ServiceNow just had its worst single-day selloff since IPO. Down 17.7% on April 23rd. Worst day in fourteen years. And it happened after a beat-and-raise quarter. Revenue $3.77B, subscription growth 22% year-on-year, AI commitment lifted 50% from $1.0B to $1.5B for the year, RPO at $27.7B growing 25%, 16 deals over $5M in net new ACV, renewal rate at 97%. None of that triggered the sell. What did was a Q2 operating margin guide of 26.5% versus the Street at 30.1%, a 200 bps headwind to free cash flow from the freshly closed $7.75B Armis acquisition, and a handful of on-premise deals slipping in the Middle East as Iran tensions delayed sovereign cloud closings.

Here is what the price tells you the business is doing: it is broken. Here is what the business is actually doing: NOW Assist customers spending over $1M in ACV grew 130% year-on-year, 50% of net new revenue now comes from non-seat-based pricing, and Moveworks delivered more deals in Q1 alone than it did in all of 2025. Bill McDermott told analysts that the goal of $1B in AI commitments for the year was "understated". They are already at $1.5B and on a run. Yevgeny Dibrov, CEO of Armis, joins the team to run security. ServiceNow now sits inside 9 of the world's 10 largest companies, and roughly 40% of the Fortune 100, via Armis alone.

Scenario entry zone $XX–$XX reflects forward P/E of roughly 20x against a 5-year median of 64x, a 68% discount to its own history, cheaper than Microsoft, Oracle, and SAP despite faster top-line growth. At GuruFocus' GF Value of $223, NOW is flagged as "significantly undervalued" for the first time in the company's modern history. Wall Street consensus from 47 analysts sits at $143.40 average, with high of $240 and low of $85. Market is pricing a structural break in software while ServiceNow's underlying business reaccelerates. That is the dislocation. That is the trade.

Key Metrics at a Glance

Numbers above describe a SaaS business operating at scale most peers can only target on a roadmap. A $15B subscription revenue base compounding above 20% per year. Operating margin at 32%, eleven points higher than five years ago. Free cash flow margin at 44% in Q1. Remember, Q1 is the seasonal high, so the full-year 35% guide is the cleaner read. Rule of 56 number management quotes is real: revenue growth plus FCF margin lands at 56.8 on trailing twelve months, well above the Rule of 40 benchmark McKinsey uses to define elite software.

What matters more than any single Q1 figure is the shape of contracted backlog. RPO at $27.7B growing 25% is contracted revenue customers have already committed to pay, and it is growing faster than recognised revenue, which means the pipeline of future revenue is widening, not narrowing. Software in structural decline does not have backlog accelerating. Software losing seats to AI does not see 28 new customers cross the $5M annual spend line in a single quarter while renewal rates stay glued to 97%.

One number I keep returning to: 50% of net new business in Q1 came from non-seat-based pricing: tokens, infrastructure, hardware, connectors. A year ago, that figure was barely measurable. ServiceNow has executed the single most important pricing pivot in enterprise software. While Wall Street debates whether AI kills the seat model, ServiceNow has already moved past it. Half the new business is structurally usage-priced. Rather than a company exposed to AI disruption, this is a company monetizing the same trend that is supposedly disrupting it.

What ServiceNow Actually Is ... and Why It Cannot Be Vibe-Coded

Biggest misunderstanding in this whole AI-disruption discourse is treating ServiceNow as a CRM clone or a help-desk ticketing app. That framing is so wrong it borders on malpractice. ServiceNow is not a feature. It is connective tissue.

An average Fortune 500 company runs on roughly 100 million lines of custom code stitched across hundreds of point applications, three or four hyperscaler stacks, dozens of SaaS vendors, several systems of record, and an explosion of homegrown tools. ServiceNow sits above that chaos and orchestrates the workflow between humans, agents and software. McDermott calls it the "AI control tower for business reinvention." Customers call it the "ERP for IT." Pick your label. Functionally, it is the rail on which work moves inside a global corporation.

"There has never been a tailwind for ServiceNow like AI. Since Fred Luddy started the company, we've always focused our platform on the jobs our customers needed done... As code volume increases 20x by 2030, the complexity of managing this explosion of code will increase exponentially. Volume of tickets generated by this complexity will also explode. In this scenario, the number of tickets hitting an ITSM system will increase by 50x compared to today."

Bill McDermott, Chairman & CEO, ServiceNow Q1'26 Earnings Call, April 22 2026Context Engine is what makes that defensible. ServiceNow has trained on more than 95 billion annual workflows and 7 trillion transactions across 22 years inside the world's most regulated, most complex enterprises. Approval chains. Cost thresholds. Vendor histories. Asset dependencies. Identity relationships. Compliance rules. None of that lives in a foundation model. None of it can be inferred from a public corpus. A large language model is brilliant at generating language. ServiceNow knows which approval chain applies when a $50,000 procurement request from a German subsidiary touches an asset that is subject to GDPR and tied to a vendor on the export-control list. Foundation models do not. They cannot.

That is also why "vibe-coding" the replacement does not work. A start-up can spin up a chat interface in a weekend. It cannot replicate two decades of accumulated enterprise context, a network of integrations into SAP, Workday, Salesforce, ServiceNow's own CMDB, and a 200,000-customer install base. Customer base is the moat. Data flywheel is the moat. AI is the accelerant, not the assassin.

Platform now spans five hypergrowth surfaces management called out on the call: core IT (ITSM, ITAM, ServiceOps), AI security via Armis + Veza, AI-native CRM, EmployeeWorks as the conversational front door, and Workflow Data Fabric. Each is large enough to be a stand-alone public company. All sit on a unified data layer and a single Context Engine. That is the structural advantage hyperscalers and language model companies cannot match, and it is precisely what the current selloff ignores.

A Beat-and-Raise Quarter, Worst Single-Day Drop Since IPO

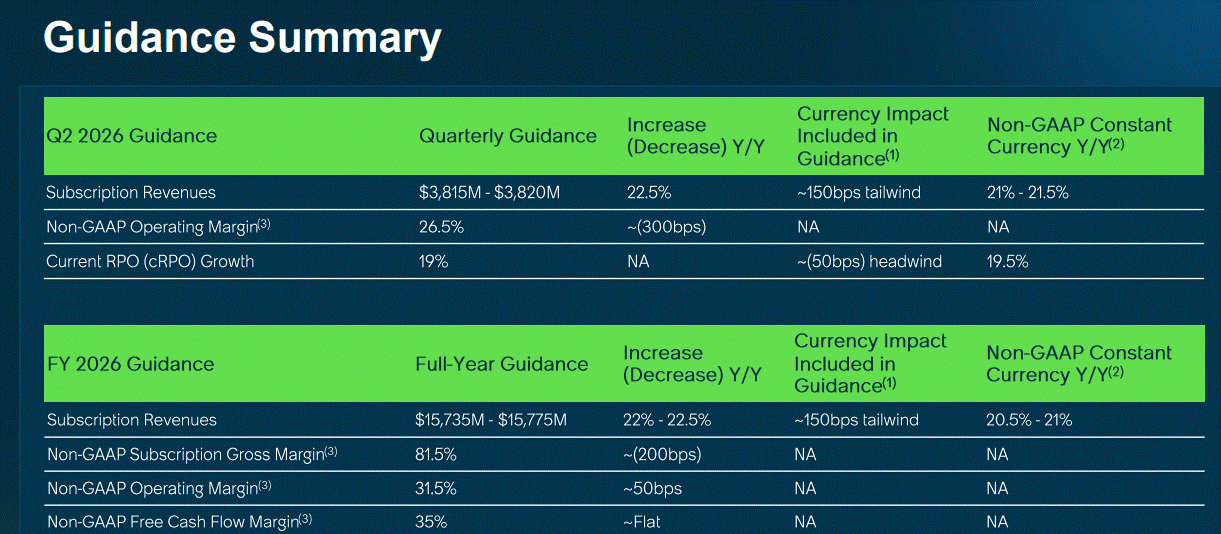

Let me lay out what actually happened on April 22nd, after-hours. ServiceNow reported Q1 FY26 revenue of $3.77B (consensus $3.75B), non-GAAP EPS of $0.97 (consensus $0.97), and beat its own subscription revenue guide at the high end. Non-GAAP operating margin came in at 32%, fifty basis points above guidance. FCF margin at 44%. Subscription revenue guide for the full year was raised by $205M at the midpoint to $15.735–$15.775B. AI commitment for the year was raised 50% from $1.0B to $1.5B. Renewal rate held at 97%.

Stock closed Wednesday at $103.07. It opened the next morning trading near $83. Intraday low touched $83.58. Down 17.7% on the day. Worst single-day selloff in ServiceNow's history since the June 2012 IPO. Volume hit the highest since late 2019, before the pandemic. By any reasonable measure, this was a capitulatory event. And by any reasonable measure, the reaction was wildly disproportionate to what was reported.

So what triggered it? Three things, in order of weight:

First, Q2 operating margin guidance came in at 26.5% versus a Street expectation of roughly 30.1%. That gap is real. Driver is the freshly closed $7.75B Armis acquisition, a 125 bps headwind to Q2 operating margin, 75 bps to full-year operating margin, 25 bps to subscription gross margin, and 200 bps to full-year free cash flow margin. None of that was a surprise to anyone reading the acquisition announcement. But the market interpreted Armis dilution as a sign that ServiceNow is "buying growth" because organic is decelerating. That framing is uncharitable. Excluding Armis, management held the full-year subscription guide flat at the prior level despite delayed Middle East deals. Holding flat in this macro reflects execution under stress, not deceleration.

Second, delayed on-premise deals in the Middle East represented a 75 bps headwind to Q1 subscription revenue. Iran war pushed several sovereign cloud closings out of the quarter. Those deals are sovereign clouds, recognised as on-premise revenue, so the impact is lumpy. It hits all at once instead of ratably. Management said the conversations are active, people are back in their offices, and a few of those on-prem deals already closed in Q2. CFO Mastantuono explicitly noted that the full-year guide does not assume the Middle East situation resolves. Reads as conservative guiding rather than deteriorating fundamentals.

Third, and most telling, Anthropic's ARR run-rate hit $30B during the quarter, up from $9B at the end of 2025. That spike triggered a sector-wide panic that AI labs are eating SaaS budgets and seat-based pricing is dead. Software ETF IGV is down 9% YTD. NOW is down 57% from the January 2025 high. Adobe is down nearly 30%. Salesforce is down too. Market is pricing a sector reset, not a ServiceNow-specific deterioration. That is why I find the entry asymmetric. Selloff is index-driven sentiment, not name-specific data.

One detail worth lingering on. Bill McDermott has been doing earnings calls for over twenty years across SAP and ServiceNow. His tone on this call was notably defiant rather than defensive. Quote: "In the short run, markets are voting machines. And right now, uncertainty is winning the vote. But don't worry. In the long run, they are weighing machines. And I'll tell you, I'll get on that scale with that ServiceNow brand on my chest any day." Translation: management is unflinchingly confident, the Board is supportive, the Financial Analyst Day on May 4 in Las Vegas will be the next opportunity to reset narrative. McDermott also gave an early headline (the $1.5B AI commit number) that he openly admitted was supposed to be reserved for FAD. That is not the posture of a CEO worried about the trajectory.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. ServiceNow, Inc. (NYSE: NOW) is a high-growth technology company subject to significant risks including: competitive pressure from Microsoft, Oracle, Salesforce, Workday, foundation-model AI labs, and other enterprise software vendors; dependence on continued enterprise adoption of agentic AI and workflow automation; macroeconomic sensitivity as a long-duration growth asset; geopolitical exposure through the Middle East and other international markets; integration risk associated with the recently closed Armis ($7.75B) and Veza ($1.2B) acquisitions; elevated stock-based compensation as a percentage of revenue; potential for further multiple compression if SaaS sector sentiment deteriorates further; and execution risk on the pricing transition from seat-based to consumption-based models. Technical analysis presented reflects historical price and volume data and is not a guarantee of future price movements. RSI and moving average signals are lagging indicators with well-documented limitations. Scenario analysis and price targets are based on publicly available information, independent modelling, and analyst consensus data as of April 2026; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision. Position sizing guidelines are general in nature and do not account for individual circumstances, tax situations, or risk tolerance.