There is a particular kind of opportunity that appears only when the market is looking elsewhere. Boeing is embroiled in quality scandals and production shortfalls. Airbus is sold out until the end of the decade. And somewhere in São José dos Campos, Brazil, the world’s third-largest aircraft manufacturer is quietly posting its highest backlog in seven years, watching its margins inflect upward for the first time since the pandemic, and preparing to collect on a decade of product development that nearly ended in a fire sale to Boeing.

Embraer is entering what its own CEO calls “harvest season.” The company spent the last five years restructuring, deleveraging, and refreshing its product portfolio after Boeing walked away from a $4.2 billion deal in 2020, leaving Embraer with $300 million in sunk costs and a bruised reputation. What followed was a turnaround that the market has only partially recognized: a $21.1 billion backlog, an S&P upgrade to investment grade, and four business segments all pointing in the same direction for the first time in the company’s history.

This briefing examines why Embraer at $XX–$XX is a risk/reward setup that stands out in the aerospace sector right now. The thesis rests on four engines - commercial aviation recovery, executive jet dominance, C-390 military expansion, and high-margin services - each independently capable of driving the stock higher, and collectively pointing toward a re-rating that the consensus has not yet priced in.

To understand Embraer’s current opportunity, you need to understand what nearly killed the company. In 2018, Boeing agreed to acquire 80% of Embraer’s commercial aviation division for $4.2 billion. The deal would have effectively ended Embraer as an independent planemaker. Then the 737 MAX crashes happened. The pandemic hit. And in April 2020, Boeing terminated the agreement, leaving Embraer holding the bill for roughly $300 million in carve-in/out costs and posting a $121 million loss in Q3 2020.

It was, in retrospect, the best thing that ever happened to the company.

Forced to stand on its own, Embraer’s management under CEO Francisco Gomes Neto launched an aggressive turnaround: cutting costs, deleveraging the balance sheet, and investing in the product portfolio they had nearly sold for parts. The results have been quietly spectacular. Net Debt/EBITDA fell from 2.3x in 2022 to 1.4x in 2023. S&P upgraded the credit rating to investment grade BBB−. Free cash flow hit $318 million in 2023 - more than double the guidance of $150 million. And the backlog swelled to $21.1 billion, the highest level in seven years, driven by orders across all four segments.

“For now, we have a very young and competitive portfolio of products developed in less than 10 years and we are in a good moment. We want to sell those products and improve our financial performance.”

- Francisco Gomes Neto, CEO, EmbraerThe CEO’s choice of words is deliberate. “Harvest season” means no expensive new aircraft development programs that would drain cash flow and distract management. Instead, the company is focused on monetizing its existing E2 commercial jets, Phenom and Praetor executive aircraft, C-390 military transporter, and a rapidly growing services business. This is a capital-light, cash-generative phase of the cycle - precisely the phase where aerospace companies re-rate.

Meanwhile, Embraer’s two largest competitors are creating a vacuum. Boeing’s ongoing quality and production struggles have reduced its output and consumer confidence. Airbus has its production sold out for the better part of the decade. Airlines need aircraft. They cannot wait five years for a delivery slot from Toulouse or Seattle. Embraer has production available from 2026 onward - and the world is starting to notice.

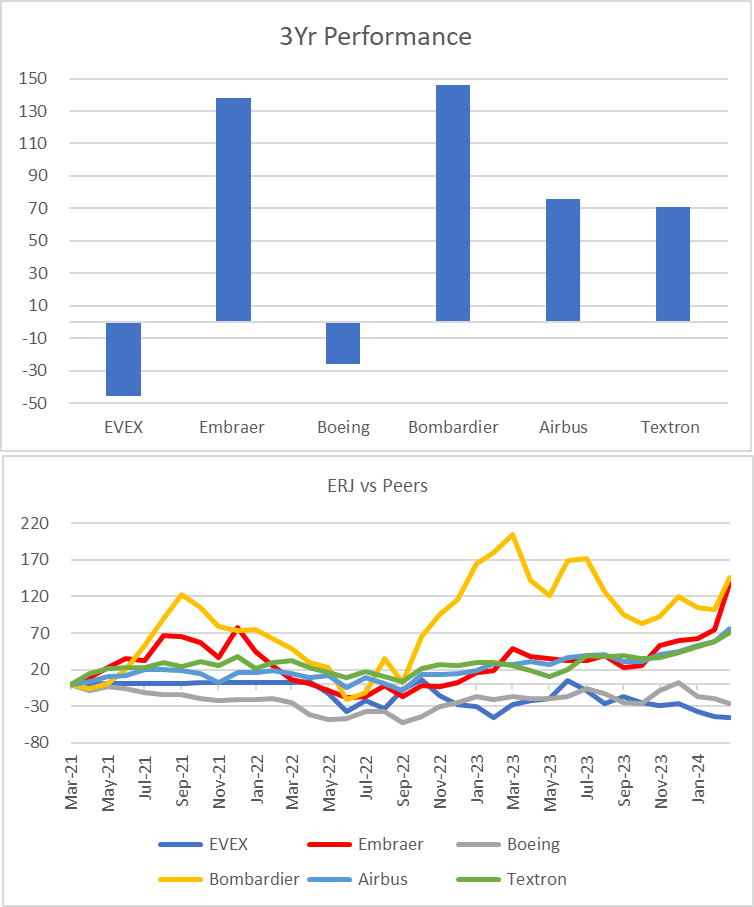

The stock has already moved - up roughly 130% from its mid-2022 bottom - but the thesis is not about what has happened. It is about what is still not priced in. Specifically: the NetJets optionality worth up to $5 billion that sits outside the disclosed backlog, the C-390’s $60 billion addressable market with only seven aircraft delivered to date, the Pratt & Whitney GTF engine contract that could add $500 million in annual high-margin services revenue, and a potential Boeing arbitration resolution. Each of these represents a catalyst the consensus has not fully modeled.

Embraer is the undisputed leader in commercial jets with up to 150 seats. Its E-Jet family - spanning the E170, E175, E190, and E195 - is the backbone of regional aviation worldwide, operated by carriers including Delta, American Airlines, JetBlue, Austrian Airlines, and Aeromexico. The newer E2 generation (E190-E2 and E195-E2) offers 17.3% lower fuel burn than its predecessor, fly-by-wire controls, 120-minute ETOPS certification, and what the company claims is the best seat-mile cost among all single-aisle jets.

The commercial segment has been the slowest to recover from the pandemic, with deliveries falling from a peak of 162 jets in 2008 to just 44 in 2020. But the trajectory is now firmly upward: 48 deliveries in 2021, 57 in 2022, 64 in 2023, and guidance for 72–80 in 2024. Management expects to approach “very close back to the three digits” in 2025 - a statement that implies approximately 90–100 deliveries, restoring production rates not seen since 2014.

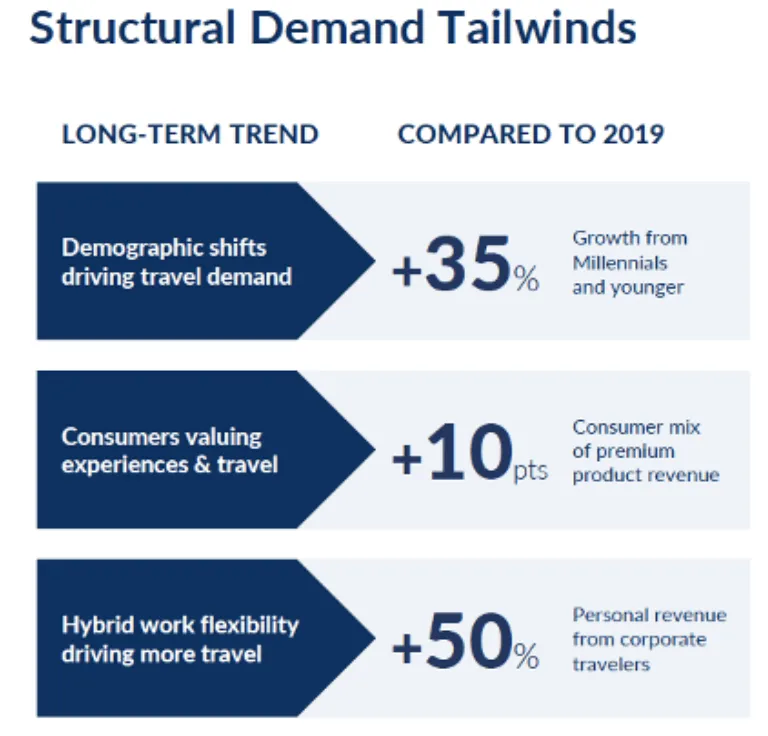

The catalyst for this acceleration is twofold. Structural demand is the first part. Global revenue passenger kilometers (RPK) are expected to increase 9.8% in 2024, surpassing even the 4.5% growth seen in pre-pandemic 2019. Delta Air Lines’ Investor Day data reveals that demographic shifts - Millennials and younger cohorts - are driving 35% more travel demand compared to 2019, while hybrid work flexibility is generating 50% more personal revenue from corporate travelers.

The supply constraint is the other half. Boeing and Airbus are capacity-constrained, unable to fulfill existing orders let alone take new ones for near-term delivery. This creates a structural opening for Embraer. American Airlines’ landmark order for 90 E175 aircraft (plus options for 43 more) - the largest single Embraer order since 2016 - was not an act of charity. It was a rational decision by a major carrier that needed planes it could actually receive.

“We currently have concrete sales campaigns for more than 200 aircraft across the world for both our E1 and E2 jet families.”

- Francisco Gomes Neto, CEO, Q1 2024 Earnings CallIn the US regional market, Embraer enjoys a unique protective moat: union agreements that limit regional jet weight to 39 tonnes. The E2 series is heavier and cannot compete in this segment, but the E175 can - and it dominates. By 2030, an average of 40 aircraft in the sub-76-seat category will be retired annually in the US, creating a predictable replacement cycle that Embraer is uniquely positioned to capture. The company is also targeting the aging Bombardier CRJ 700/900 fleet, expanding its addressable market beyond just E1 replacements.

Internationally, the E195-E2 is finding traction. China’s CAAC has certified the E2, opening the world’s fastest-growing aviation market. Singapore’s carriers are using E2s to open new routes and increase frequency. The aircraft’s 6-hour range and ETOPS certification give it operational flexibility that many airlines find compelling as a complement to their narrowbody fleets.

The commercial segment posted just 1.1% EBIT margins in 2023, but this is a high-fixed-cost business where margins leverage sharply with volume. Management targets 3–4% EBIT margin in 2024, rising to 5–6% as deliveries scale. By 2026, NHM Capital estimates the segment could generate approximately $150 million in adjusted EBIT versus just $20 million in 2023 - a 7.5x increase driven primarily by volume, not pricing. The historical margin profile for Embraer’s commercial division was “double-digit territory in the mid-teens” at peak production - a level that current volume trends suggest is achievable again by the late 2020s.