TransMedics ran to roughly $150 in February. By the time the dust settled after its May 5th first-quarter print, the stock had given back about 55% and was trading in the low-$60s. What broke? Revenue growth decelerated to 21% year-over-year, the slowest in years, and adjusted operating margin compressed to about 10% of sales. For a name the market had learned to treat as a serial beat-and-raise machine, a single ordinary quarter read like a regime change.

Here is the part the tape is missing. That margin compression was deliberate and pre-announced. Management is front-loading a once-in-a-company-history wave of investment: the OCS Kidney program, a Gen 3.0 device platform, a European National OCS Program with its own dedicated air fleet, a new cold-storage product line called CHOPS, and a 498,000-square-foot headquarters. Strip those out and you still own the only FDA-approved warm-perfusion organ platform on earth, sitting behind roughly 26% of every liver, heart and lung transplant in the United States, throwing off $192.8 million of operating cash flow last year, and guiding to 20–25% growth this year. Flight activity, the cleanest real-time read on case demand, hit an all-time high in the same month the stock bottomed.

Scenario entry zone $XX.X–$XX.X corresponds to roughly 3.5x next-twelve-month EV/sales, the cheapest TransMedics has ever traded, versus a historical average closer to 8x and a slower-growing surgical-robotics peer at 13x. GuruFocus flags it in its lowest valuation band since 2022. Wall Street's published average target sits near $117. Market is pricing an investment year as if it were a broken business. That gap is the trade.

Signal Dashboard

Key Metrics at a Glance

Read that grid in two halves. Left of center is the business: a 37% grower in 2025, decelerating to a still-healthy 21% in the first quarter of 2026, sitting behind a quarter of all US thoracic and liver transplant volume, generating real cash for the first time in its history. Right of center is the dislocation: margins guided lower on purpose, a multiple that has fallen to the floor of its own range, and a published analyst target nearly double the current quote.

Worth saying plainly what kind of company this is, because it governs how you read the drawdown. TransMedics is not a binary biotech waiting on a single readout. It sells a commercial product, runs a national logistics network, and collects revenue every time an organ moves. Revenue is real, recurring at the case level, and growing. So when a 37% grower slips to 21% and the stock halves, the question is whether that deceleration is structural or self-inflicted. I will argue, across the sections below, that it is overwhelmingly the latter.

One number anchors the whole thesis. For the full year 2025, TransMedics generated $192.8 million in operating cash flow. A genuinely broken growth story does not produce that. A company spending heavily to pull forward its next three growth engines, while the existing engine keeps running, does. That distinction is the entire argument.

What TransMedics Actually Is

Device, Service, Network – Why This Cannot Be Copied on a Short Timeline

Most investors meet TransMedics as "the company that flies organs in jets" and stop there. That framing badly undersells what has been built. Three layers stack on top of each other, and each one is harder to replicate than the one beneath it.

First, the device. Organ Care System, or OCS, is the only FDA-approved portable warm-perfusion platform for the heart, lung and liver. For sixty years the standard of care was a beer-cooler full of ice and preservation fluid, a method essentially unchanged since the early 1960s. Cold storage suspends an organ's biology and starts a clock: a heart has roughly four hours before accumulated ischemic damage makes it unusable. OCS does something categorically different. It keeps the organ warm, oxygenated and functioning in real time. A liver on OCS produces bile. A heart on OCS beats. An organ on OCS does not know it has left the donor. That eliminates the decay clock, lets organs travel coast-to-coast, and most importantly resurrects organs that cold storage would have forced surgeons to discard.

Second, service. Proving that a device worked was never what stalled adoption. What stalled adoption was operational burden — an individual transplant center could not absorb training perfusion teams, staffing procurement surgeons for 2 a.m. flights, chartering aircraft, and coordinating with its local procurement organization, all on top of an already-stretched on-call schedule. So in 2022 TransMedics built its National OCS Program, or NOP, and took that entire operation onto its own balance sheet. A center calls NOP. NOP sends a surgeon and a clinical specialist, manages perfusion, arranges logistics, and delivers a living, assessable organ to a waiting operating room. Revenue went from $30 million in 2021 to $93 million in 2022 once a constraint on adoption was removed.

Third, the network. In 2023 TransMedics acquired a charter operator and began building a dedicated fleet of Embraer Phenom 300E jets flown only for organ transport. Wall Street hated it; medical-device investors did not sign up for jet fuel and FAA compliance. They missed the point. Owning the aircraft converted unpredictable spot-market charter costs into a fixed asset the company controls, and turned logistics from a ceiling on growth into a moat. By the end of 2025 the fleet stood at 22 aircraft covering roughly 82% of NOP air missions.

"Our vision has always been bold and growth-oriented... we've been deliberate yet aggressive in our strategic investment in growth initiatives. We believe that 2026 is a critical and transformational year that stands to cement TransMedics' near, mid- and long-term growth trajectories... we fully expect that our financial performance over the next several quarters will reflect these necessary investments in people, infrastructure and technology development."

Waleed Hassanein, M.D., Founder & CEO — Q1 2026 Earnings Call, May 5, 2026Sit with that quote, because it pre-frames every margin number you will read in this tip. Management told investors, in advance and on the record, that they were going to spend now to capture later. Per company data drawing on national registry figures, between 2022 and 2025 US liver, heart and lung transplant volume grew about 25%; without OCS and NOP, management says it would have fallen roughly 1%. A 26-point swing in the national trajectory of a system that had crawled for decades.

Why has no Medtronic or J&J replicated this? Because the product and the service are inseparable, and large device companies are not built to run a 24-hour command center, employ more than fifty transplant surgeons, and operate an airline. TransMedics ran nine FDA pivotal trials to get here. A competitor showing up today with a perfusion box and retrospective data is not two years behind. On the Level-1 clinical evidence alone, they are closer to two decades behind. Founder-analysts call the combination of device, clinical service and owned logistics the "TransMedics Trident" ... three prongs a domestic rival has to match simultaneously, not one at a time.

Why This Market Still Exists

Why This Market Still Exists – Discards, Dialysis, and a $40B Bill

Sizing this opportunity means sizing waste. American transplant medicine, for all its sophistication, was engineered to manage scarcity, not to overcome it. Clearest evidence of that sits in one organ: kidney.

As of late 2024, roughly 90,000 Americans were waiting for a kidney, by far the longest list of any organ. In 2024, procurement organizations recovered more than 25,000 kidneys from deceased donors and discarded over 9,200 of them. One in four recovered kidneys went in the trash, a discard rate that has climbed more than 80% in five years. Those discards are logistical, not medical: by the time an offer reaches a willing center, the cold-storage clock has run too far. A National Academies study found that roughly 62% of kidneys discarded in the United States would have been transplanted in France, the same organs, lost to a slower system rather than a sicker population.

Behind the waitlist sits a fiscal monster. The 90,000 people waiting are mostly on dialysis, which costs Medicare $50,000–$90,000 per patient per year; the end-stage renal disease program runs north of $40 billion annually, roughly 6–7% of the entire Medicare budget for under 1% of beneficiaries. A successful transplant frees a patient from dialysis for a decade or more. So when CEO Waleed Hassanein says that in every meeting with the Centers for Medicare & Medicaid Services the first question is "when is the OCS Kidney arriving?", he is describing a payer that is structurally desperate for what TransMedics is building.

Why does this matter for a 9–12 month trade rather than a ten-year thesis? Because it tells you the runway is not the constraint. TransMedics handled about 5,139 US cases in 2025 against a near-term ambition of 10,000 by 2028, and a kidney program that addresses a pool larger than heart, liver and lung combined. A business one-third of the way into its own stated target, trading at a trough multiple, is the setup that creates asymmetric entries. That long-term story underwrites the near-term margin of safety.

Q1 2026 Earnings Read

A 21% Growth Quarter, a 55% Drawdown – Reading May 5th Line by Line

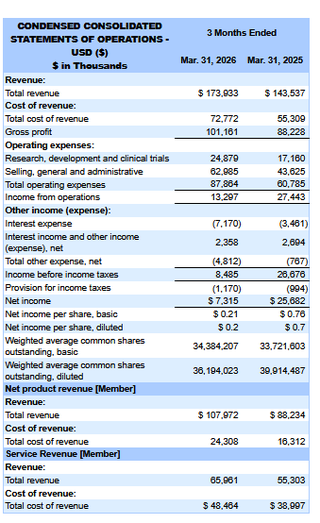

Let me walk through the May 5th print without spin. First-quarter revenue came in at $173.9 million, up 21% year-over-year and 8% sequentially. US transplant revenue was $167 million, growing 20%; international, still tiny, was $5.6 million but up 39%. By organ: liver $139 million, heart $26 million, lung just $2 million. Product revenue $108 million (+22%), service revenue $66 million (+19%), logistics inside that at $32 million (+22%). Adjusted operating profit of about $18.1 million, roughly a 10.4% margin. Cash ended the quarter at $462 million.

Two things spooked the market. Growth had been running 30–40%+ for years; 21% felt like a ceiling arriving. And adjusted operating margin, which touched the high teens in 2025, fell to about 10%. Gross margin slipped to roughly 58%, down 331 basis points from a year earlier. Put those together and a market conditioned to serial beats decided that the story had changed.

Q1 income statement, right from a 10-Q

Most useful read of that comparison is what stayed positive. Gross profit still expanded by roughly $13 million in absolute dollars despite the headline margin slip — meaning the business above the operating-expense line is still scaling cleanly with revenue. Every basis point of net-income compression sits below gross profit, in the deliberate step-up of R&D and SG&A. So when the bear case is framed as "earnings missed," the more accurate framing is: TransMedics chose to take $14 million of incremental operating profit and redeploy it into kidney, Gen 3.0, European NOP and CHOPS in a single quarter. Even after that deliberate redeployment, operating income, net income and diluted EPS all stayed positive. A company funding three new growth platforms simultaneously while still printing positive net earnings is a very different story than the headline "EPS miss" suggested.

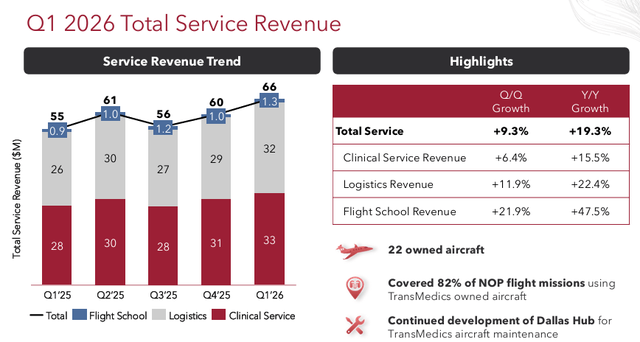

Service revenue trend – a demand signal under a headline

This slide is the antidote to the headline panic. Service revenue is the line of TransMedics' P&L most directly tied to NOP case volume — clinical service plus logistics plus flight school — and every single sub-line accelerated in the same quarter the headline number decelerated. All three sub-lines printed double-digit YoY growth, and clinical service plus logistics combined now run at roughly the same dollar pace as net product revenue. Fleet coverage of NOP missions also ticked higher quarter-over-quarter, meaning more of every incremental case is captured inside TransMedics' own logistics economics rather than paid out to third-party charter. Read that way, the part of the business that scales with actual transplant adoption kept compounding through the very quarter the market priced as deceleration.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. TransMedics Group, Inc. (NASDAQ: TMDX) is a high-growth medical technology company subject to significant risks including: revenue concentration in liver transplantation; dependence on continued adoption of the Organ Care System and the National OCS Program; clinical and regulatory risk on the ENHANCE Heart, DENOVO Lung, CHOPS, and OCS Kidney programs and any FDA or international approvals; execution risk on international expansion and the PAD Aviation partnership; aviation operational risk including fuel-price exposure, pilot availability, and FAA compliance; sensitivity to US transplant policy, the Transplant Modernization Act, OPTN reform, and reimbursement dynamics; meaningful and ongoing shareholder dilution; quarter-to-quarter seasonality and variability in donor volumes; near-term operating-margin and free-cash-flow compression from front-loaded investment; and general macroeconomic sensitivity as a long-duration growth asset. Technical analysis presented reflects historical price and volume data and is not a guarantee of future price movements. RSI and moving-average signals are lagging indicators with well-documented limitations. Scenario analysis and price targets are based on publicly available information, independent modelling, and analyst consensus data as of May 2026; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision. Position-sizing guidelines are general in nature and do not account for individual circumstances, tax situations, or risk tolerance.