The Most Powerful Advertising Engine on Earth

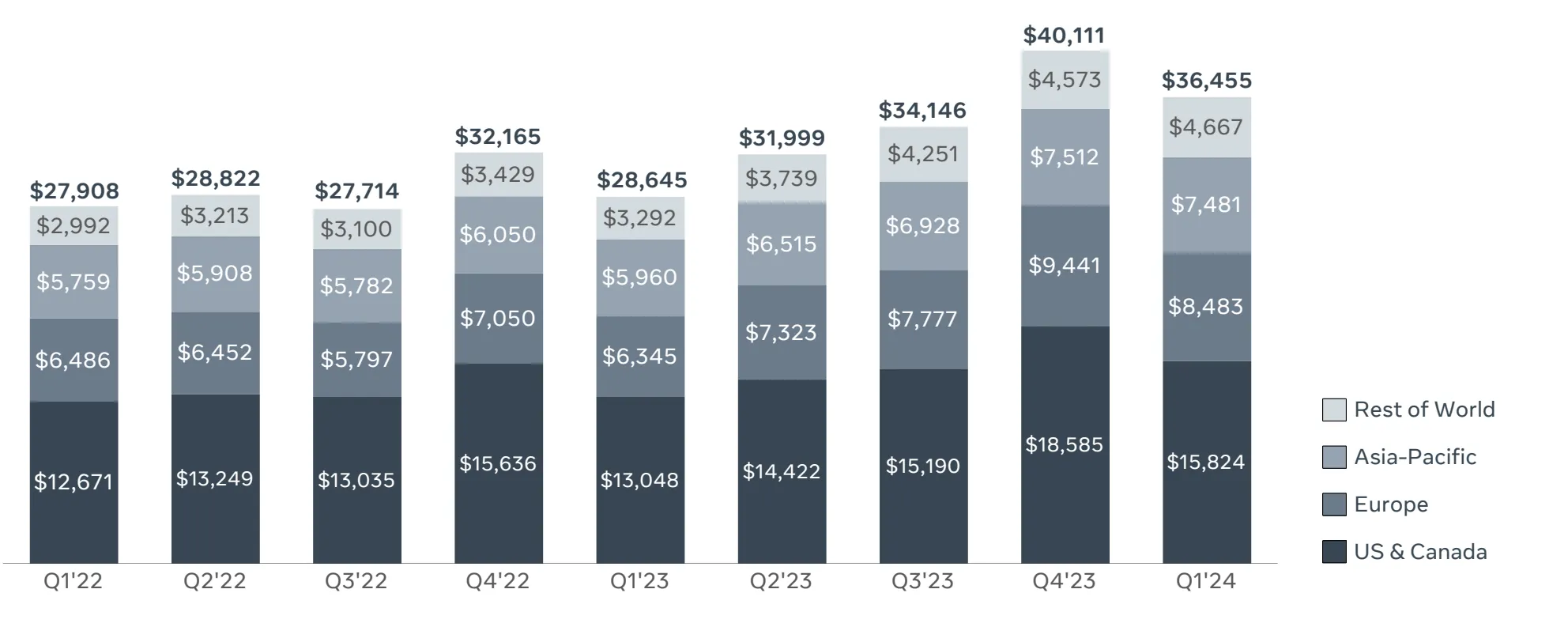

Before discussing what Meta could become, it is worth pausing to appreciate what Meta already is. The company generated $36.5 billion in revenue in Q1 2024 alone, up 27% year-over-year - its fastest rate of expansion for any quarter in three years. This growth is not coming from one geography or one product. It is broad-based and accelerating.

The geographic breakdown tells a story that many investors underappreciate. While the US & Canada segment remains Meta’s largest revenue contributor at $15.8 billion, the real acceleration is happening internationally. Europe delivered $8.5 billion (up 34% YoY), Asia-Pacific contributed $7.5 billion (up 41% YoY), and the Rest of World segment surged to $4.7 billion - a staggering 42% year-over-year increase. This is a company that has barely begun to monetize its international audience at rates approaching US levels.

