Here is the situation in plain terms: Exxon Mobil - one of the most profitable energy companies on earth, a dividend champion that has raised its payout for over four decades, and a business generating tens of billions in operating cash flow - is sitting at a valuation multiple at the low end of its own historical range, at a moment when most investors have written it off because oil prices dipped.

Oil weakness is real. The headlines about OPEC production increases and softening demand are real. But what the market seems to be mispricing is the rest of the story: a massive natural gas business that is about to be turbocharged by a colder-than-expected winter, a transformational Guyana production ramp that adds long-duration low-cost barrels to the mix every year, a freshly permitted Golden Pass LNG terminal, and a balance sheet so solid that the company spent $9.8 billion buying back its own stock in just the first half of 2025.

The question isn't whether Exxon is a great company. It demonstrably is. The question is whether the current pessimism is creating a window - and we believe it is.

Snapshot - October 21, 2025

Key Figures at a Glance

Exxon Mobil needs little introduction. It is one of the largest publicly traded energy companies in the world, operating across the full spectrum of upstream (exploration & production), downstream (refining), and chemicals. What it does need is a re-examination right now, because the market's laser focus on oil price weakness is causing investors to miss quite a lot that matters.

The stock has been under pressure since oil prices slid from their 2022 peaks and have now settled in the low-$60s per barrel. That pressure is rational - lower oil prices do compress Exxon's upstream earnings. But Exxon is not a pure-play crude oil business. It is a diversified energy conglomerate with natural gas operations, a massive refining segment, a chemicals business, and a rapidly growing portfolio of new energy materials.

At the current entry zone of $XXX–$XXX, the stock's P/Cash flow multiple sits at the low end of its historical range - historically, that's the kind of entry that's paid off. The market is pricing in permanent impairment. That's not what the fundamentals show.

Oil prices hovering around $62 - creating investor pessimism that may be overdone.

Oil Down, Gas Up: The Dual-Force Dynamic

The narrative dominating Exxon right now is simple: OPEC is adding supply, trade tensions are weighing on demand, and oil prices could stay soft. That's the bear case, and it has some merit. What it ignores, however, is that Exxon is also one of the US market's most significant producers of natural gas - and the natural gas story heading into winter 2025 is a very different one.

"A large portion of the US is expected to face a colder-than-average winter in 2025 and 2026, with the Northern Plains, Great Lakes, and New England likely seeing the most intense cold - particularly in mid-January and mid-February."

