Robotics might be the most over-narrated, under-analysed theme in markets right now. Every conference deck has a humanoid on the cover. Every fund launch has the word "physical AI" in the prospectus. And almost none of it tells you the one thing an investor actually needs to know, which is where, inside this enormous and genuinely real build-out, the money ends up.

Here is my answer up front, because you deserve a stance before you deserve my reasoning. Robots themselves, the gleaming humanoids that get the magazine covers, are where capital is loudest and unit economics are worst. China has already commoditised that hardware, building humanoids at roughly half the Western cost and shipping close to nine in ten of the world's units last year. Durable money for a Western investor sits one layer above the robot and one layer below it: in the enabling stack that every robot has to buy, and in the proven service niches that already bill real revenue. Own the toll booths and the cash registers. Be very careful with the lottery tickets.

That is a contrarian read against a market that wants to pay up for the robot itself, so I am going to earn it. This study does four things. It maps physical AI as a stack, so you can see which layers are defensible. It walks the forecast fog, where credible houses disagree by more than an order of magnitude. It confronts the China question honestly, because it reframes the whole opportunity for Western capital. And it sorts the investable names into three buckets with three completely different payoff shapes.

Before the argument, here is the terrain it covers: what the bet is worth, who is actually shipping, and where the value quietly leaks.

Inflection Point

Something changed in the last eighteen months, and it is worth naming precisely, because the precision is where the analysis lives. Robots stopped being a demo and started being a line item. Not a science-fair humanoid waving on a stage. A unit on a purchase order, with a delivery date and a warranty.

Look at what crossed the wire just in the run-up to this study. Nvidia introduced Halos for Robotics, which it calls the industry's first full-stack safety system for physical AI, and Agility Robotics became the first to build it into Digit, the humanoid already working logistics for Amazon, GXO, Schaeffler, and Toyota. Zebra Technologies, having folded Photoneo's vision-guided bin-picking into its machine-vision line, reckons 98% of the manufacturers it surveys will be using machine vision by 2029. AgiBot rolled its ten-thousandth humanoid off a line in March. France placed an order for five thousand military drones with a two-year-old startup. None of those is a concept video. Each is a transaction.

Deepu Talla, who runs robotics and edge AI at Nvidia, framed the shift in a single sentence that an investor should sit with.

"With NVIDIA Halos for Robotics, developers and system builders can harness NVIDIA's proven autonomous-vehicle safety foundation to develop safer robots faster and bring them into industrial operations alongside workers with greater confidence."- Deepu Talla, Vice President of Robotics and Edge AI, Nvidia

Read that as a supplier would, not as a press release. Safety certification is the gate between a robot that demos and a robot that gets insured, deployed, and paid for. When the dominant compute vendor productises that gate and routes it through an accredited inspection lab, it is removing the single biggest non-technical barrier to deployment at scale. That is what an inflection looks like up close. Boring, procedural, and far more bullish than another backflip video.

Money is following the procedure. Masayoshi Son told CNBC this is where he sees the next trillion-dollar company emerging. Dan Ives at Wedbush calls humanoids "the golden goose for physical AI." Jason Pidcock, who runs Jupiter's Asian Income fund, put it plainly at a London briefing in May: in ten years "there will be humanoid robots all over the place. You may have one in your home. Factories will be full of them." Conviction is not the scarce input anymore. Discernment is. Which brings us to the first hard question, because the people selling you the theme cannot even agree on how big it is.

Market Forecasts

Six credible research houses publish six different sizes for "the robotics market," and the spread between them is not a rounding error. It is more than an order of magnitude at the back end of the decade. That dispersion is not a flaw in the data. It is the single most useful piece of information in this entire study, and almost nobody treats it that way.