What makes these numbers structurally important is the context of the broader digital advertising market. According to Precedence Research, global digital advertising spend stood at approximately $550 billion in 2023 and is projected to exceed $1.36 trillion by 2033, implying a CAGR of 9.58%. Meta does not need to take market share to grow - the pie itself is expanding at nearly double-digit rates as traditional advertising budgets continue their migration online. Yet Meta is simultaneously benefiting from both the expanding market and its own share gains through superior AI-driven ad targeting.

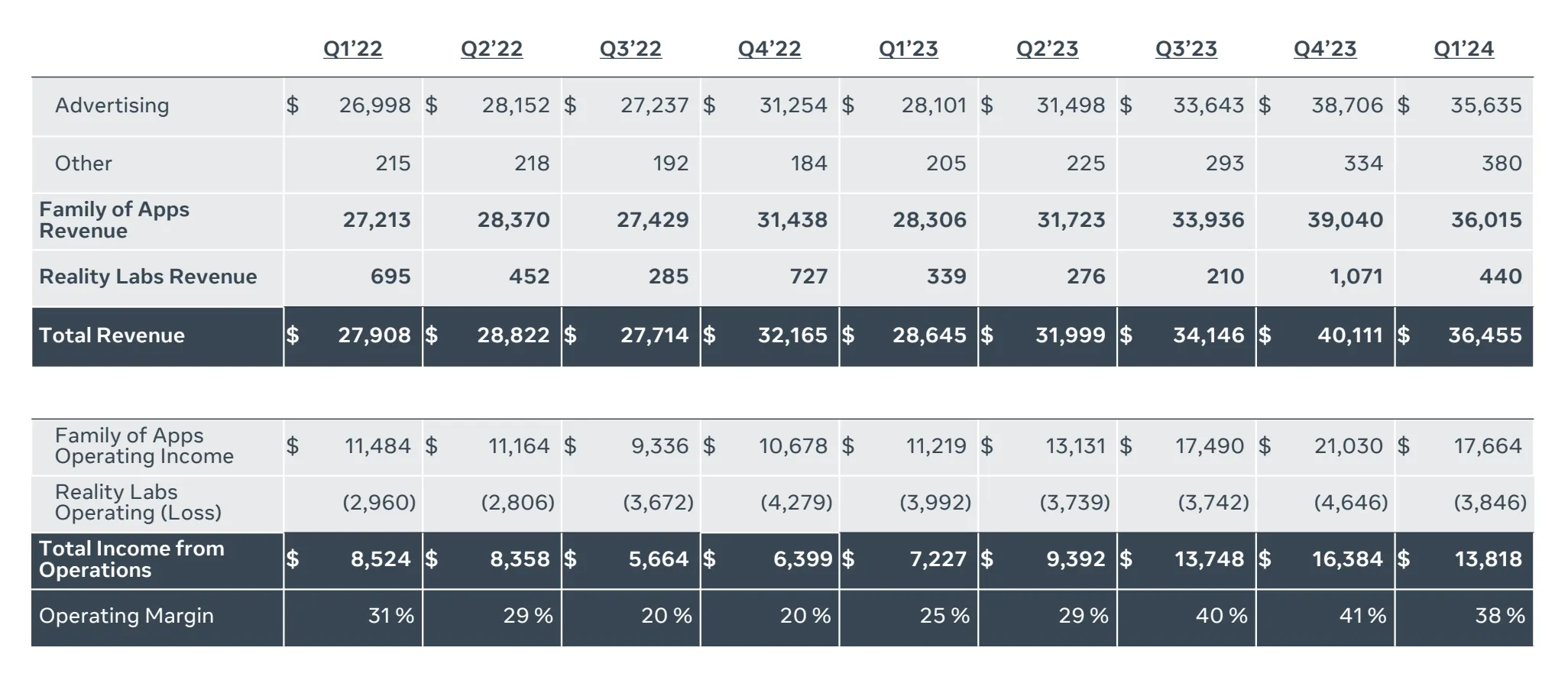

The segment-level data makes the core economics strikingly clear. Family of Apps - Facebook, Instagram, WhatsApp, and Messenger combined - generated $36 billion in revenue and $17.7 billion in operating income in Q1 2024, representing an operating margin of 49.2%. That is nearly 1,000 basis points of expansion year-over-year. This is not a company struggling to find profitability; it is a company whose core business is among the most profitable operations in the history of technology.

Advertising accounts for 97.8% of total revenue. Some analysts frame this as a concentration risk. We see it differently: it means Meta has a singular, obsessive focus on making its advertising platform as effective as possible for the millions of businesses that depend on it. And the results speak for themselves.

3.24 Billion People and Counting

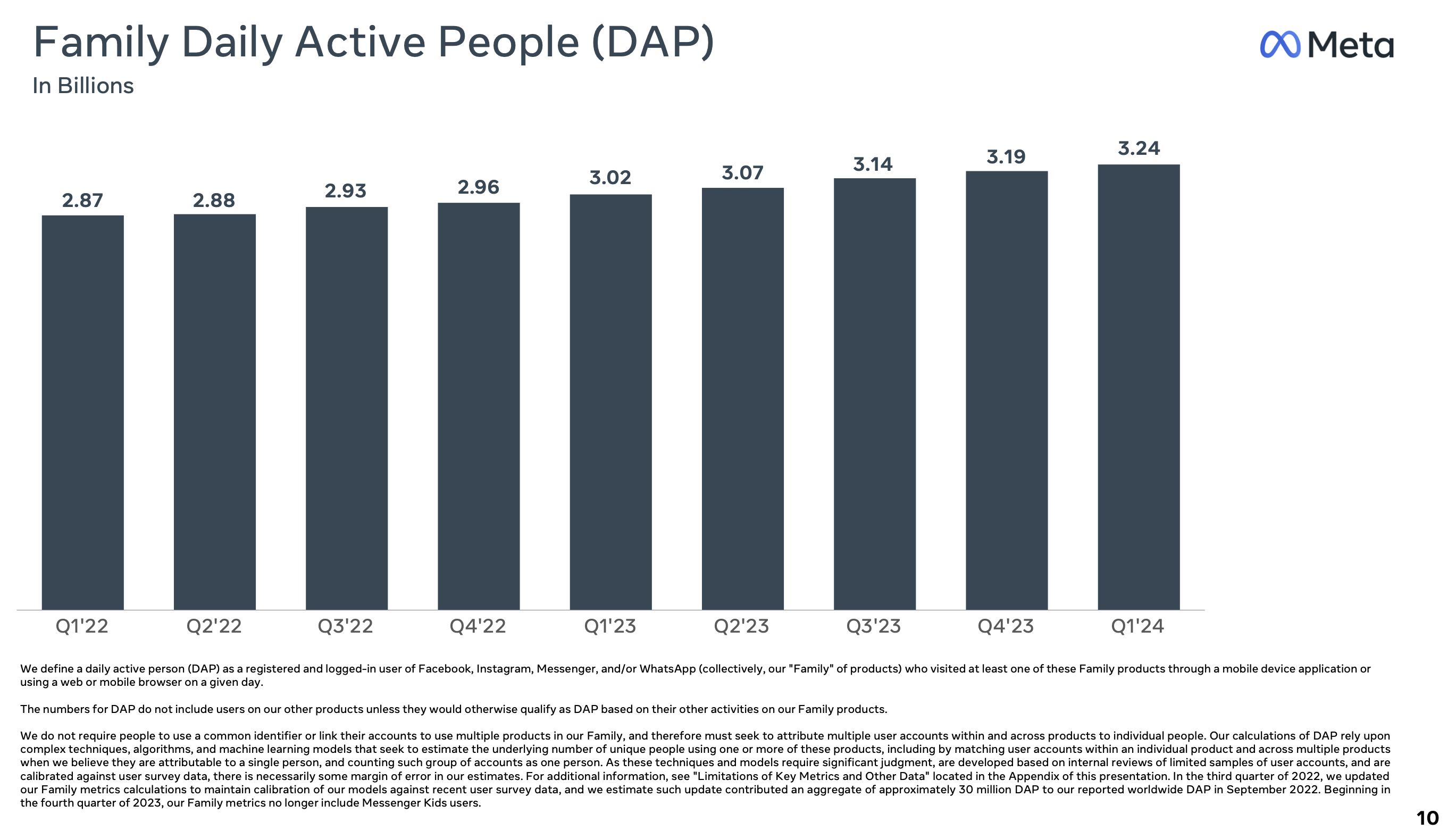

The moat around Meta’s business is not a technological secret or a patent portfolio. It is something far simpler and far more durable: 3.24 billion people use at least one Meta app every single day. That figure represents roughly 40% of the global population. There is no other company on Earth - not Google, not Apple, not Amazon - that commands this level of daily engagement with this many human beings.

What makes this metric even more remarkable is its trajectory. From Q1 2022 to Q1 2023, Meta added approximately 150 million daily active people. Over the subsequent twelve months, that number increased by 220 million - nearly 50% faster growth despite the already-massive base. The narrative that Meta’s platforms are “aging” or “losing relevance” simply does not survive contact with the data.

The competitive dynamic here is fundamentally different from what we see in cloud computing, search, or e-commerce, where the major big tech companies constantly encroach on each other’s territory. Microsoft can compete with Google in search. Amazon can compete with Microsoft in cloud. Google can compete with Amazon in advertising. But none of them can compete with Meta in social networking. The network effect is simply too powerful. Every person who joins makes the platform more valuable for every other person already there, creating a self-reinforcing cycle that no amount of engineering talent or capital can easily replicate.

No one has been able to break this dominance. Remember when Snapchat introduced Stories? Instagram adopted the feature, and Snapchat’s growth trajectory never recovered. When Twitter stumbled, Meta launched Threads - which accumulated 100 million users faster than any app in history. When Apple implemented its iOS privacy changes in 2022, Wall Street declared Meta’s ad business permanently impaired. Within eighteen months, Meta had rebuilt its measurement and targeting stack using AI, and revenue growth reaccelerated from near-zero to 27%.

There is one competitor that has genuinely challenged Meta: TikTok. ByteDance’s short-video platform captured a meaningful share of attention among younger demographics. But even here, the story is more nuanced than the headlines suggest. Despite TikTok’s rise, Meta still managed to grow its daily active people by 370 million over two years. And critically, President Biden signed a bill on April 24, 2024 that could potentially force TikTok to divest from its Chinese parent company or face a ban. Whether TikTok is ultimately banned, divested, or continues operating under increased scrutiny, the regulatory headwinds are real - and every point of uncertainty for TikTok is a potential tailwind for Instagram Reels.

Perhaps the most underappreciated aspect of Meta’s competitive position is its relationship with China. Unlike virtually every other mega-cap tech company, Meta has no operational dependency on China. Facebook and Instagram are already banned there - it cannot get worse. But Chinese companies like PDD Holdings (Temu), Shein, and Alibaba spend billions on Meta’s platforms advertising their products to Western consumers. Meta can do without China, but Chinese e-commerce companies cannot do without Meta if they want to reach the West. That is an asymmetry worth paying attention to.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Meta Platforms, Inc. (NASDAQ: META) is subject to regulatory risk (EU Digital Services Act, GDPR, US antitrust), governance concentration risk (dual-class share structure), advertising market cyclicality, competitive risk from TikTok and emerging platforms, AI investment ROI uncertainty, and ongoing Reality Labs cash burn. The company generates virtually all revenue from digital advertising, making it sensitive to economic cycles and shifts in advertiser spending. The valuation frameworks presented rely on publicly available information and independent analytical models as of June 2024; actual results may differ materially. Mark Zuckerberg’s controlling stake means strategic direction cannot be changed by minority shareholders. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision.