Opening Perspective

I almost passed on this one. "Consolidated Water" - a sub-$500M market cap company headquartered in the Cayman Islands, producing desalinated seawater for Caribbean island utilities - doesn't exactly scream opportunity. It sounds like the kind of company you discover on page 14 of a stock screener, shrug at, and move on. That's precisely why I'm writing this.

What stopped me was a number I don't often see: negative net debt. The company carries $99.4M in cash and virtually no debt. At a $400M market cap, the enterprise you're actually paying for is worth roughly $300M - a water infrastructure business that has operated profitably since 1973, paid dividends since 1985, and just signed a $204M contract to build and operate a desalination plant in Hawaii for the next two-plus decades. The market is valuing 20 years of recurring O&M revenue from that contract at almost nothing.

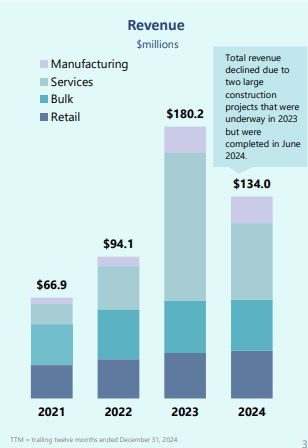

The Q4 2024 earnings call (March 18, nine days ago) was telling. Revenue dropped 47% year-over-year - but only because two large construction projects were completed in early 2024. CEO Rick McTaggart was calm about it: "We knew this was coming." Meanwhile, recurring operations-and-maintenance revenues grew 51% to $29.3M. The company is quietly becoming more stable as a business even as the headline revenue number falls off a cliff. And construction - the volatile, high-margin driver - is coming back hard in 2026 when Hawaii breaks ground.

There is regulatory risk in Cayman. There is client-payment risk in the Bahamas. This is a microcap with thin liquidity and a non-Big-Four auditor. I am not pretending otherwise. But at $XX–$XX, the math on risk-reward is compelling enough that it deserves a position.

Key Metrics at a Glance

The Stock Nobody Watched - And Then It Doubled

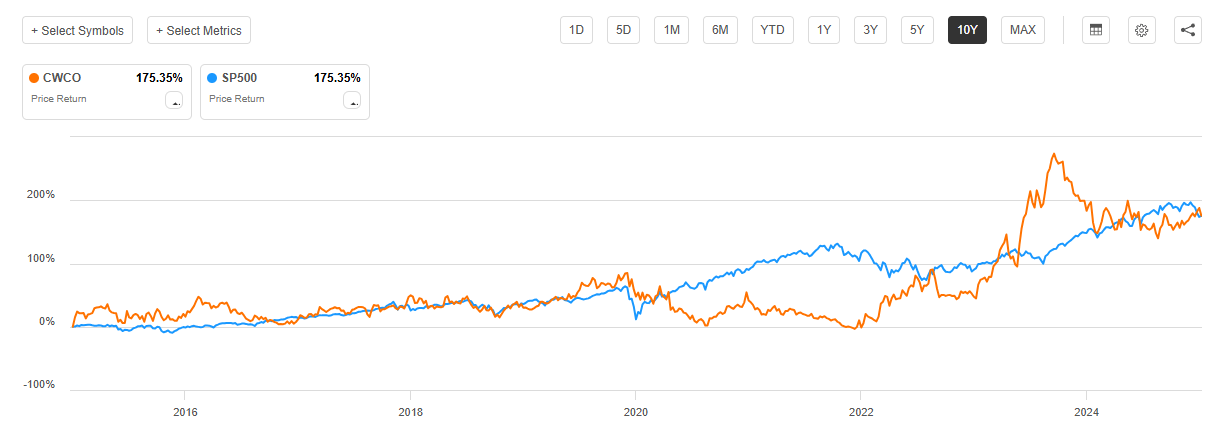

Over the past decade, Consolidated Water has matched the S&P 500 almost tick-for-tick - a 175% total return from a microcap Caribbean water company that few institutional investors bother to cover. The catch: almost all of that outperformance came in a single surge during 2023, when a new desalination plant in Cayman and construction contracts in Hawaii and the Caribbean all crystallised simultaneously. The stock ran from under $14 to over $40. Then it gave half of it back. We're now back near the base of that rally - with an even better earnings profile and a larger catalyst on the horizon.

CWCO has always been a sleeper with episodic catalysts. Long stretches of sideways drift, then a sharp re-rating when a big contract or expansion finally hits the income statement. The 2023 spike was one of those episodes. The 2026 Hawaii construction commencement could be the next - and this time the setup is cleaner because the stock has already retreated to entry-level prices while the balance sheet has actually improved.

Four Revenue Streams, One Overlooked Business

The "water utility" label is misleading. Consolidated Water operates across four distinct segments - the most exciting of which (Services) looks terrible right now because two large projects were completed in 2024. But the revenue mix is actually shifting toward something more durable, and most people watching the headline number are missing it entirely.

The crown jewel. Exclusive utility concession in Grand Cayman - CWCO produces all potable water for two of the island's most populated areas via reverse osmosis. Record volumes in 2024: 4.3% more customer accounts, 4.5% more water sold. Highest margins in the group. The island keeps growing.

Sells treated water wholesale to state utilities in the Caymans and Bahamas. The Bahamas client (WSC) is the concentration risk - and a chronic late-payer - but $28M in receivables has always eventually been settled with interest. The cash-heavy balance sheet turns this from a threat into an inconvenience.

The volatile segment - design-build-operate contracts. Construction revenue fell from $77.3M in 2023 to $17.6M in 2024 as two projects finished. But the underlying shift is important: O&M contract revenues grew 51% to $29.3M (plus additional project, technical, and management services revenues). PERC Water and the new REC (Colorado) subsidiary are building a recurring revenue base that's changing the segment's character permanently.

Aerex Industries - an OEM supplier of water production and treatment equipment, operating in Fort Pierce, Florida. Revenue stable at $17–18M; margins improving on better product mix and fabrication efficiency. Aerex is expanding its facility (completion late 2025) to run more jobs simultaneously. A quiet compounder inside a compounder.