| Source | Base | Terminal | CAGR | What It Actually Measures |

|---|---|---|---|---|

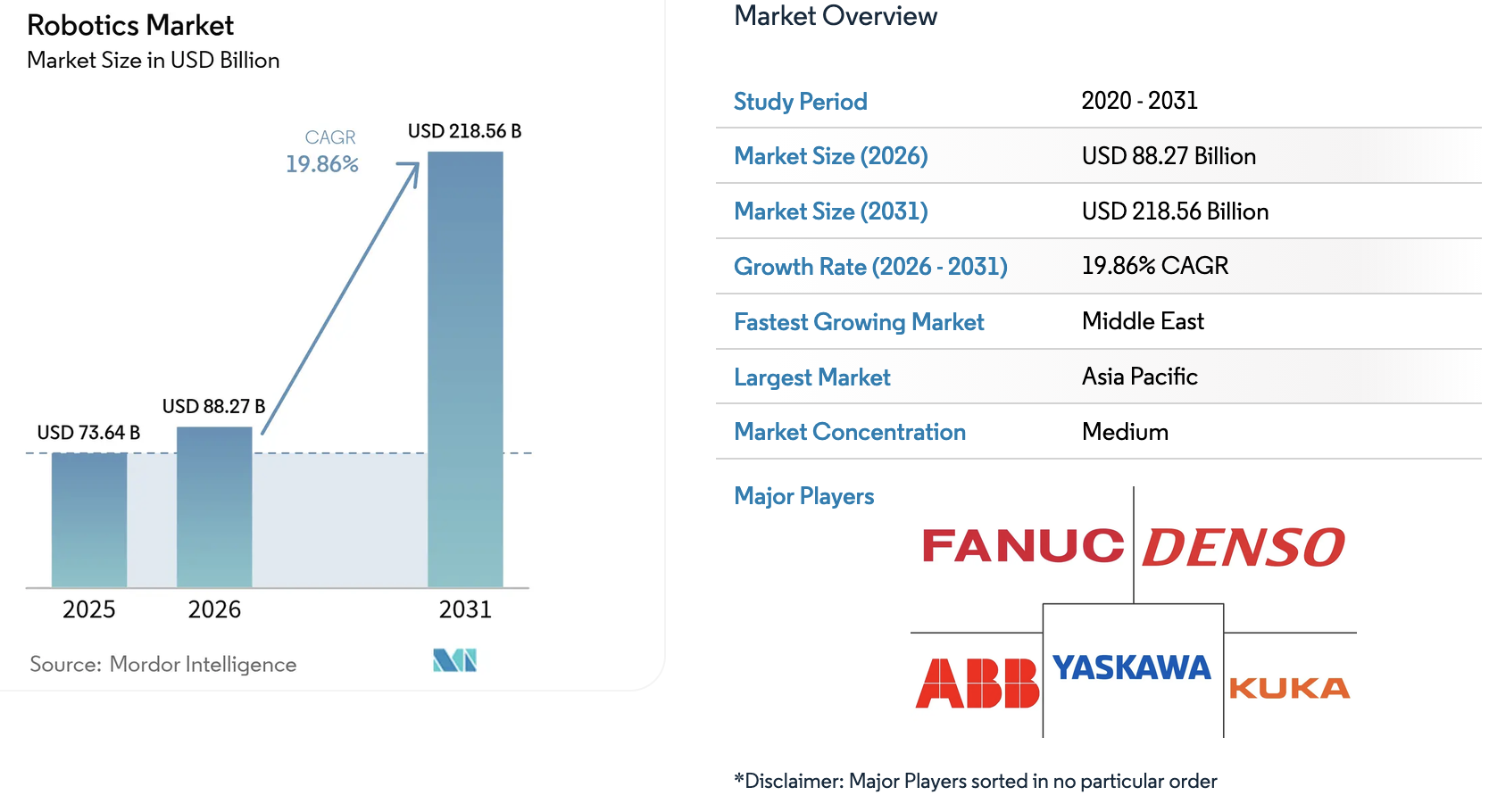

| Mordor Intelligence | $88.27B (2026) | $218.56B (2031) | 19.86% | All robotics; industrial robots are 71% of it |

| Global Growth Insights | $90.07B (2026) | $905.45B (2035) | 29.23% | All robotics, aggressive humanoid ramp baked in |

| Global X (issuer) | $108B (2025) | $416B (2035) | ~14% | Robotics & automation universe (ETF framing) |

| Syndicated industry report | $31.42B (2025) | $89.21B (2035) | 11.00% | Narrow hardware base, service-robotics weighted |

| Coherent Market Insights | $6.25B (2026) | $35B (2033) | 33.00% | "AI robots" only, the intelligent slice |

| Barclays | $2-3B (today) | $200B (2035) | steep | Humanoids specifically, optimistic adoption |

Stare at that table and a discipline reveals itself. Every one of these numbers is defensible, because each measures a different object. A $35 billion "AI robots" forecast and a $905 billion "all robotics" forecast are not in conflict, they are answering different questions. So when a pitch deck quotes you a robotics TAM, your first question is never "is that right." It is "which slice and does the company I am looking at actually sell into it." Slice-level growth matters infinitely more than universe-level growth, and conflating the two is how investors overpay.

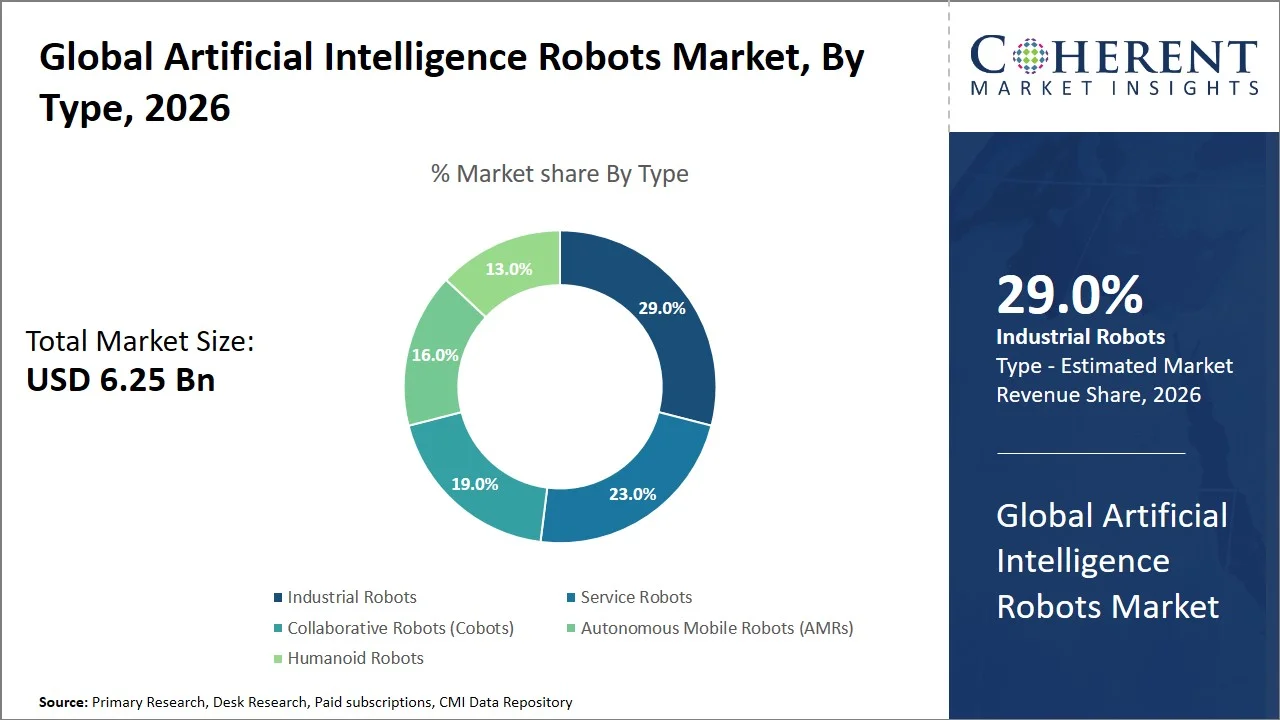

Underneath the headline number mix tells you where today's dollars genuinely are, and it is not where the headlines point. By Mordor's cut, industrial robots still command 71% of revenue and logistics-and-warehousing is the single largest application at 39%. Humanoids, the entire reason this theme is fashionable, are a rounding error in current revenue. Coherent Market Insights, which measures the narrower "AI robots" slice, makes the same point from a different angle.

Hold that thought, because it sets up the central tension of this study. Demand and revenue today live in industrial and logistics automation, a mature, cyclical, mid-teens-to-twenties grower. Imagination and valuation live in humanoids, a tiny, pre-profit slice with a venture-scale risk profile. Both are real. They do not deserve the same multiple and they certainly do not deserve the same conviction. To see why, you have to understand how a robot is actually built.

Physical AI Stack

A robot is not one product. It is a stack, and the layers have wildly different economics, exactly the way they did in personal computers, smartphones and cloud. Get the layers straight and investment map draws itself. Skip this and you will keep mistaking the most visible layer for the most valuable one.

Start with conceptual shift engineers are living through, because it tells you which layer is hardening into a moat. Industry writers now talk about "physical AI 1.0" giving way to "physical AI 2.0." Version 1.0 was vision-first: pile on cameras and compute, train on massive video and simulation, and assume the model can predict the world. Version 2.0 adds the layer that actually breaks systems in the field, physical state recovery, the job of reconstructing what is really happening from noisy, occluded, contradictory sensor data before any reasoning happens at all. One line from that literature is the whole thesis in miniature: "in the real world, what you don't see matters more than what you do."

Why does that matter to an allocator? Because it tells you the unit of competition is no longer the model. A humanoid has to fuse sensing, world models, state recovery, reasoning, safety, and bounded actuation into one loop that works at the edge, in real time, without hurting anyone. That integration is brutally hard, and it pushes value toward whoever supplies the hardest, scarcest pieces of the loop. Map the stack by how defensible each layer is and the picture is stark.

Compute and safety. This is Nvidia's layer and it is the most defensible in the entire industry. Jetson Thor for edge compute, Isaac GR00T as a foundation model for humanoids, Cosmos and Omniverse for simulation, Halos for certified safety. Its March 2026 deal to fold Omniverse into ABB's RobotStudio claims to close the sim-to-real gap with up to 99% accuracy, and FANUC, Foxconn, Boston Dynamics with Google DeepMind, and Kawasaki's new San Jose physical-AI centre are all building on the same substrate. When every robot maker, Western and Chinese, trains and validates on your platform, you are selling shovels to every miner in the field.

Memory and sensing. One layer down, and almost nobody is pricing it as robotics yet. A humanoid running vision, planning and motor control simultaneously is a memory hog, and it needs that memory to be dense, fast and miserly with power. Micron sits exactly here, with LPDDR5X moving data near 9,600 MT/s and LPCAMM2 modules that the company says free up to 60% of motherboard space. Robotics will not move Micron's needle this year, the analyst who covers it is explicit that the supercycle is a 2030s story, but the point holds: every robot is a memory customer and the memory leader for automotive-grade reliability is already in the building.

Actuators and components. Here is where the bull case for Western robot makers springs a leak. Actuators, the motors and joints that give a robot strength and dexterity, are close to half the bill of materials of a humanoid, and roughly 90% of key robotics components are sourced from China. That is not a detail. It is the ballgame, and it is why a materials breakthrough matters. In 2026, MIT published electrofluidic fiber muscles in Science Robotics, an actuator that pumps fluid with electric fields, weighs almost nothing, runs silent, and hits 50 watts per kilogram, matching skeletal muscle, with a single bundle lifting 4 kilograms, two hundred times its own weight. Every serious humanoid program, Figure, 1X, Boston Dynamics, Tesla Optimus, is bottlenecked on actuation that is too rigid, too loud, or too heavy. Whoever industrialises the next actuator captures margin that today leaks to Chinese suppliers. That is the prize, and it is a components prize, not a robot-brand prize.

Robot itself. Bottom of the moat chart for a reason. Assembling a humanoid out of largely commoditised parts, in a world where China builds them at half your cost, is the thinnest-margin job in the stack unless you own the layers above it. That is precisely why the credible Western players, Tesla and Figure, are vertically integrating, building their own actuators, sensors, and batteries in-house. Apptronik, which raised $520 million in February backed by Google and Mercedes-Benz, is doing the same. They are not trying to be robot assemblers. They are trying to own the defensible layers so the robot is not a commodity. Whether they pull it off is the trillion-dollar question, and it is the subject of Chapter V.

China Volume Lead

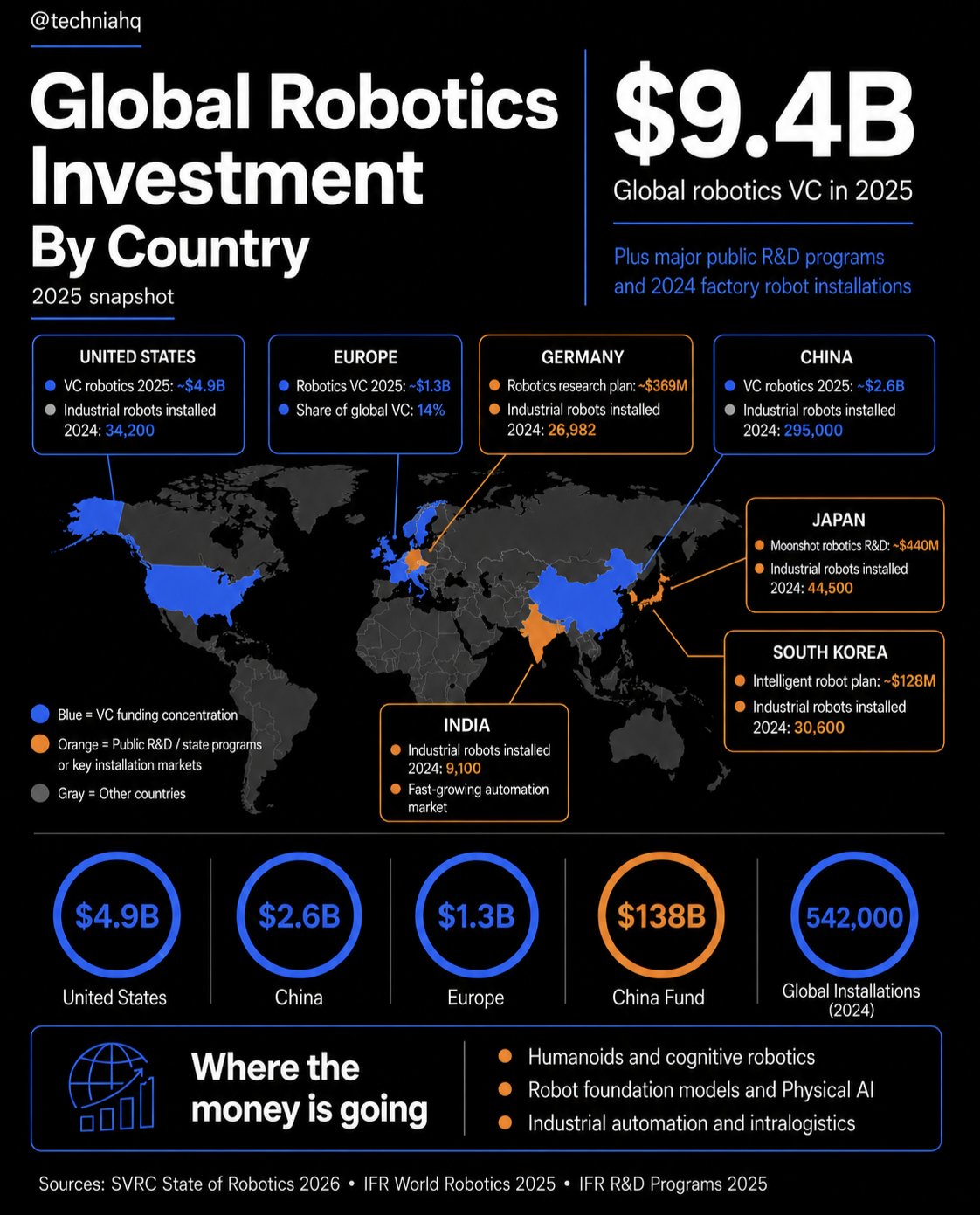

Any honest robotics study has to plant a flag on China, because the numbers are not close and they reframe the entire opportunity for Western capital. So let me plant it. On volume, manufacturing depth and cost, China has already won, and pretending otherwise is the fastest way to misprice this sector.

Weigh the evidence. China installed roughly 295,000 industrial robots in 2024, about nine times the United States' 34,200, and now operates more than two million units, the largest stock on earth. It produces an estimated 70-80% of the world's commercial drones and held 79% of approved drone patents in 2024. On humanoids, Chinese vendors shipped close to 90% of the roughly 13,000 units sold globally in 2025, a market that quintupled in a year, led by AgiBot near 5,200 units and Unitree above 5,500. And it builds them cheap, Barclays pegs Chinese humanoids near the $50,000 range, roughly half the cost of Western competitors. Robot density makes the structural point: China has lifted to about 470 units per 10,000 workers, while the United States ranks ninth globally at 285, behind South Korea's 1,012 and Japan's 397.

Now the part pessimists miss, because it is where investable Western thesis actually lives. America is arguably the design leader even as it trails on volume. All three non-Chinese names on Omdia's top-selling humanoid chart for 2025 were American: Figure AI, Agility Robotics, and Tesla. TrendForce frames it cleanly, US edge is a more advanced AI ecosystem, China's is supply-chain density and cost, and Japan's is component precision. So the question for a Western investor is not "can America out-ship China." It cannot, not this decade. What matters now is whether American companies can capture durable value in the layers where they actually lead, software, compute, design, and certified safety, while the commodity assembly happens elsewhere.

Policy is now bending hard in that direction, and defence is the sharp end. Washington's Drone Dominance program targets roughly $1 billion in orders across about 340,000 drones, Pentagon drone spending is projected at $9.4 billion in fiscal 2026 inside a $13.4 billion autonomous-systems budget, and in December 2025 the FCC added DJI, Autel and effectively all foreign-made drone hardware to its Covered List, blocking new authorisations. Europe is moving too: France's five-thousand-drone order with Dassault-backed Harmattan AI is exactly the reshoring reflex Ukraine taught the continent. None of this closes the manufacturing gap quickly, that takes a decade, but it changes the demand curve and the capital available to climb it. For investors, the cleaner read is to own the layers where the West leads rather than to bet it wins a volume war it is structurally losing.

Humanoid Economics

Now the glamour trade...and I am going to give the bulls their best shot before I push back, because a thesis you cannot steel-man is a thesis you do not really hold.

Here is the bull case, made as well as I can make it. Humanoids are "automation 3.0," built to fill structural labour gaps that ageing, urbanising societies cannot fill with people. Barclays' Zornitza Todorova, co-author of the bank's "AI Gets Physical" report, told CNBC the market goes from $2-3 billion today to $200 billion by 2035, in two waves, manufacturing and logistics first through 2030, then services, healthcare, and eldercare after. If physical AI follows the smartphone arc, value accrues to whoever ships the integrated device at scale, way Apple captured the phone and not its glass supplier. China's cost lead is then the very reason a vertically integrated Western maker that owns its own actuators could earn the entire margin stack as component costs fall an estimated 50-70% after 2029. On that logic, buying picks-and-shovels instead of the robot is like buying Gorilla Glass instead of Apple.

"Humanoid robotics is really on an upward trajectory... we see it going up to $200 billion in 2035. We're just scratching the surface of what humanoid robots can do."- Zornitza Todorova, Head of Thematic FICC Research, Barclays, on CNBC's "Squawk Box Europe"

I take that case seriously. Now here is why I will not pay up for it yet, and it comes down to economics that are visible today rather than narratives about 2035.

Consider Ubtech Robotics, the cleanest listed humanoid pure-play and, to its credit, a genuinely improving business. Its 2025 net loss narrowed to about CNY 703 million, better than the roughly CNY 1.02 billion the street feared, gross margin jumped 900 basis points to 38%, and humanoids grew to 44% of revenue. Management guides to 10,000 deliveries in 2026 against just 1,079 actually sold in 2025, and to break-even in 2027 at 30,000-50,000 cumulative units. Bulls at one shop model the path and arrive at a $20 target, roughly 48% above the recent quote.

That is the most disciplined version of the long case, and look at what it requires. Profit is entirely a 2027-2028 event, contingent on a near tenfold delivery ramp, in a segment where Unitree and AgiBot are aggressively cutting price. Now widen the lens to the celebrated Western names, where the gap between ambition and reality is starker still. Figure AI raised over $1 billion at a $39 billion post-money valuation and is building toward 100,000 units over four years, impressive...but entirely a promise. Tesla discontinued Model S and Model X to convert Fremont lines to Optimus, targeting a million units a year, yet Musk admitted in January 2026 that zero Optimus robots were doing useful work in Tesla's own factories and the Gen-3 reveal slipped again to mid-summer. Serious capital, serious engineering, a future that has not arrived.

My read, and I will own it. Humanoids are the correct long-term theme but wrong place to concentrate capital in 2026. Payoffs are binary and terminal, leaders are pre-revenue or loss-making and the most likely volume winner may well be Chinese, private, or both, which means the public Western investor often cannot even buy the actual winner. That is a recipe for owning the theme through diversified exposure and enabling layers, not through a concentrated bet on a single robot maker's execution.

Proven Revenue Niches

While humanoid camp argues about 2035, an entire wing of robotics is already billing customers today, with real margins and proven adoption curves. This is the unglamorous half of the sector, and it is where I would rather have capital working while the humanoid question resolves itself.

Surgical robotics is the sharpest example. Intuitive Surgical built a software-margin business out of hardware by making razor-and-blade model work in an operating room. Whole category is compounding, Mordor sees surgical systems running from $4.18 billion in 2025 to $8.11 billion by 2031. Underneath the incumbent, a genuine disruptor is scaling. SS Innovations sells its SSi Mantra system for roughly $700,000 against the $2-2.5 million sticker on a da Vinci, about 65% cheaper, and the adoption curve shows it is landing.

SS Innovations' Q1 revenue more than doubled to $11.1 million with gross margin near 48%, and its cumulative installed base has climbed steadily toward roughly 194 systems. Treat it as the speculative end of the proven-niche bucket: real product, real revenue, real moat-in-the-making, with the entire upside hinged on FDA and CE clearances expected this year. Miss those and it is a developing-market growth story; hit them and the multiple re-rates. That is a defined, analysable bet, which is more than humanoid pure-plays can offer.

Machine vision is the second cash register and it is the actual brain of most working robots. Zebra Technologies, through its Photoneo acquisition, now sells vision-guided bin-picking and depalletizing, the dull, high-value tasks that warehouses pay for now. Zebra's own study found 92% of manufacturing leaders call digital transformation a priority and 98% plan to deploy machine vision by 2029. Vision is the sensor layer of physical AI, Zebra sells it with a revenue statement attached.

Then there is the cyclical backbone, the industrial automation that has carried robotics through every prior cycle. Juliana Faircloth of TD Asset Management captured the current setup on MoneyTalk, describing a "depleted industrial economy" where automation orders are turning up from a low base. ABB's automation orders have climbed from mid-single digits to near 10%, Sandvik posted 23% organic order growth, and the whole complex is lifting on labour scarcity rather than a boom. Her caution is the useful part for our purposes:

"These stocks are also starting to get wrapped up in a new thematic of what might physical AI look like one day, which is far down the road, but people get excited well ahead of these things becoming reality."- Juliana Faircloth, VP & Director, Portfolio Research, TD Asset Management, on MoneyTalk

That is the right frame for the whole proven-niche bucket. Surgical, vision, logistics AMRs, and cobots are real businesses with real cash flows that happen to carry a free physical-AI call option. Amazon's Vulcan picking robots, ABB's cobot launches, surge of Chinese cobot makers from 35% to 73% domestic share, these are revenue events, not promises. You are paid to wait, and the optionality is a bonus rather than whole thesis.

Supplier Mirage

A warning, because this is the trap that catches thoughtful investors who did the work but stopped one question short. "Robotics exposure" on an investor slide is not the same as robotics economics in the financials and the gap between the two is where money goes to die.

Aptiv is the instructive case, and I say that with respect, since serious analysts rate it a buy. Its robotics pitch is genuinely attractive on paper, partnerships with Comau, Robust AI, and Vecna. Management guiding that supplying autonomous mobile robots and humanoids could carry margins in the thirties versus the company's own high-teens. Margins in the thirties. That is the line that ends up on the slide. Here is the line that does not.

One step further down the quality ladder sits the pure micro-cap trap - Richtech Robotics is the cautionary tale. Compelling product narrative in hospitality automation, a healthy cash runway near $328 million, and then the fine print: a financial restatement across 2024 and 2025, a Nasdaq notice for a late quarterly filing, a share count that ballooned from 95.8 million to 197.7 million in a year, and a valuation at roughly 30 times sales against a sector near 2.4. Quarterly revenue of $1.1 million against operating expenses of $12.4 million is not a business yet, it is a story funded by dilution. None of that says the technology is bad. All of it says the equity is priced on faith, and faith is the most volatile input in any model.

Lesson for the whole sector. When a company sells you robotics exposure, find the robotics revenue and the robotics margin in the actual statements. If you cannot, you are buying a narrative wrapped around a different, often weaker, core business, and you are paying a robotics multiple for it.

Capital Allocation Buckets

Time to make it concrete. Everything above resolves into three buckets. Entire point is that they carry completely different payoff shapes, so they belong in different parts of a portfolio and at different sizes. An equal-weight scatter across "robotics names" is the lazy move that ignores the only distinction that matters.

