed. The meme-stock villain. That narrative hardened fast - Robinhood was a gamified toy for reckless speculators, one crypto winter away from irrelevance. Not entirely wrong. Just about two years out of date.

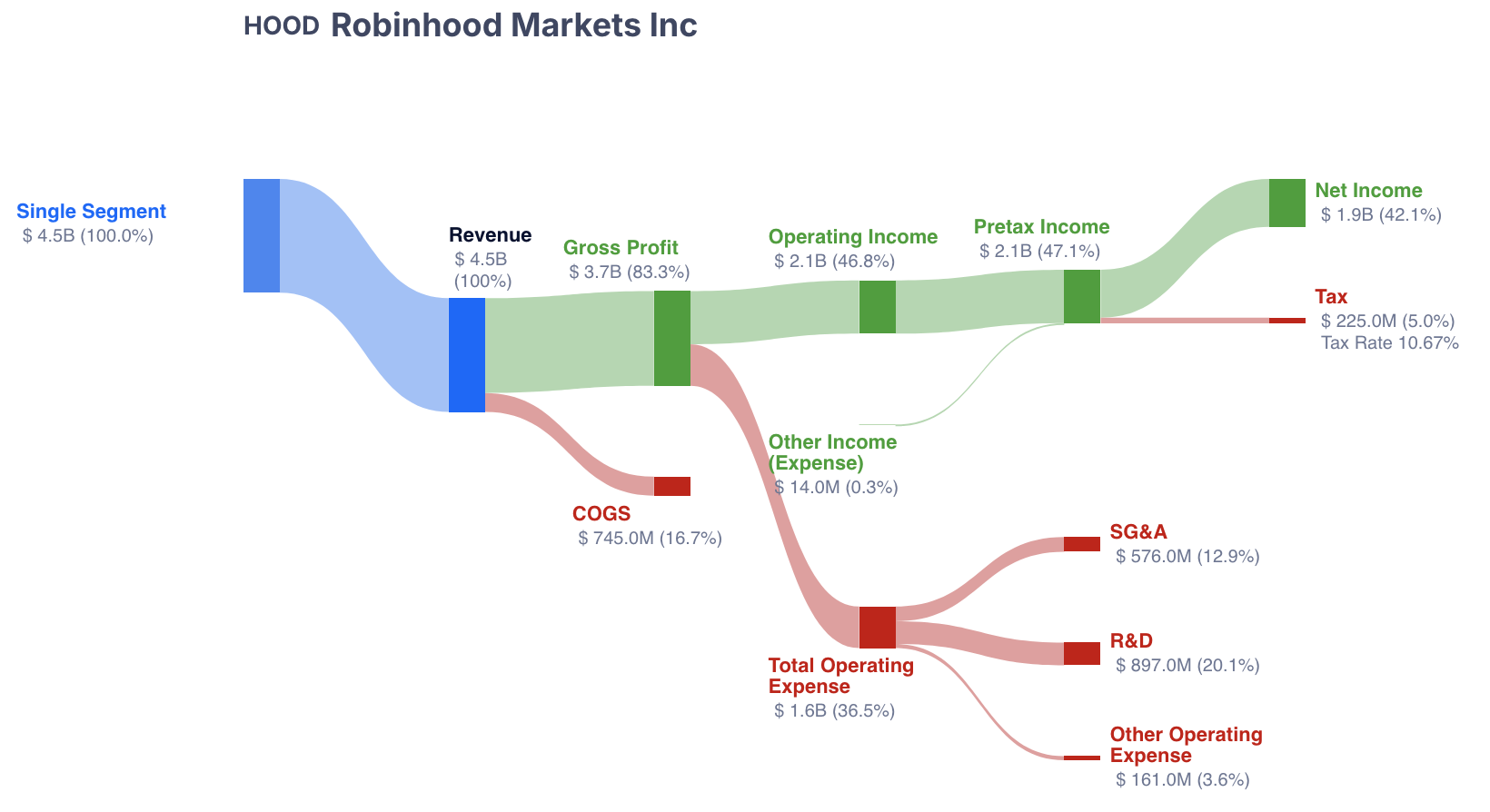

What the company actually delivered in 2025 wasn't a lucky quarter on the back of a crypto wave. It was $4.5 billion in revenue (up 52%), $1.9 billion in net income (EPS $2.04), $68 billion in net deposits, and 11 distinct business lines each generating over $100 million in annualized revenue. The company investors still mentally associate with GameStop now processes more options contracts than any U.S. brokerage, manages $324 billion in platform assets, and has 4.2 million paying Gold subscribers. Not a trading app. A financial operating system.

And yet. The stock is down 51% from its October 2025 highs. At roughly $72, you're paying about 29x forward non-GAAP earnings for a company growing revenue at 52%, with 56% adjusted EBITDA margins, a $1 billion buyback running, and a product pipeline covering private markets (Robinhood Ventures), AI advisory (Cortex), social trading, full banking, and international expansion into a $100 trillion generational wealth transfer. Coinbase - a company that is narrower, slower-growing, and more crypto-dependent - trades at a 75% P/E premium. Think about that for a second.

The entry zone of $XX-$XX reflects one simple view: the pullback - crypto cooling, macro fear, guilt-by-association with the broader fintech sell-off - has opened a window where the stock price is still narrating 2021 while the business is already living in 2026. That gap is the trade.

Robinhood at a Glance

Vlad Tenev and Baiju Bhatt were Stanford roommates with a simple pitch: democratize finance for all. Commission-free trading. No account minimums. The whole U.S. brokerage industry - Schwab, Fidelity, E*Trade, all of them - was eventually forced to follow. Robinhood went public in July 2021 at $38 per share, just months after the GameStop fiasco made it simultaneously the most famous and most hated company in retail finance.

What came next was ugly. The stock bottomed near $7.70 in 2022 as retail trading volumes dried up and rates climbed. But something interesting happened during that two-year nuclear winter: Robinhood rebuilt. IRAs with matching programs. The Gold subscription tier. Bitstamp acquisition for institutional crypto. An entirely new product stack. By late 2024, the company was GAAP profitable for the first time. By the end of 2025, eight consecutive profitable quarters and $1.9 billion in full-year net income. Most investors missed the whole thing.

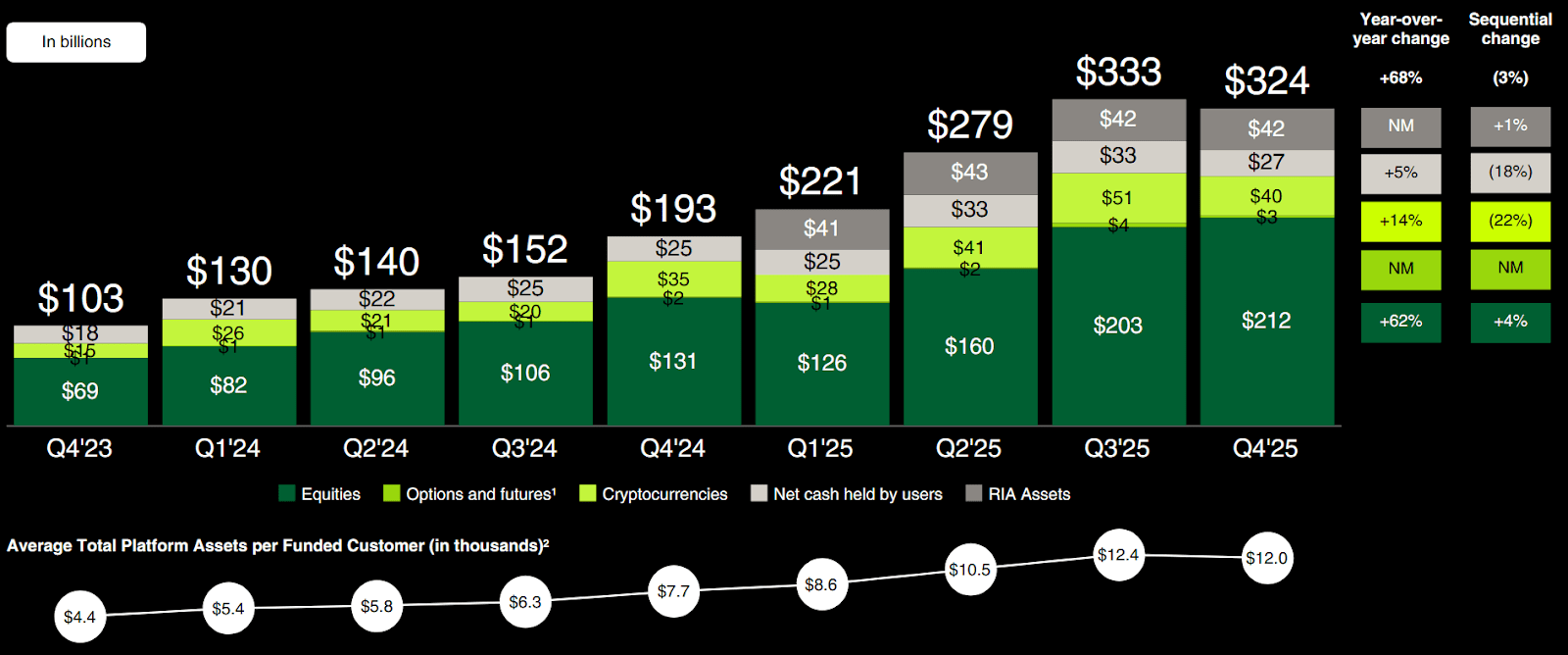

The company now serves 27.4 million funded customers across 28.4 million investment accounts. Over 40% of total assets are parked in ETFs, advisory products, retirement accounts, and cash - not crypto, not meme stocks. The speculative trading narrative that defined 2021 just doesn't match the actual asset mix anymore. The market's mental model is stuck in the past. The business isn't.