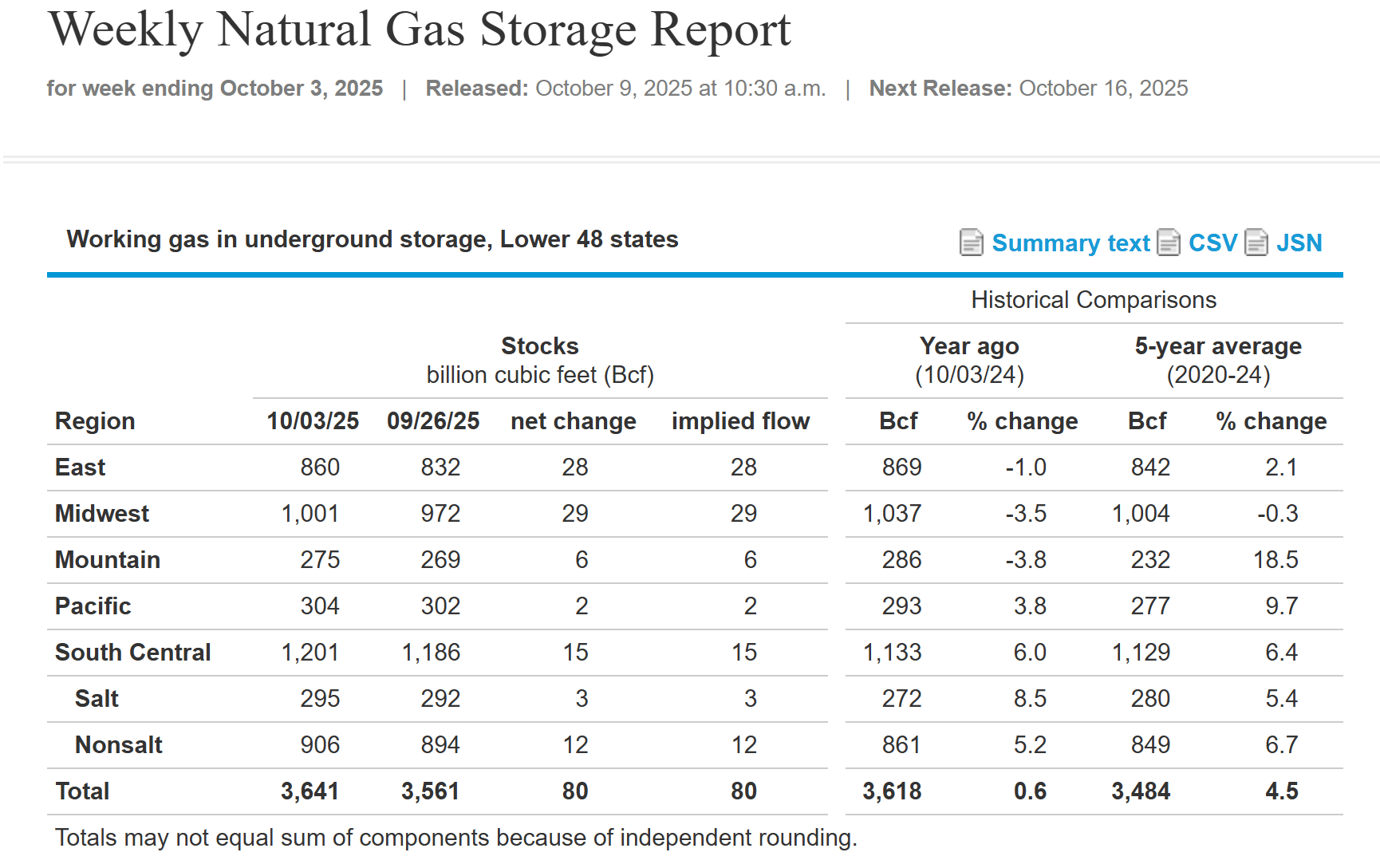

- Seasonal weather forecast consensus, Q4 2025Natural gas is currently priced around $3.32 per MBTU, roughly 10% below its five-year historical average of $3.67. But here's what matters: the current storage situation is much tighter than the headline number suggests. Working gas inventory across the lower 48 states stood at approximately 3,618 billion cubic feet as of early October 2025. That's only about 22 Bcf more than the same period last year - a buffer that sounds meaningful until you consider that residential NG consumption alone averages 12–13 Bcf per day, and in a cold month, that figure can more than double.

In other words, the margin of safety in storage is thin. A colder winter doesn't need to be dramatic to shift the demand-supply dynamics meaningfully. And when it does, natural gas prices respond quickly - which directly feeds into Exxon's earnings.

Run the numbers and it gets interesting fast. Exxon produces approximately 8.7 billion cubic feet of natural gas per day on average. Using a breakeven price of around $2.80/MBTU from its Permian operations, every $0.10 per MBTU increase in natural gas prices translates to roughly $0.08 in additional EPS for XOM. That's a lever that doesn't get discussed much - but in a year where gas could move from $3.32 toward $4.50–$5.00 on a cold-winter demand surge, that's a potential EPS boost of more than $0.90 to $1.10 per share. This re-rating toward $130–$135 assumes not just the EPS uplift but also a modest P/E expansion from approximately 13x to 14–15x as the market re-prices Exxon's improved earnings mix toward higher-margin natural gas - a reasonable expectation when commodity tailwinds drive outsized FCF generation. The broader target of $XXX–$XXX is supported by the full suite of catalysts described below.

The Natural Gas Math in a Cold Winter Scenario

Exxon NG production capacity: ~8.7 Bcf/day | Breakeven: ~$2.80/MBTU

Sensitivity: +$0.10/MBTU NG price → +$0.08 EPS for XOM

If NG rises from $3.32 to $4.50–$5.00 (plausible cold-winter scenario):

EPS uplift: +$0.96 to +$1.12/share → stock re-rating toward $130–$135 on this catalyst alone (incorporating both the EPS uplift and a modest P/E expansion from approximately 13x to 14–15x as the market re-prices Exxon's earnings mix).

Meanwhile, the oil price headwind is real but not necessarily terminal. The market is pricing in a prolonged soft-oil environment, which is one legitimate scenario. But it is not the only scenario. A re-escalation of Middle East tensions, a reversal of OPEC production decisions, or simply a colder-than- expected winter boosting fuel oil demand could all shift the oil picture faster than consensus expects. Exxon doesn't need a dramatic oil recovery to hit our target - it just needs natural gas to do its thing and the market to stop pricing the stock as if earnings will permanently be near their current trough.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Exxon Mobil Corporation (NYSE: XOM) is subject to commodity price risk, geopolitical risk, regulatory risk, and general market risk. The price targets, EPS sensitivity analyses, and valuation frameworks cited in this tip are based on publicly available information and independent analytical models as of October 2025; actual results may differ materially. Natural gas price forecasts and winter weather projections are probabilistic - cold weather scenarios are not guaranteed. Oil price assumptions reflect conditions as of the tip date and are inherently unpredictable. Dividend continuity, while historically supported by Exxon's financial strength, is not guaranteed. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision. The authors and publishers are not responsible for any financial losses resulting from the use of this information.