Sell into all of it. Compute and safety, memory, sensing, actuation, motion control. They win whether the humanoid winner is American, Chinese, or unborn.

Nvidia is the purest version, the platform everyone trains and certifies on. Micron is the memory option priced as a data-centre stock. ABB, Fanuc, Keyence, and Teradyne own arms, vision, and motion the whole industry rents.

Profile: core weight, multi-year holds, lowest binary risk.

Proven revenue now. Surgical systems, machine vision, warehouse automation, cobots. Real cash flow with a free physical-AI option attached.

Intuitive Surgical and Zebra are the quality end. SS Innovations is the speculative end, real product and revenue, upside gated on US and EU clearance this year.

Profile: opportunistic weight, sized on entry discipline and earnings, not on hype.

A direct bet on the robot. Payoff rides on a 2028+ that assumes flawless execution against cheaper Chinese rivals, so it is binary rather than a smooth compounding curve.

Ubtech is the cleanest listed pure-play, still loss-making. Figure is a private startup retail investors simply cannot buy. Richtech is the cautionary micro-cap. Tesla is the odd one out: a profitable mega-cap where Optimus is embedded optionality, never a clean wager, since you cannot own the robot bet without also buying the cars, the energy unit, and the robotaxi promise. And the eventual humanoid winner may stay private, or Chinese, or both.

Profile: tactical weight only, sized to a risk budget you can lose outright.

For most investors the practical vehicle is an ETF (and the menu has widened fast), but the labels hide what you are actually buying. Global X's Robotics & Artificial Intelligence ETF, BOTZ, is the household name. Open the hood, though, and it is not a humanoid fund at all.

Valuation is the catch, and it is why a "hold" is defensible here. BOTZ carries a P/E above 32 against a long-run earnings growth rate near 10%, which puts its PEG north of two. No bargain, and over the trailing year it returned about 35%, beating the S&P 500 near 31% but badly lagging plain technology near 53%. Read that last comparison twice: a robotics-and-AI fund underperformed a vanilla tech ETF, because two-thirds of its weight sits in slower-growing international industrials. If you want the humanoid tilt specifically, ARK's ARKQ leans into Tesla and autonomy, Roundhill's HUMN puts Ubtech, Tesla, and Hyundai up top, and WisdomTree's WDRN deliberately targets physical AI, humanoids, and drones with, as of mid-May, no exposure to Chinese-listed robotics names. Different baskets, different bets. A label like "robotics ETF" tells you almost nothing; the holdings tell you everything.

Scenarios

Three ways the next four years can break for robotics as an investable theme, with honest probabilities. Anyone quoting you certainty on which path wins is selling something.

Notice the through-line across all three. In the base case the stack wins, in the bull case the stack still wins alongside the survivors, and in the bear case the stack survives while the pure-plays do not. That asymmetry is the whole argument. You do not need to know which scenario lands to know where the risk-adjusted return sits, which is exactly why I anchor exposure in enabling layers and proven niches rather than in a humanoid moonshot.

Bottom Line

Robotics is a genuine, multi-decade structural wave and it is also the most mis-framed theme in the market. Both statements are true, the way they usually are at the start of a build-out. Demand and revenue live today in industrial and service automation. Imagination and valuation live in humanoids. China has won the volume war on cost and scale, which means the Western edge, and the Western trade, is in the layers above and below the robot rather than in the robot itself.

So my conclusion is the one I opened with, now earned. Own toll booths, compute, safety, memory, sensing, and component layers that every robot has to buy. Own the cash registers, the surgical, vision, and logistics niches already generating real cash. Treat the humanoid pure-plays as small, sized bets you can afford to lose, not as the core of the position, because the most likely winner may be Chinese, private, or simply years from profit. That is how you get paid for Decade of the Robot without betting the outcome on a single robot maker's execution.

What would change my mind? I would move toward the humanoid pure-plays if two things happened together: a Western maker reaching profitable volume, tens of thousands of units at positive gross margin, and visible progress on US and allied actuator-and-component reshoring that cracks the China dependence. Until both print, integrated-robot bull case is slideware with serious capital behind it, and I would rather own the layers that get paid no matter who wins. Show me the margin and I will move. That is the honest line in the sand.

Research Desk, Bellwether Research, June 15, 2026