The Transformation - From Trading App to Financial Super-App

Here's what I keep coming back to: the Robinhood you remember from 2021 doesn't really exist anymore. That company was a single-product brokerage - live and die by PFOF from speculative options and crypto. The company operating today is a three-pillar financial platform with ambitions that put it directly in the path of Schwab, Fidelity, Coinbase, PayPal, and Goldman Sachs' consumer division. All at once.

It started in 2022 with a 1% IRA match (now 3% for Gold members). Audacious, frankly. The message was unambiguous: Robinhood wanted customers for decades, not for a bull market cycle. And it worked. Over 40% of total platform assets now sit in ETFs, advisory products, retirement, and cash - a number that would have been laughable to describe in 2021. Customers who open retirement accounts have lower churn, bigger balances, and longer lifetimes. The boring long-term stuff, it turns out, builds durable businesses.

"Over 40% of our total assets are now across ETFs, advisory, retirement and cash. It's great to see customers trusting us with more of their financial lives."

- Vlad Tenev, Q4 2025 Earnings CallThen came the Gold Card in 2024 - 3% cash back, 600,000+ active users, $10 billion in annualized spend. Banking launched late 2025 with 25,000 funded customers depositing $400 million out of the gate, and over 50% enrolled in direct deposit within months. That last number surprised me. Direct deposit enrollment is the kind of stickiness metric that banks spend years and significant money to achieve. Robinhood got there in the product's first months. Also in that same 18-month window: Robinhood Strategies (advisory), TradePMR (access to the $7 trillion RIA custody market), and Legend (desktop platform for serious traders).

The velocity is what separates this company from its peers right now. Tenev's framing from the Q4 call: the goal is "wallet share" - Robinhood customers should never need another financial app. So far, the data supports the ambition. Eight consecutive quarters of positive net transfers from all major brokerage competitors. Eight quarters. That stat doesn't come from a trading app. It comes from a platform that's genuinely taking market share from institutions that have been in this business for decades.

Revenue Architecture - Three Pillars, Eleven Business Lines

The old Robinhood basically lived on Payment for Order Flow. That was the vulnerability, and the bears were right to flag it. But the business has since built a three-pillar revenue structure, and the most common bear argument now - "Robinhood depends on crypto" - is only partially correct. That partial truth is exactly what the market is mispricing.

