I've been watching European natural gas inventories all year, and the chart keeps telling the same story the market refuses to hear. Storage levels have run 10% below the five-year average for twelve consecutive months. Russia, which used to supply roughly 40% of Europe's gas, has been effectively cut off. Asia is competing for the same LNG cargoes. And yet the TTF spot price has actually fallen since the heating season began - down about 12%. That's not fundamentals. That's complacency.

Meanwhile, the company that has quietly become Europe's most important remaining gas supplier is trading at 8.8x forward earnings and paying you nearly 8% to wait. Equinor grew production 7% year-over-year to 2,130 thousand barrels of oil equivalent per day. It generated $14.7 billion in cash flow through nine months. It returned $9 billion to shareholders - a ~15% total yield - while keeping its balance sheet at just 12.2% net debt with $22.4 billion in cash. And the stock has gone roughly nowhere.

I started building this position because I believe the market is making a mistake it has made before: pricing a dual-engine energy company as though both engines are permanently broken. They are not. European gas is structurally tighter than the spot price suggests, and the global oil market may have far less spare capacity than institutional estimates assume. You do not need both of those catalysts to fire for this trade to work - but if they do, the repricing will be significant. $XX.XX–$XX.XX is where I've been adding. That's not a premium price for what you're getting.

Equinor at a Glance

If you know Equinor only as "that Norwegian oil company," you are already underestimating it. Yes, it's majority-owned by the Norwegian government (67%), headquartered in Stavanger, and it operates across more than 30 countries. But what makes it genuinely interesting - and genuinely different from its peers - is that it is not an oil company or a gas company. It is both, in roughly equal measure, sitting in one of the most geopolitically stable and tax-transparent jurisdictions on earth. In an era of rising resource nationalism, the market keeps underpricing exactly that.

Think of Equinor as a dual-engine machine. One engine runs on European natural gas - where the company is the continent's dominant remaining supplier. The other runs on crude oil, with world-class fields like Johan Sverdrup producing at near-perfect regularity. There is also a growing, if still modest, renewables portfolio - Dogger Bank offshore wind in the UK, Empire Wind in New York - that positions the company for the energy transition without betting the house on it. Suncor is pure oil. Cheniere is pure gas. Neither can do what Equinor does from a single position.

I keep coming back to the valuation, because it does not make sense to me. At 8.8x forward earnings, Equinor trades at a meaningful discount to both Suncor (13x) and Cheniere (11x) - despite offering a higher dividend yield, more commodity diversification, and superior geopolitical stability. The Norwegian government's majority ownership ensures policy continuity and eliminates the capital allocation volatility that can plague companies with activist shareholders or speculative management. There is no drama here, no empire-building CEO, no shareholder activism. This is a company that does what it says it will do, quarter after quarter. And somehow, it's the cheapest of the three.

The European Gas Thesis - Tighter Than You Think

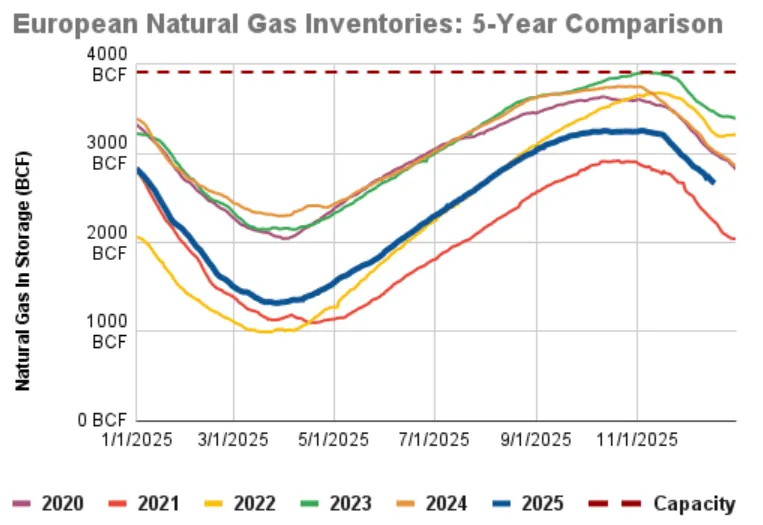

If I had to pick one chart to explain why I'm buying Equinor, it would be the European natural gas inventory chart below. It tells a story that the spot market has stubbornly refused to acknowledge: Europe is structurally short on gas, and the buffer is thinner than it has been at any point since the energy crisis of 2022.

As the chart shows, Europe's natural gas storage levels have been trending below the five-year average for the entire year. We are currently approximately 10% below those levels - not a crisis, but a vulnerability. The storage level heading into winter 2025/2026 sits around 83%, which is 12 percentage points below where it was at the same point last year. As Equinor's CFO Torgrim Reitan noted on the Q3 earnings call: the market seems tighter than many actually think. A cold winter could have a significant impact on pricing.

The classic cold-winter catalyst has not materialised in the early weeks of the 2025-26 heating season - TTF has actually declined roughly 12% since October as temperatures tracked seasonal norms. This is not a defeat for the thesis; it simply means the weather optionality has not been exercised yet. The more durable setup is the structural storage deficit entering the 2026-27 refill season. Storage running approximately 10% below the five-year average means Europe faces a more demanding injection season in spring and summer 2026 - demand for refilling storage at below-average levels provides a more reliable, less weather-dependent price catalyst than any single cold snap. A mild winter doesn't fix any of this. It just pushes the reckoning into spring.

"In the short term, this winter, the market seems tighter than many actually think. We are on a storage level around 83%, which is 12 percentage points below last year. If we see a cold winter, it can really have a significant impact on the market."

- Torgrim Reitan, Equinor CFO, Q3 2025 Earnings CallBut the more important story isn't this winter at all. Russian pipeline gas to Europe has been reduced to a trickle. The potential sanctioning of Russian LNG - approximately 17 billion cubic metres - would further tighten the European market. Meanwhile, new LNG supply from the US and Qatar, while significant, is not arriving as quickly as projected, and Asian demand is growing at approximately 3% per year, competing for the same cargoes. Equinor's cost position - at roughly $2/MMBtu for Norwegian gas delivered into an $11/MMBtu European market - provides an enormous margin of safety regardless of where spot prices settle.

The Oil Wildcard - OPEC+ Spare Capacity Fiction

I want to be upfront about the oil side of the thesis: the consensus narrative is bearish, and for understandable reasons. OPEC+ is adding 2 million barrels per day back into the market. The EIA forecasts persistent oversupply. Prices have drifted down nearly 20% year-to-date. For Equinor, which derives approximately half its revenue from oil-related products and services, this has been a headwind - and it's the main reason the stock has gone nowhere.

But I have been studying OPEC+ spare capacity numbers for some time now, and I think the consensus may be significantly wrong on one critical variable. The EIA estimates over 4 million barrels per day of spare capacity - a number that, if true, would cap oil prices for years. The problem is that this estimate has a poor track record. When the Saudis and OPEC were called upon to stem the oil price surge in 2007–2008 that ended near $150/barrel, the promised spare capacity simply did not materialise. They failed to produce it, because it didn't exist in the quantities they claimed.

What's striking is how much OPEC and the EIA disagree on where the market actually is. The gap between OPEC's estimate of a modest 0.4 mb/d surplus in Q3 and the EIA's estimate of a 2.5 mb/d glut in the same period is enormous - roughly 2 million barrels per day of disagreement. This is not a rounding error; it is a fundamental dispute about the state of the oil market. The truth is likely somewhere in between, which means the surplus is meaningfully smaller than the bearish consensus assumes.

None of this requires certainty. The oil market doesn't need to boom for this trade to work. The gas side alone justifies the position. But if the bears are wrong about oil - if OPEC+ has largely exhausted its real spare capacity, if demand continues to grow at approximately 1 mb/d per year, and if the decline in US drilling activity is the market's own way of signalling that current prices are too low - then the oil leg of Equinor's revenue base becomes a powerful bonus catalyst. It's the difference between a solid return and an exceptional one, and the market has not priced in any probability of the upside scenario.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Equinor ASA (NYSE: EQNR) is subject to commodity price risk (oil and natural gas), geopolitical risk, currency risk (NOK/USD), Norwegian tax regime risk, operational risk related to offshore production, and general market risk. Natural gas prices in Europe are highly volatile and may not follow the seasonal or structural patterns described herein. Oil prices are influenced by OPEC+ decisions, global demand dynamics, and geopolitical events that are inherently unpredictable. Norwegian withholding tax on dividends for non-resident shareholders may reduce effective dividend yields; investors should consult a tax advisor regarding their specific situation. The scenario analysis and financial estimates are based on publicly available information and independent analytical models as of January 2026; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision.