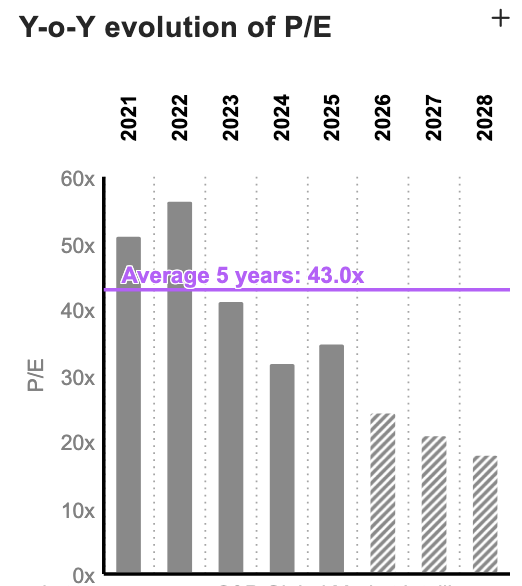

For most of the past decade, Xylem was a stock you only ever bought expensive. Shares changed hands in the thirties and forties times earnings because the market treated clean water as a one-way structural bet and paid up for it. That premium is gone. After a year in which the broad market climbed roughly a fifth and Xylem went sideways, a 40x compounder now sits at under 20x forward adjusted earnings, less than half its own five-year average multiple. Same franchise. Same megatrend. Roughly half the price tag.

Here is what the cheapness is paying you to look past: organic revenue was flat in the first quarter, China sales fell 30%, and a deliberate portfolio cleanup is shaving points off the top line. Here is what it ignores. Order backlog sits at a record $4.7 billion with book-to-bill above one, company just booked its largest contract in history, data-center orders in one segment already topped all of last year and management is buying back stock hand over fist into the weakness. Scenario entry zone $XXX-$XXX is where the valuation floor and the chart finally agree, with shares back at a multi-year base it has defended three times.

There is a top-down reason to care now, too. Capital has spent two years crowding into a handful of AI and technology names. When that trade cools and money rotates back toward real, tangible, hard-asset businesses, the neglected compounders move first. Xylem is exactly that kind of name: pumps, pipes, meters and treatment plants that the world cannot run without. Market is pricing a water compounder as if its best years are behind it. I think the tape and the order book say otherwise.

Key Metrics at a Glance

Numbers above describe a business the market has decided to ignore. A $9 billion water-technology franchise growing earnings high-single-digits, throwing off cash, raising its dividend for a sixteenth straight year and carrying almost no net leverage. Forward multiple under 20x adjusted earnings is the part that should make you sit up. For a decade this stock was a 30x-to-40x name. Investors complained it was too expensive to own. That complaint no longer holds.

One figure frames the whole setup. Five-year average price-to-earnings ratio for Xylem is roughly 43x. Today's forward multiple sits at less than half of that. Earnings did not collapse to justify it. Adjusted EPS is guided up about 8% this year and consensus has it compounding near 10% a year through 2028. A quality compounder trading at half its normal multiple while earnings keep climbing is the definition of multiple compression, not business deterioration. Distinguishing one from the other is the entire job of this tip.

What pulled multiple down is real and worth naming up front: organic growth stalled to zero in the first quarter, China is in a deep trough, and management is deliberately walking away from low-margin revenue. That cocktail kept buyers away for a year while everything else in the market ran. My argument is that each drag is either self-inflicted or cyclical, that the order book is already pointing up, and that you are being paid an unusually wide margin of safety to wait for the turn.

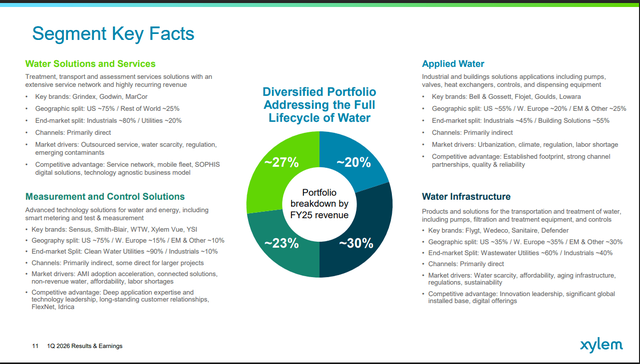

What Xylem Actually Is - Four Segments, One Essential Job

Strip away the jargon and Xylem does one thing: it moves, measures, treats, and protects water for the people who cannot afford to get it wrong. Utilities. Industrial plants. Cities. Spun out of ITT in 2011, today it runs across more than 150 countries, employs roughly 22,000 people and books around $9 billion a year across four segments of roughly equal size. No single-product rival covers the same ground. That breadth is the first half of the moat.

Walk the four. Water Infrastructure, about 30% of revenue, moves and treats water under brands like Flygt, Wedeco and Sanitaire. Water Solutions and Services, about 27%, runs outsourced and emergency water operations with a long recurring-service tail. Measurement and Control Solutions, about 23%, is the smart-meter and sensing arm anchored by Sensus and the Xylem Vue software platform, the piece that turns hardware into recurring digital revenue. Applied Water, about 20%, sells pumps and systems into buildings and industry under Bell & Gossett, Goulds and Lowara. Equal legs, different drivers.

Balance is the moat's quiet half. When Water Infrastructure treatment softened this spring and China fell 30%, energy metering and dewatering picked up the slack and the consolidated top line still held. A business with four roughly equal legs does not tip over when one wobbles. That is why a company growing zero organically in a given quarter can still expand margins and beat earnings, which is precisely what happened.

Stickier half is switching cost. Xylem sells into mission-critical systems where failure is measured in boil-water notices and shut-down production lines, so buyers do not chase the cheapest pump. They specify the proven one, then stay. Once a utility standardizes on Sensus meters or a plant runs on Flygt pumps and Xylem's analytics layer, ripping it out is a multi-year, multi-million-dollar project nobody wants to own. Buyers here pay for uptime, compliance, and lower lifetime cost, not for novelty, and that is what turns recurring service, spare parts, and software on a decades-old installed base into something close to an annuity.

Demand behind it is not a story you have to squint to believe. CEO Matthew Pine put hard numbers on the call.

"We're dealing with an aging infrastructure in the developed parts of the world... If you look at what the U.S. Army Corps of Engineers says about our infrastructure, they give us a C- to a D+ depending on which part... drinking water, wastewater, and stormwater. So we talk about $1.5 trillion needed over the next decade, just in the U.S. to maintain those poor ratings."

Matthew Pine, CEO, Xylem Q1 2026 Earnings Call, April 28 2026That is the demand floor under this franchise: a maintenance bill developed economies have already run up, on top of a global water-treatment market independent researchers expect to compound in the mid-teens through 2030. A business this essential, this diversified, and this entrenched does not stay a flat-growth story forever. It is flat right now for specific, fixable reasons, which is exactly what the next section takes apart.

Why This Stock Went Nowhere - And What Ends It

Quality franchise plus structural demand usually means an expensive stock, and for a decade that is exactly what Xylem was, a 30x-to-40x name income investors grumbled they could never buy cheaply. Then it went nowhere for a year. While the broad market climbed roughly a fifth, Xylem drifted sideways and its multiple quietly halved. Earnings did not collapse to cause it. A rating did.

So what actually went wrong? Three things...naming them honestly is the whole point. First, a deliberate cleanup management calls 80/20: walking away from low-margin business, which shaves roughly 200 basis points off organic growth and peaks this year. Second, China, down 30% year on year, a drag Xylem partly chose by exiting low-value work. Third, ordinary project-timing lumpiness in the services arm. Add a flat first quarter and you get a stock the momentum crowd had no reason to touch.

Here is why none of that is the franchise breaking. Two of the three drags are self-inflicted, the deliberate price of a margin program that is already lifting profitability. China is cyclical and, by management's own read, "bottoming." And underneath the soft headline, the order book is pointing the other way: a record $4.7 billion backlog, book-to-bill above one, smart-metering orders up double digits and data-center bookings in one segment that already topped a full prior year. Drags on a timer, orders turning up. To me, that is much more of a coiled spring than a value trap.

There is a top-down reason to look now, too. Capital has crowded into a thin band of AI and technology names for two years, and the real-economy, hard-asset businesses got left behind, repriced on neglect rather than results. When that trade broadens, money rotates back toward tangible-asset compounders and water sits at the center of that map. So the question is no longer whether Xylem is a good business. It plainly is. Real question is whether this is the moment to act, which the franchise, financial, valuation, technical work that follows is built to answer.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Xylem Inc. (NYSE: XYL) is an industrial company subject to significant risks including: cyclicality in industrial and municipal end markets; dependence on government and utility budgets and the pace of infrastructure funding; international exposure, particularly a prolonged downturn in China and currency fluctuation; integration and execution risk on acquisitions and divestitures, including the Evoqua and Sensus International transactions; raw-material, tariff, and energy-cost inflation; interest-rate sensitivity for a long-duration quality compounder; the risk that organic growth fails to re-accelerate as guided; and the risk that return on invested capital remains below the cost of capital. Technical analysis presented reflects historical price and volume data and is not a guarantee of future price movements. Fibonacci levels, RSI, and moving-average signals are lagging indicators with well-documented limitations. Scenario analysis and price targets are based on publicly available information, independent modelling, and analyst consensus data as of June 2026; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision. Position-sizing guidelines are general in nature and do not account for individual circumstances, tax situations, or risk tolerance.