Transaction-Based

Net Interest

Subscriptions & Other

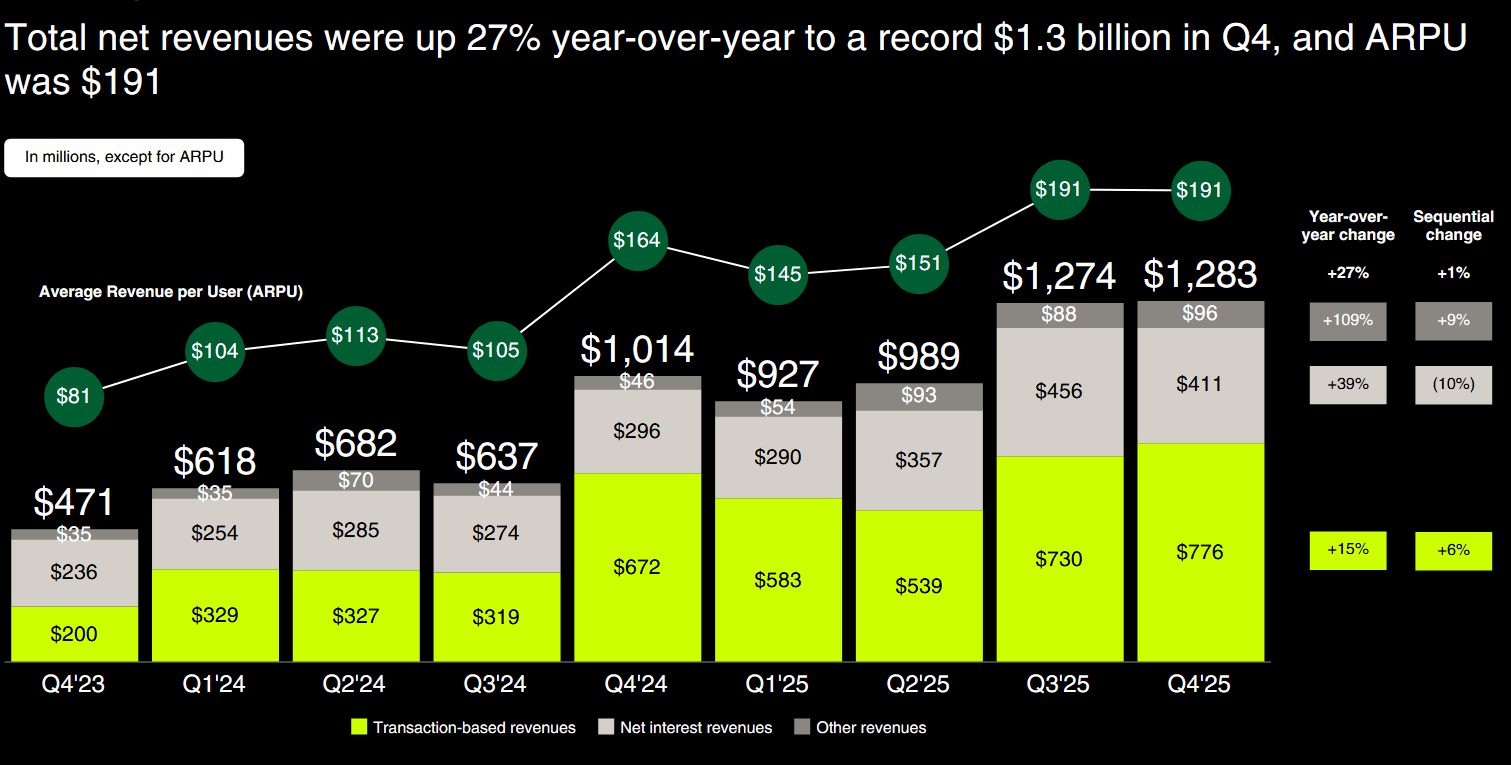

In Q4 2025, crypto transaction revenue was $221 million. Real money. But only 17% of total quarterly revenue. The "lives and dies by crypto" narrative just doesn't hold up against that mix. Run an extreme scenario: crypto transaction revenue falls to zero. Robinhood still generates approximately $1.06 billion in that quarter from equities, options, futures, event contracts, net interest, and subscriptions. Annualized, that's over $4.2 billion - higher than the company's entire 2024 revenue. The floor has moved.

ARPU reached $191 in Q4 2025 (trailing twelve months), up 16% year-over-year. And what's interesting here isn't the number itself - it's what's driving it. This isn't growth from adding cheap, low-engagement customers. Existing customers are trusting Robinhood with more of their money, more product categories, more of their financial life. That's the kind of growth that compounds in ways that are hard to model from the outside.

Q4 2025 Earnings & the Numbers Behind the Narrative

The Q4 2025 results are worth sitting with for a moment. Full-year revenue hit $4.5 billion - 52% growth year-over-year. That's the second consecutive year above 50%. Adjusted EBITDA reached a record $2.5 billion at 56% margins. Incremental EBITDA margins above 70% for the third straight year. The cost structure is scaling efficiently - revenue growing faster than expenses, which is exactly what you want to see at this stage.

Net deposits of $68 billion for the full year. Not total assets - net new money customers chose to add beyond market appreciation. That's a 35% annualized growth rate, and to put it in context: Robinhood brought in roughly as much fresh capital in 2025 as some regional banks hold in total deposits. Q4 alone was $16 billion. That was the eighth consecutive quarter above $10 billion. At some point you have to stop calling this a trend and start calling it a machine.

But it wasn't just a top-line story. Net income reached $1.9 billion. EPS of $2.04 reflects capital discipline as much as earnings growth - the denominator matters, as CFO Shiv Verma put it directly. Robinhood has a $1 billion+ buyback running, and during a period where the stock has fallen 51%, that program is buying back shares at what management clearly believes are deeply discounted prices. When companies buy back stock at multi-year lows, that's worth paying attention to.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Robinhood Markets, Inc. (NASDAQ: HOOD) is subject to market risk, crypto market risk, interest rate risk, regulatory risk including potential changes to Payment for Order Flow regulations, competitive risk from established brokerages, and execution risk on new product launches. The stock has high beta and is correlated with crypto market sentiment. Revenue from transaction-based sources is inherently volatile and may decline significantly during periods of reduced trading activity. Earnings estimates, price targets, and fair value calculations cited in this analysis are based on publicly available information and independent analytical models as of March 2026; actual results may differ materially. The entry and target zones reflect scenario-based analysis, not price predictions. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision.