Bitcoin mining companies that trade on public exchanges sit in this weird interstitial space in financial markets. Their revenues live and die with Bitcoin's price. Their cost structures? Dictated by electricity markets and semiconductor supply chains - two worlds that couldn't care less about crypto sentiment. And their stock prices end up reflecting what institutional money thinks about the sector's near-term direction, often before the broader market catches on. I've watched these stocks move 5, 10, sometimes 15 days ahead of Bitcoin itself. So the question keeps coming up: can mining stock behaviour actually signal when a correction is brewing?

Here is what makes this question worth revisiting right now. In the first two weeks of January 2025, JPMorgan's mining research desk reported that 12 of the 14 mining stocks they track outperformed Bitcoin. The combined market cap of those 14 US-listed miners jumped by $4.5 billion. Riot Platforms alone gained 32%. The signal works in both directions - when miners are quietly surging ahead of Bitcoin, that is institutional capital front-running optimism just as reliably as it front-runs fear. Understanding why requires knowing how this $15 billion-a-year machine actually works.

The $15 Billion Machine

Before the predictor thesis means anything, you need to understand the economics underneath it. Bitcoin mining is conceptually simple but operationally immense. Specialized computers compete to guess a random number, and the machine that guesses correctly first earns the right to update the blockchain and collect the block reward. No shortcuts exist. No clever algorithm speeds up the search. It is pure brute force - like rolling a trillion-sided die over and over until the right number comes up.

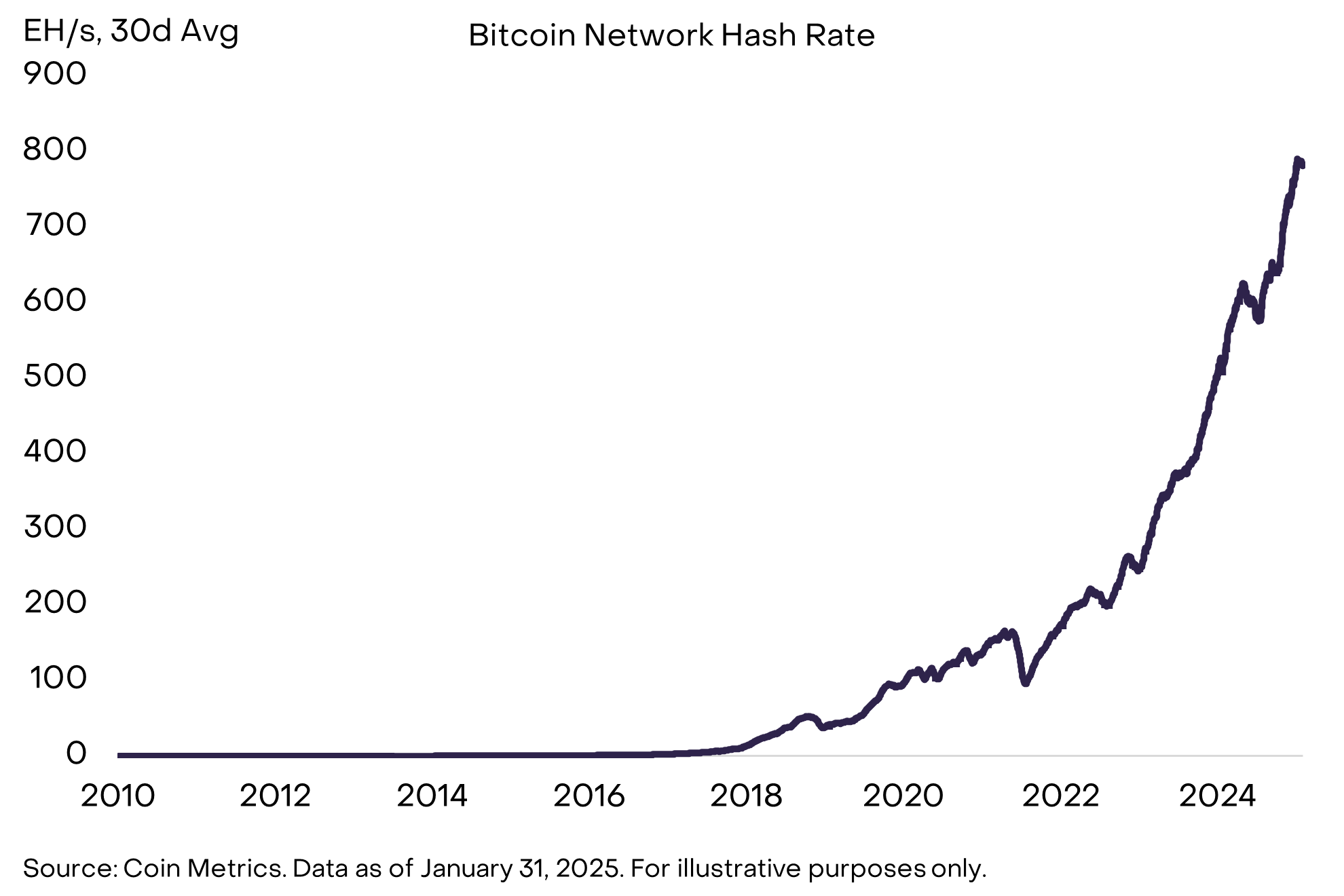

The scale of this guessing game is almost impossible to grasp. According to Grayscale Research, the Bitcoin mining network currently produces hashes at a rate of 765 exahashes per second. An exahash is one quintillion hashes. So miners are collectively performing more than 700 quintillion calculations every second. For perspective, scientists estimate there are approximately 7.5 quintillion grains of sand on Earth. Bitcoin miners blow past that number roughly every ten seconds.

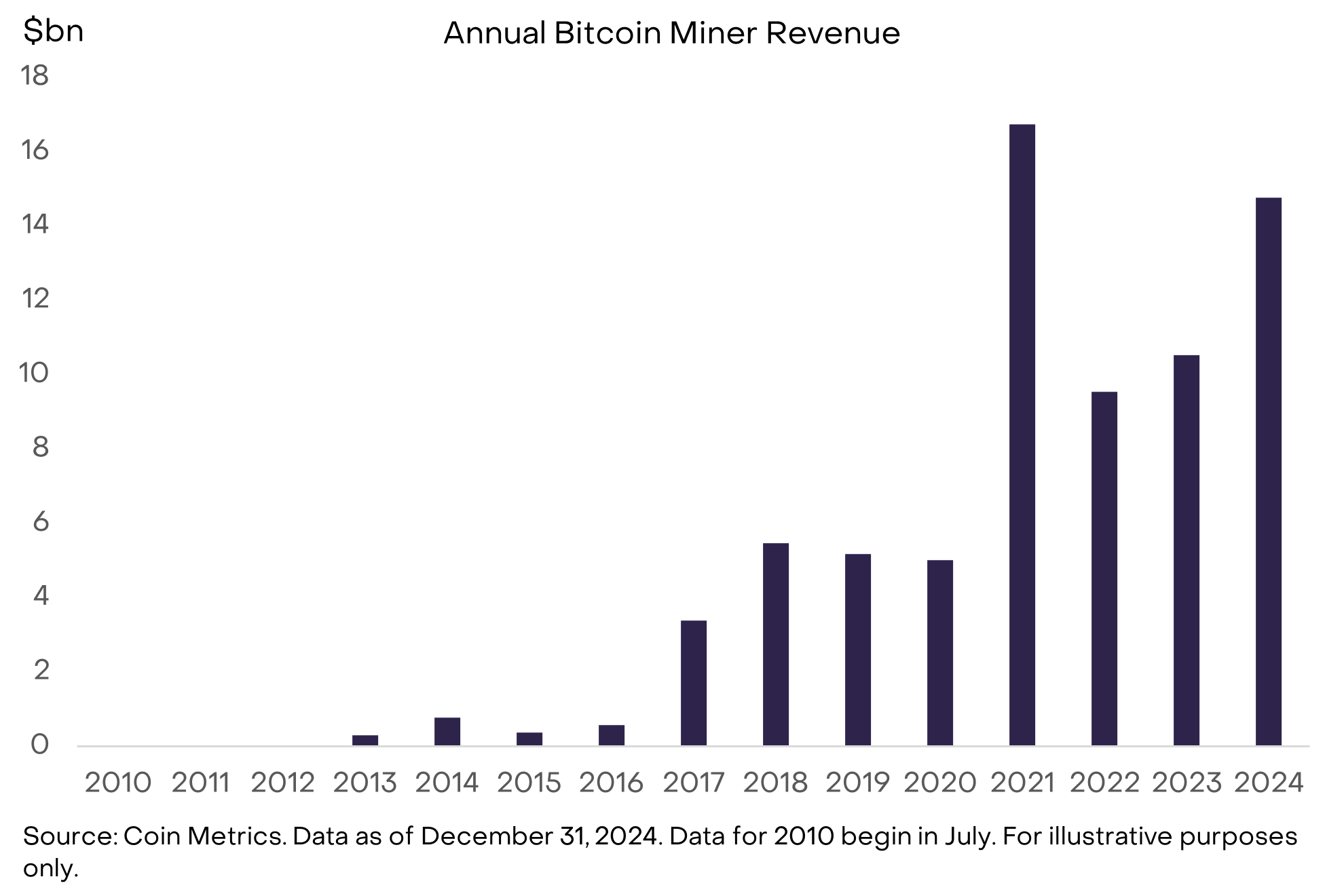

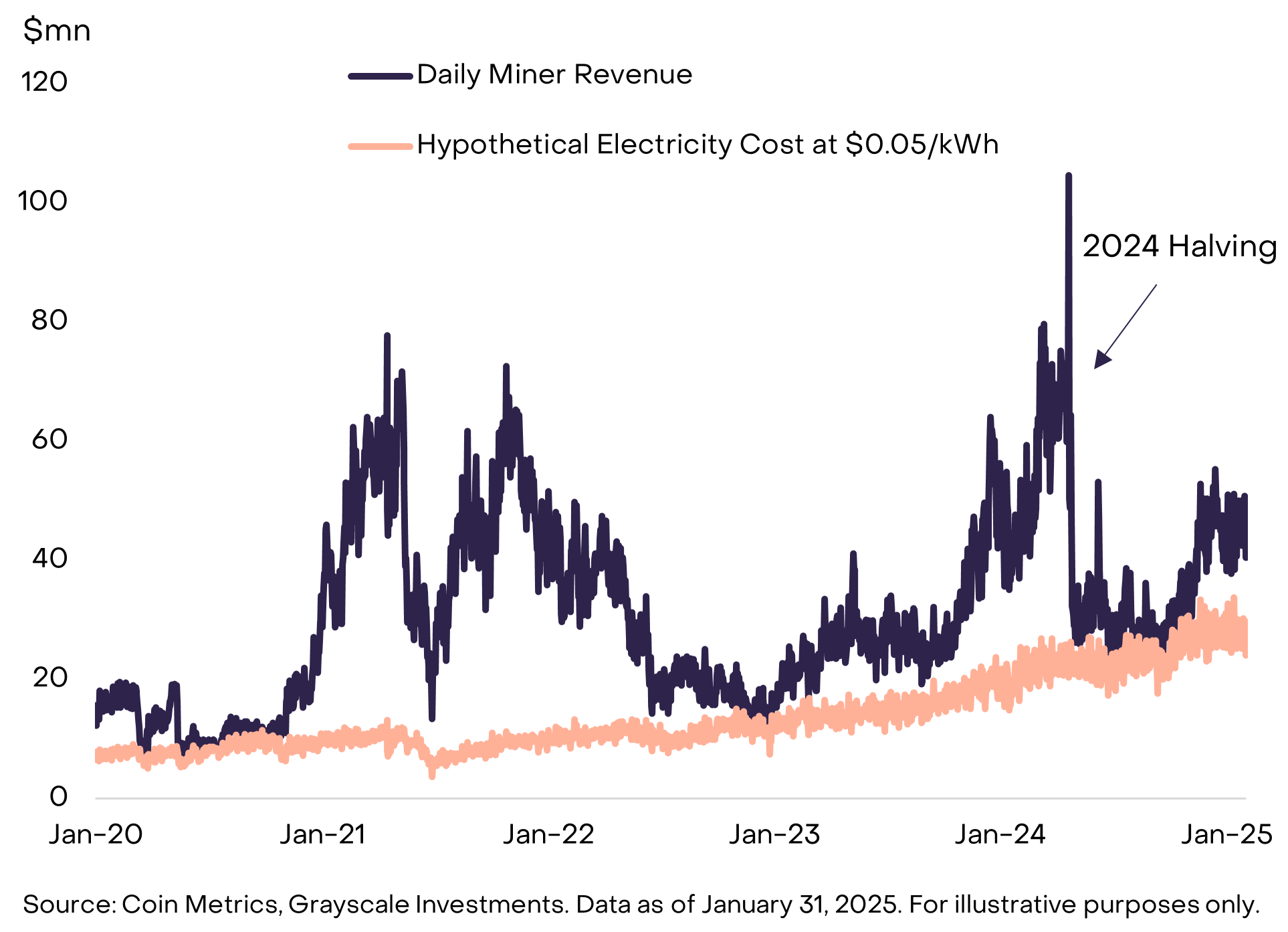

And they get paid handsomely for the effort. In 2024, miners collectively earned about 230,000 Bitcoin valued at nearly $15 billion. That represents a 34% compound annual growth rate from essentially zero in 2014 - a decade of explosive revenue growth despite the block reward getting cut in half every four years. The halving mechanics should theoretically shrink revenue. They haven't, because Bitcoin's dollar price has more than compensated each time. So far.

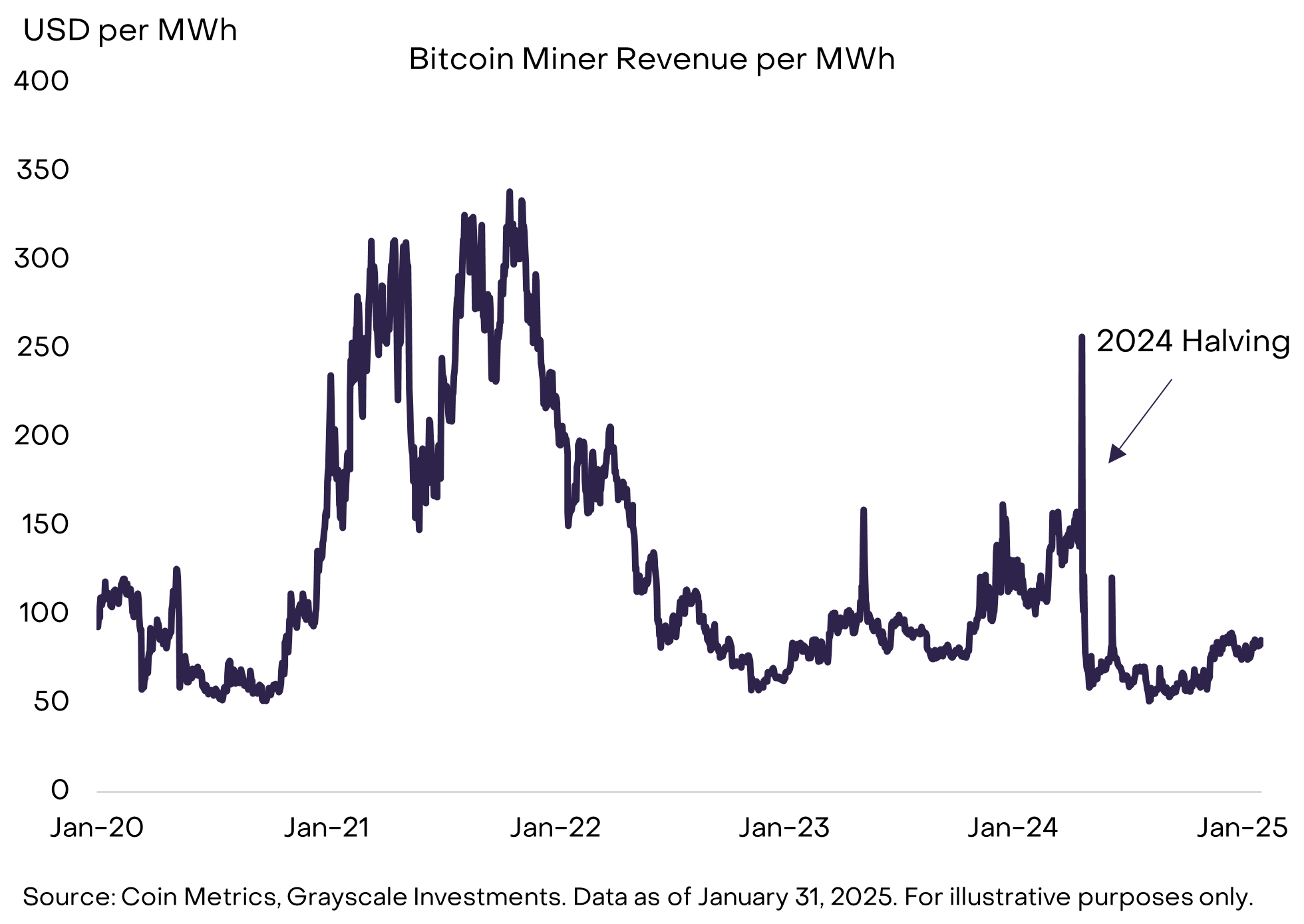

But revenue is only half the picture. Every miner pays for electricity, and the spread between what they earn per megawatt-hour and what they spend determines whether the business model holds up. Grayscale's data shows that at a hypothetical electricity cost of $0.05 per kilowatt-hour, aggregate miner operating margins have fluctuated wildly around halving events but generally recovered within months. The more intuitive metric - miner revenue per MWh consumed - has actually been broadly stable over the past two years, despite the April 2024 halving. That surprised me. The machines got more efficient at roughly the pace the rewards shrank.

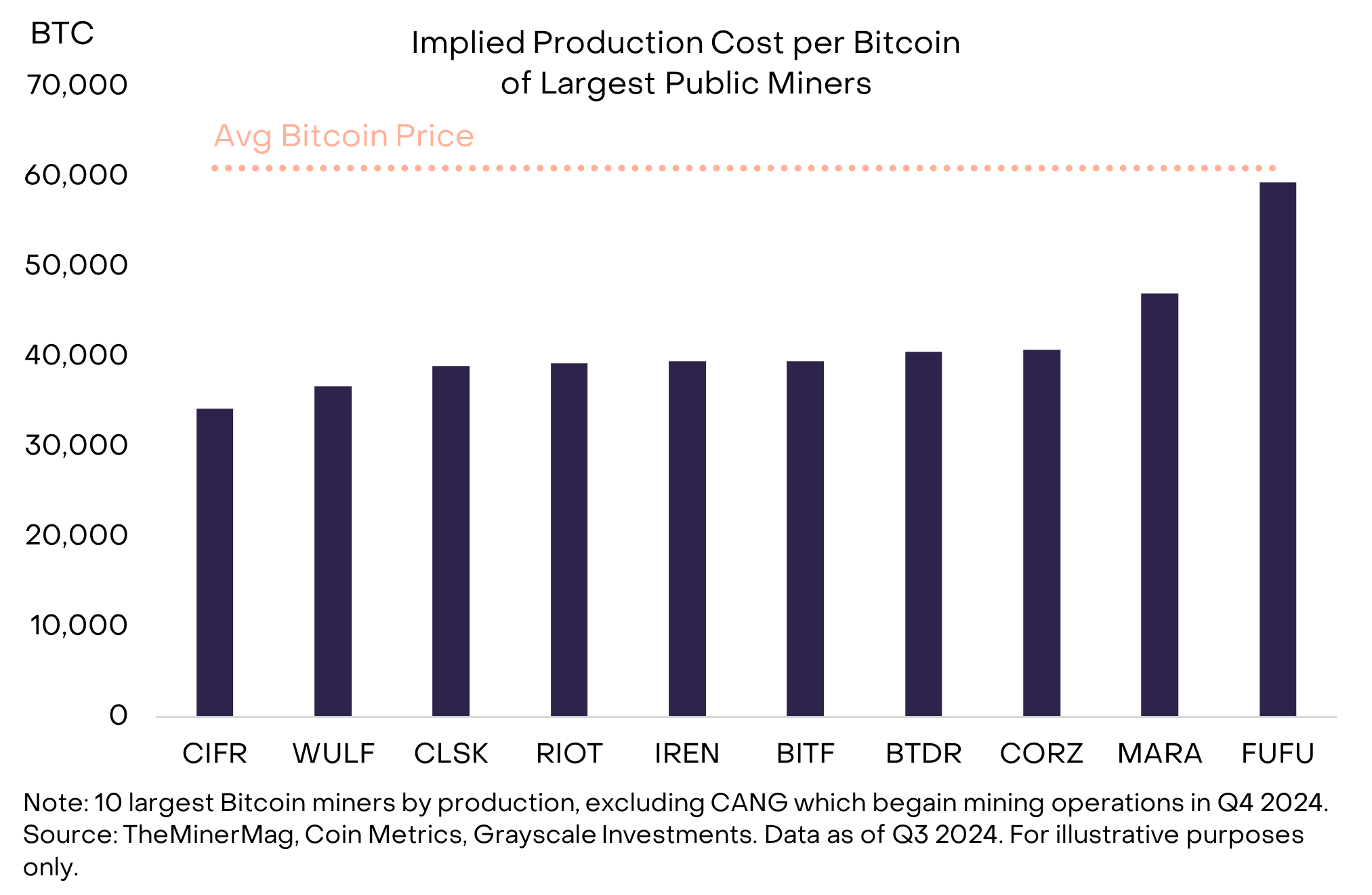

Production costs tell the most revealing story. During Q3 2024, the largest publicly traded miners produced Bitcoin at costs ranging from $34,000 to $59,000 per coin. The average Bitcoin price that quarter was $61,000. Some miners had comfortable margins. Others were operating right at the edge. That range - $34k to $59k - is what equity analysts are watching when they decide whether to buy or sell mining stocks. And it is exactly why those stocks move before Bitcoin's spot price does. When analysts can see margin compression coming, they don't wait.

Why does this matter for the predictor thesis? Because mining stocks aren't just proxies for Bitcoin's price. They are equity instruments priced on forward earnings, and forward earnings in mining are a function of hash rate, difficulty, energy costs, and hardware efficiency. Institutional holders model these variables continuously. When the model breaks, they sell. Sometimes weeks before the spot market catches on.

The Historical Evidence: When Miners Moved First

The mechanism isn't complicated. Institutional investors holding mining equities react to deteriorating fundamentals - rising energy costs, increasing difficulty, regulatory smoke - before the retail-heavy spot market fully prices in those risks. When big shareholders start trimming, that selling pressure hits equity markets first. You get a measurable divergence from Bitcoin's price, and it persists for days or even weeks before crypto catches up. Mining stocks are the canary. The coal mine is whatever correction is brewing underneath.

Go back through the major corrections since 2020 and a pattern shows up. Not a clean one - nothing in crypto is ever clean - but it is there. In multiple instances, mining stocks started rolling over before Bitcoin's spot price broke down. Equity analysts had access to forward-looking data on energy costs, hash rate trends, and profitability. They repositioned while retail was still posting rocket emojis.

Mining Stocks Led by ~10 Days

Mining equities started sliding in early May as reports of Chinese regulatory crackdowns circulated through institutional channels. Bitcoin's spot price? Still holding its range. It didn't break decisively until mid-May, and the full crash to ~$30,000 took weeks. But miners with Chinese exposure were already getting hammered. Smart money saw it coming.

Mixed Signal - Concurrent Decline

Mining stocks and Bitcoin peaked within days of each other around the $69,000 all-time high. No meaningful advance warning from the miners. But here is what was interesting - mining stock trading volumes surged before the broader market recognised the reversal. Prices moved in tandem. The volume did not. If you were watching volume instead of price, there was a signal buried in the noise.

Mining Stocks Led by ~7 Days

Mining stocks started selling off in early May 2022 as on-chain data showed miner selling accelerating. Terra/Luna imploded in mid-May and dragged everything down. But equity markets had already priced in deteriorating miner economics. If you were paying attention, you had a week's head start.

No Advance Warning

Fraud event. Pure and simple. No amount of mining stock analysis was going to predict Sam Bankman-Fried's house of cards. Mining stocks and Bitcoin fell simultaneously. No lead, no lag. That is the critical limitation: mining stocks signal deteriorating fundamentals. They cannot signal that someone is committing fraud behind closed doors.

Mining Stocks Led Bitcoin Higher

JPMorgan's data showed 12 of 14 tracked miners outperforming Bitcoin in the first two weeks of the year, with a combined $4.5 billion in market cap gains. Riot Platforms surged 32%, Cathedra Bitcoin 25%, Bit Digital 24%. The signal works in the other direction too. When miners are leading up, institutional money is front-running optimism in the same way it front-runs fear. Bitcoin's 144% year-on-year growth provided the backdrop, but mining stocks priced in the continuation before spot confirmed it.

The pattern is clear enough to be useful, but limited enough to be dangerous if you treat it as gospel. Mining stocks have shown genuine predictive value for corrections driven by fundamental deterioration - rising costs, regulatory pressure, declining margins. For black-swan events like exchange fraud or stablecoin collapses? Useless. The signal is fundamentals-based, not event-based. That distinction matters more than most people realise.

The Consolidation Factor: 12 Companies, 30% of Hash Rate

Something fundamental has changed about the structure of Bitcoin mining since the last cycle, and it directly affects whether mining stocks work as a predictor. A Bernstein report from January 2025 found that just twelve publicly traded companies now control 30% of Bitcoin's total network hash rate. That is up from 22% in January 2024. A nearly 40% increase in concentration in a single year.

Marathon Digital leads the pack at 53 EH/s - roughly 7% of the entire network. One company. Seven percent of the computational power securing a $2 trillion asset. CleanSpark experienced a 400% year-over-year hash rate increase and now holds about 5%, having actually surpassed Riot Platforms in operational capacity. Iris Energy grew its hash rate by 450% in 2024 and simultaneously expanded its GPU infrastructure for AI workloads. Riot, while growing more slowly, has continued acquiring capacity through development projects and acquisitions.

The Perryman Group put broader numbers on this. US-based public miners now control approximately 29% of Bitcoin's global hash rate, a 50% increase from the previous year. The combined market capitalisation of 31 publicly traded Bitcoin mining firms stands at $44 billion, with 26 of those companies showing positive stock movement in early 2025.

For the predictor thesis, this consolidation cuts both ways. On one hand, fewer and larger stocks mean a cleaner signal. When Marathon's stock drops, it moves the aggregate meaningfully - there is less noise from micro-cap miners that trade on tiny volume. On the other hand, single-company events now carry outsized weight. If Marathon announces a facility outage or a convertible bond offering, its stock can drag the whole composite down in ways that have nothing to do with Bitcoin's trajectory.

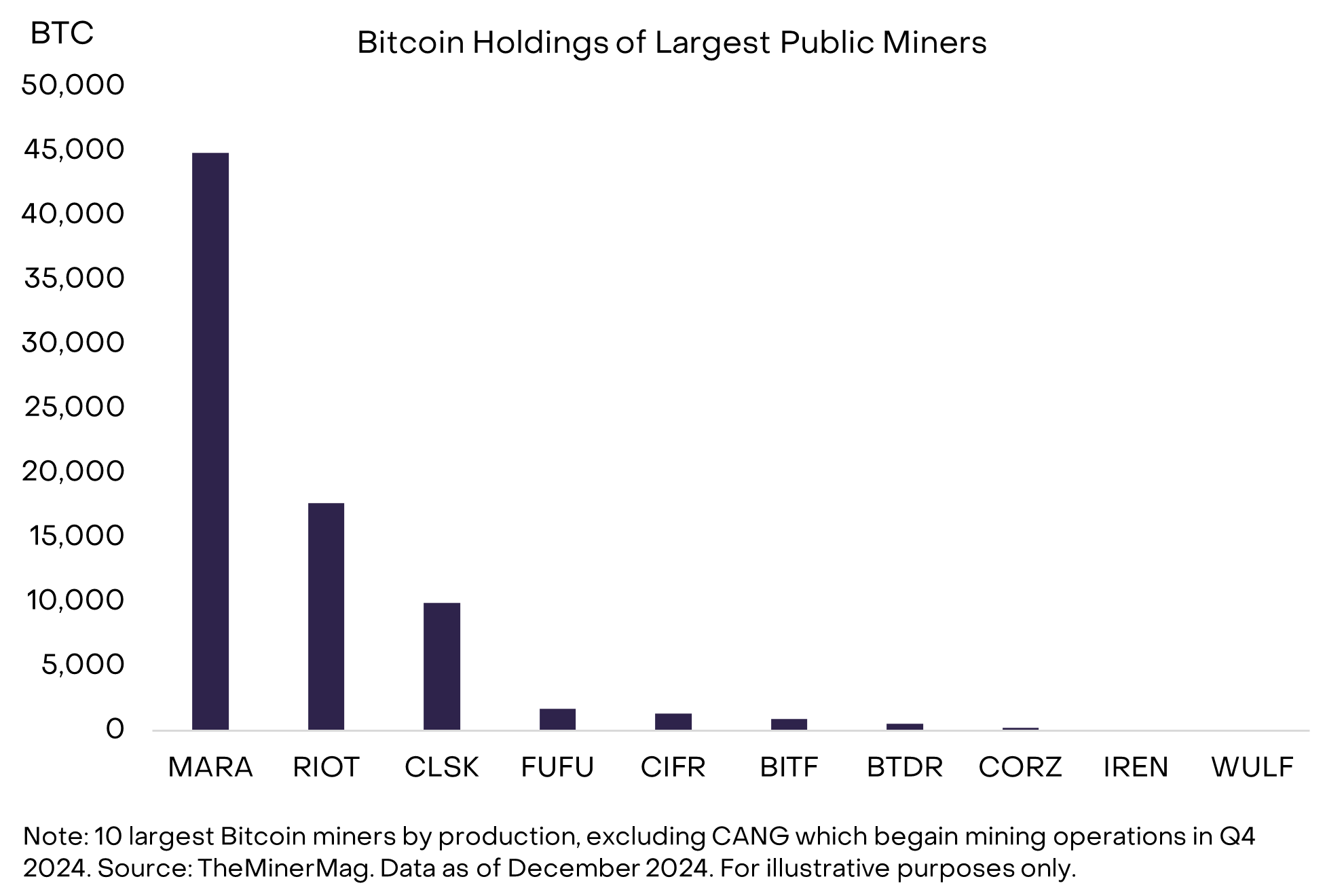

And then there is the balance sheet question. Marathon holds approximately 44,890 BTC on its books - valued at around $4.5 billion, representing roughly 70% of its overall market capitalisation. This is the MicroStrategy playbook applied to a mining operation: use Bitcoin as a balance sheet asset, raise capital through convertible bonds, and let the stock price become a leveraged bet on BTC appreciation. Bernstein flagged this as a growing trend among the large consolidators. But it changes what the stock price means. When 70% of your market cap is just Bitcoin sitting in a wallet, your stock isn't really tracking mining economics anymore. It is tracking treasury value. You need to account for that when reading the signal.

Meanwhile, publicly listed miners collectively held a record 92,473 BTC as of December 2024, according to TheMinerMag. That is significant. When miners are accumulating rather than selling, it is a bullish data point in its own right - they are betting on higher prices with their own production. When that trend reverses, and miners start liquidating aggressively? That is one of the earliest warning signals in the toolkit.

The KPIs That Matter: What to Actually Watch

If mining stocks can work as a forward indicator, what exactly should you track? Not all mining companies are built the same, and the wrong KPIs will send you chasing ghosts. What I have found most useful is combining stock-level data with operational metrics - the stuff that actually reflects whether these businesses are healthy or quietly bleeding out.

Stock Price vs. BTC Correlation

Track the rolling 30-day correlation between each miner's stock and Bitcoin. When it breaks down - the stock drops while BTC holds - something is off. The typical range sits between 0.6 and 0.85. Anything below 0.5 for more than a few days demands investigation.

Relative Trading Volume

Volume spikes in mining stocks without corresponding BTC volume often precede directional moves. Watch for 2x+ average volume days that diverge from Bitcoin's trading activity. The November 2021 cycle top was flagged by volume before price.

Hash Rate & Difficulty

Network hash rate hit 793 EH/s in January 2025 - a 51% yearly increase. Declining hash contributions from public miners suggest machines going offline due to unprofitable economics. JPMorgan noted miners earned roughly $54,900 in daily block reward revenue per EH/s in early January, down just 2% from December.

Miner BTC Holdings

Public miners held a record 92,473 BTC as of December 2024. Accelerating sales - especially into strength - indicate miners raising cash or hedging against expected declines. Marathon alone holds 44,890 BTC. When the big holders start selling, pay attention.

Production Cost per BTC

During Q3 2024, production costs across major miners ranged from $34,000 to $59,000 per BTC against an average price of $61,000. That spread is what equity analysts model. When the cheapest miners start losing money, the entire sector is in trouble.

Debt-to-Equity & Liquidity

Highly leveraged miners amplify both directions. Marathon and Riot have raised capital through convertible bonds - the MicroStrategy playbook. Deteriorating balance sheets increase the probability of forced selling and stock breakdowns that precede broader market weakness.

The Mining Stock Watchlist

A reliable signal requires monitoring the largest and most liquid publicly traded miners. These companies collectively represent close to 30% of Bitcoin's total hash rate, and their stocks are the most widely followed by institutional investors. Here is the updated watchlist with data from Bernstein's January 2025 research:

| Company | Ticker | Hash Rate (EH/s) | Signal Profile |

|---|---|---|---|

| Marathon Digital | MARA | 53 EH/s | 7% of network. Holds 44,890 BTC ($4.5B) - stock partially tracks treasury value, not just mining. MicroStrategy-style approach complicates the signal. Weight accordingly. |

| CleanSpark | CLSK | ~37 EH/s | 400% YoY hash growth. Aggressive acquisitions, low-cost energy focus. Now 5% of network. Purest mining signal of the large caps - limited AI diversification. |

| Core Scientific | CORZ | ~20 EH/s | Post-bankruptcy. 12-year CoreWeave AI hosting contract worth billions. Heavy AI/HPC revenue dilutes mining signal. Down-weight in BTC predictor model. |

| Riot Platforms | RIOT | ~22 EH/s | Corsicana TX mega-facility. Led the January 2025 rally with a 32% gain. Energy trading capabilities provide non-BTC revenue. Still primarily a mining play. |

| Iris Energy | IREN | ~15 EH/s | 450% hash growth in 2024 plus NVIDIA GPU expansion for AI. 90% realization rate in December. Dual identity: miner and AI infrastructure. Watch both sides. |

| Hut 8 Corp | HUT | ~8 EH/s | Canadian ops, large BTC reserve. Integrating AI into operations with NVIDIA GPUs. Smaller but with distinct geographic and strategic profile. |

The 2024 Halving: How It Reshaped the Signal

The April 2024 halving cut the block reward from 6.25 BTC to 3.125 BTC, instantly slashing mining revenue per block. Pre-halving, the market spent months pricing in the squeeze - mining stocks underperformed Bitcoin through Q1 2024 as investors front-ran the profitability hit. Since then, three things have reshaped the relationship between mining stocks and Bitcoin.

The survivors are bigger and better capitalised. The post-halving shakeout culled weaker operators, and what is left is a concentrated group of larger, more efficient companies. These firms can absorb moderate Bitcoin dips without triggering the operational distress signals that used to ripple through mining equities after every 10% pullback. The sensitivity threshold has shifted upward. Small corrections barely register in mining stock prices anymore.

But here is the flip side: because the halving raised the industry's average break-even cost, when corrections do cross that higher threshold, the stock price declines are sharper and faster than anything we saw pre-halving. Grayscale's data showed that miner revenue per MWh dipped significantly around the halving event before recovering - the V-shape was brutal for operators running at $55,000+ production costs while Bitcoin briefly traded in the low $60s. That kind of margin compression (about $6,000 per coin for the least efficient producers) doesn't show up gradually. It hits earnings estimates all at once, and the stock price reacts before the quarterly numbers come out.

Bitcoin is up 61% since the halving, 51% since the US presidential election in November, and 144% year-on-year. Those returns have bailed out even the least efficient miners - for now. But the structural vulnerability remains. The next time Bitcoin's price drops toward the $55,000 to $60,000 range where the upper end of production costs sits, mining stock behavior will be an early warning system unlike anything available in the spot market.

Post-Halving Signal Adjustments

- Higher break-even costs ($34k-$59k range) mean mining stocks now react more violently to downside - corrections that were absorbed pre-halving now trigger genuine distress signals

- AI/HPC diversification adds noise - Core Scientific's 12-year CoreWeave contract means its stock price increasingly reflects data centre demand, not Bitcoin

- Industry consolidation means 12 companies control 30% of hash rate - single-company events (capex delays, facility outages) can create false signals in a way they couldn't when hash rate was distributed across hundreds of smaller operators

- BTC treasury strategies have evolved - Marathon's 44,890 BTC holding means 70% of its market cap tracks Bitcoin's price directly, not mining economics

The AI Pivot: Signal or Noise?

This is probably the most important development for anyone using mining stocks as a Bitcoin predictor. A growing number of miners are pivoting substantial infrastructure toward artificial intelligence and high-performance computing. And it raises a question that didn't exist two years ago: if mining companies derive 30, 40, 50% of revenue from AI hosting, does their stock price still tell you anything useful about Bitcoin's direction?

The pivot makes strategic sense. The 2024 halving cut block rewards in half, amplifying the impact of Bitcoin's price volatility on profitability. Miners already owned the two things AI needs most: access to cheap power and large-scale data centre facilities. Core Scientific's hosting agreement with CoreWeave, an AI-focused infrastructure provider, illustrates the scale of the opportunity. It is a 12-year contract projected to generate billions in revenue - the kind of financial predictability that Bitcoin mining, by its nature, can never provide.

But here is what I find fascinating about the AI pivot specifically, rather than diversifying into mining other cryptocurrencies. Bitcoin mining hardware - ASICs - is designed exclusively for the SHA-256 hashing algorithm. You can not repurpose an ASIC to mine Ethereum (which moved to proof-of-stake anyway) or most other altcoins. Even the ones that still use proof-of-work often employ different algorithms that require entirely different hardware. So miners face an unusual constraint: their machines are useless for anything except Bitcoin, but their buildings, their power contracts, and their cooling infrastructure are perfectly suited for general-purpose GPU workloads. The AI pivot isn't a choice between Bitcoin and other crypto. It is a choice between Bitcoin and an entirely different industry.

Iris Energy deployed NVIDIA GPUs for AI modelling and cloud services while simultaneously growing its mining hash rate by 450%. Hut 8 is integrating AI into its Canadian operations. And the concept of miners as "load balancers" for energy grids has emerged - scaling down Bitcoin mining during peak AI operations or periods of high energy demand, then ramping mining back up when energy is abundant. This dynamic could actually strengthen both businesses rather than cannibalise one for the other.

The network security question is worth taking seriously though. If significant hash power permanently diverts to AI, the Bitcoin network's total hash rate could decline, theoretically making the blockchain more susceptible to attacks. Grayscale estimates that a one-hour 51% attack would cost between $5 billion and $20 billion - and the difficulty adjustment algorithm ensures blocks keep getting mined at regular intervals regardless of how many miners participate. But the risk isn't zero. If the economics of AI hosting consistently beat the economics of Bitcoin mining, rational operators will allocate accordingly. The remaining miners benefit from reduced competition in the short term, but the network's long-term security model assumes miners stay.

For the predictor thesis, the AI pivot means one practical thing: you need to know which miners are still predominantly Bitcoin operations and which have become hybrid data centre operators. Core Scientific's stock might drop because of concerns about AI infrastructure competition, not because of anything happening with Bitcoin. Iris Energy might surge on a new NVIDIA partnership while Bitcoin trades sideways. The signal purity degrades in direct proportion to AI revenue share. I would down-weight or exclude any miner deriving more than 30% of revenue from non-Bitcoin sources when constructing a predictive composite.

The Real-World Friction: Lawsuits, Tariffs, and Grid Politics

The mining industry generated $4.14 billion in US gross product during 2024 and created over 31,000 jobs, according to a Perryman Group study commissioned by the Texas Blockchain Council. That sounds clean and impressive in a press release. The reality on the ground is considerably messier.

Texas dominates American mining, accounting for 40% of national revenue and 12,219 jobs. Georgia surprised everyone by emerging as the number two state with 2,300 jobs and $316 million in revenue - ahead of traditional centres like New York and North Dakota. But the industry's growth has created friction that directly affects mining stock prices in ways that have nothing to do with Bitcoin's trajectory.

Multiple lawsuits have been filed against mining operations across the country, primarily over noise pollution. Marathon Digital faces legal action in Texas where residents claim the company's mining rigs create "intolerably loud noise conditions" that have led to health issues. Similar suits target Greenridge, GMO Internet, and Red Dog. Each lawsuit is a potential headline that moves the stock price independently of Bitcoin. If Marathon drops 8% on a noise pollution ruling while Bitcoin holds steady, that is not a crash signal. That is litigation risk. But it will show up in any naive composite index as a divergence.

Then there is the grid situation. The Electric Reliability Council of Texas (ERCOT) has paid miners millions to shut down their equipment during peak demand periods. Some miners earned over $10 million monthly through these curtailment arrangements - essentially getting paid to not mine. The practice drew enough criticism that a bill in the Texas Senate aims to end these agreements entirely. If it passes, miners lose a significant alternative revenue stream, their stocks adjust, and again - none of that has anything to do with where Bitcoin is heading.

Trade policy is the newest complication. Trump's return to office was expected to boost mining in certain ways, but his administration's trade policies have created unexpected problems. Mining companies are experiencing delays in receiving ASIC shipments from Chinese manufacturers like Bitmain, with increased scrutiny at US borders slowing deliveries. For a miner that just ordered $50 million worth of next-generation machines, a three-month customs delay means three months of running older, less efficient equipment at tighter margins. The stock reacts to that. Bitcoin doesn't notice.

These non-Bitcoin factors are what create false positives in any mining-stock-based prediction model. Lawsuits, tariff delays, grid politics, equipment delays, individual company governance issues - they all move stock prices without reflecting anything about the cryptocurrency's fundamental demand or supply dynamics. This is why a single mining stock can never be a predictor, and why even a composite index needs constant maintenance to filter out the noise.

Putting the Framework Together

Given everything above, using mining stocks as a market indicator requires something more nuanced than watching a few tickers. Start by building an equal-weighted composite of four to six major mining stocks - MARA, RIOT, CLSK, CORZ, IREN, HUT - and track the composite's daily performance against Bitcoin's spot price. The composite approach is critical because it reduces single-company noise. Marathon's lawsuit doesn't matter if the other five stocks are holding up fine.

The most actionable signal is a multi-day divergence: the composite declines for three or more consecutive days while Bitcoin stays flat or rises. Historically, this pattern has preceded corrections in roughly 60-70% of cases when the composite decline exceeds 10%. Divergences under 5% or lasting fewer than two days carry a much higher false-positive rate and should be treated as noise. I would not act on anything shorter than a three-day window with less than a 7% decline.

Cross-reference with on-chain data. If the mining composite is weakening and on-chain metrics show accelerating miner outflows to exchanges (trackable via Glassnode or CryptoQuant), the signal strengthens considerably. Both data sources pointing the same direction is the confirmation that moves the probability from "possibly interesting" to "probably actionable."

Filter the AI noise. This is non-negotiable now that multiple major miners derive significant revenue from non-Bitcoin sources. Down-weight Core Scientific and any miner where AI/HPC hosting exceeds 30% of revenue. Their stock prices increasingly reflect data centre market dynamics, not Bitcoin fundamentals. CleanSpark, by contrast, remains one of the purest mining signals among the large caps - limited diversification, aggressive hash rate growth, and stock movements that track mining economics closely.

Account for treasury effects. Marathon's stock is 70% Bitcoin treasury by value. If BTC drops 5%, Marathon's stock should drop roughly 3.5% from treasury impact alone, before you even consider the mining profitability effect. That is not a predictive signal. It is math. Separate the treasury beta from the operational signal to avoid counting the same information twice.

And set realistic expectations. Even well-constructed, this framework will produce false positives 30 to 40% of the time. Never treat a mining stock divergence as a definitive sell signal. Use it as a trigger to tighten risk management: reduce position sizes, set tighter stop-losses, or rotate from high-beta crypto assets into Bitcoin or stablecoins. The framework identifies elevated risk, not certainty.

What to Watch in 2025

The early data is encouraging. JPMorgan's analysts noted that miners earned approximately $54,900 in daily block reward revenue per EH/s in early January - only a 2% drop from December. Hash price has been nearly stable. And mining stocks are outperforming Bitcoin, which historically correlates with bullish continuation. But several factors will determine whether mining stocks remain useful as indicators this year.

The post-halving adjustment period typically runs 12 to 18 months, so the industry is still finding its new equilibrium. Energy cost dynamics matter enormously - any sustained increase in US electricity prices will compress margins and show up in mining equities before it hits Bitcoin's hash rate. Spot Bitcoin ETFs have changed the demand side of the equation, and ETF inflows may now be a more important short-term price driver than supply-side mining economics, which could reduce the predictive power of the mining stock signal.

Bernstein's most striking finding is the valuation gap. Mining companies currently trade at a 90% discount compared to traditional data centre operators. If the market begins to re-rate miners as hybrid Bitcoin/AI infrastructure companies rather than pure cryptocurrency plays, these stocks could re-price dramatically - and that re-rating would create sustained divergence from Bitcoin's price that has nothing to do with predicting a crash. It would be a structural re-evaluation of what these companies are worth. Watch for it. Because when it happens, the predictor model will need a complete overhaul.

Key Takeaways

- Mining stocks have historically led Bitcoin corrections by 5-15 days in cases driven by fundamental deterioration, but provided no advance warning for black-swan events like exchange fraud

- Bitcoin mining generated $15 billion in revenue in 2024 (34% CAGR since 2014), with production costs ranging from $34,000 to $59,000 per BTC across major miners - these cost thresholds are the trigger points that equity analysts watch

- Industry consolidation has accelerated: 12 companies now control 30% of hash rate (up from 22% in January 2024), creating a cleaner but also more company-specific signal

- The AI/HPC pivot is the biggest noise factor - Core Scientific's 12-year CoreWeave contract, Iris Energy's GPU expansion, and Hut 8's AI integration all dilute the mining stock signal. Down-weight miners with more than 30% non-Bitcoin revenue

- Real-world friction (lawsuits, ERCOT grid politics, tariff-delayed ASIC shipments) creates false positives that have nothing to do with Bitcoin's direction - a composite index approach is essential for filtering company-specific noise

- Marathon's treasury strategy (44,890 BTC, 70% of market cap) means its stock is partially a Bitcoin holding vehicle - separate treasury beta from operational signal to avoid double-counting

- JPMorgan's early 2025 data showed 12 of 14 mining stocks outperforming BTC, with a $4.5 billion aggregate market cap gain - the signal works in both directions, for bullish confirmation as well as bearish warning

- Bernstein's 90% discount finding (miners vs. traditional data centres) suggests potential structural re-rating that would fundamentally change the predictor model

- False positive rate remains 30-40% - this is a risk management tool, not a standalone prediction system

Bellwether Research, Research Team, February 21, 2025