There is a pattern that repeats itself in commodity markets, reliably and almost boringly. A great company hits a rough patch - costs run higher than expected, a legal overhang clouds the outlook, China disappoints - and the market, which has a very short memory and an even shorter temper, marks the stock down to a price that implies things will stay broken forever. Then the company quietly fixes the problem, and the stock has nowhere to go but up.

That is precisely where Vale stands in December 2025. The world's largest iron ore producer is trading near multi-year lows while its direct production cost per tonne just came in at $20.7 - below its own guidance midpoint and sitting competitively between BHP and Rio Tinto. Free cash flow for the first nine months of 2025 reached $4.08 billion. Legacy dam disaster provisions are ~75% settled, with a clearly mapped schedule for what remains. And a US-China tariff truce, combined with classic Lunar New Year restocking, is providing near-term support to iron ore prices just when sentiment was at its darkest.

The market is pricing Vale as though the cost problem is permanent, China is in structural free-fall, and the dam liabilities are open-ended. We think all three of those assumptions are wrong - and the entry zone of $XX–$XX offers a meaningful margin of safety, though the degree varies significantly with entry price. The base-case DCF produces an intrinsic value that effectively sits at the upper end of the range. Entry at the lower band offers a genuine 10-13% discount to that base case - the strongest risk/reward zone. Entry at the upper band approaches or reaches the DCF base case, with upside coming primarily from the bull scenario ($100+ iron ore) rather than from a valuation discount. We recommend sizing the initial position at the lower end of the range and reserving dry powder to add if the stock tests the floor.

Vale at a Glance

Vale S.A. is the world's largest producer of iron ore - the essential raw material for steel - and one of the world's largest producers of nickel, a critical metal for electric vehicle batteries and stainless steel. Based in Rio de Janeiro, Brazil, Vale operates across more than 30 countries and ships to customers on every continent, with China representing approximately 60% of its revenues. Its Carajás complex in the Amazon is the single largest iron ore mine on earth.

Vale is, in almost every measurable sense, a company that operates at world scale. Its challenge has never been the quality of its assets - those are among the finest in the global mining industry. Its challenge has been the market's perception of its operational reliability, its legacy legal exposures, and its sensitivity to a Chinese economy that has been stubbornly reluctant to recover at pace. At $XX–$XX per share, each of those concerns is reflected - and then some.

The Cost Story - Vale's Most Important Fix

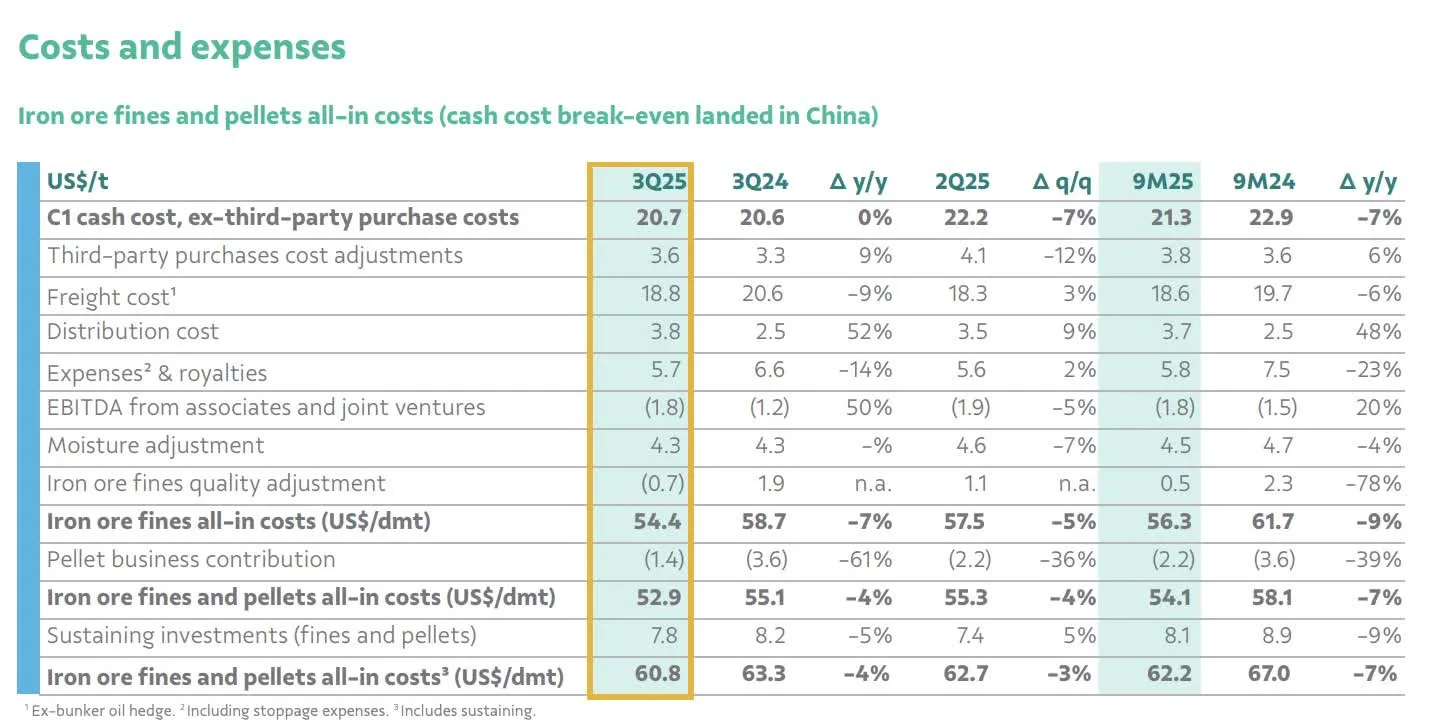

If you want to understand why Vale's stock has been under pressure for the past two years, you don't need to look at iron ore prices or China demand statistics. You need to look at one number: C1/t - the direct cost to produce one metric tonne of iron ore, excluding freight and third-party purchases. This is the number the market watches most carefully, because it's the one variable that Vale actually controls. And for a while, it was going in the wrong direction.

Rainfall disruptions, logistical bottlenecks, inventory timing issues and maintenance cycles pushed C1/t higher than guidance in several quarters - and the market responded by re-pricing the stock as if this were a permanent structural problem rather than an operational wobble. Skepticism became self-reinforcing: every guidance miss confirmed the bear narrative.

Then Q3 2025 arrived, and the picture changed materially. C1/t came in at $20.7 per tonne - a drop of 6.8% quarter-on-quarter, flat year-on-year, and below what most analysts had modelled. A full-year 2025 guidance of $20.5–$22.0/t, which had looked aspirational just two quarters ago, now looks not just achievable but potentially beatable. That single result broke the most important structural argument against Vale: that management had lost control of its cost base.

| Producer | C1 Cost (Q3 2025) | Relative Position | Cost Bar |

|---|---|---|---|

| BHP (Pilbara, FY2025) | $17.29/t | Lowest cost - premium Pilbara location | |

| Vale (Q3 2025) | $20.7/t | Mid-range - solid given logistics complexity | |

| Rio Tinto (Pilbara, 1H 2025) | $24.3/t | Highest of the three major producers |

Vale's position between BHP and Rio Tinto is actually stronger than it looks on paper, because Vale's ore comes from Brazil's Amazon basin - with higher moisture content, more complex logistics, and greater seasonal variability than the Australian Pilbara operations. That Vale can compete at $20.7/t under those conditions speaks to the efficiency of the S11D complex and the ongoing operational improvement programme.

Beyond iron ore, the cost picture in Vale's other metals divisions is also improving. Copper all-in costs fell 17% year-on-year in 2025, partly because the rising gold price is providing a significant by-product credit. Nickel all-in cost guidance was revised down approximately 7%, reflecting a more efficient operation - a meaningful positive given how much the market has worried about Vale's nickel business in a period of weak nickel prices.

"When C1/t converges to the lower end of guidance, every dollar of iron ore price becomes more margin. Trend we're seeing isn't seasonal - it's structural cost improvement. That's a valuation multiplier the market hasn't fully re-priced yet."

- Analyst commentary, Q3 2025 results reviewIron Ore: Near-Term Tailwinds, Medium-Term Realism

Iron ore is currently trading around $103.5 per tonne, up from approximately $92 in July 2025. That recovery reflects two overlapping forces - one geopolitical and one seasonal - that are providing a genuine, if temporary, lift to prices and to sentiment around Vale.

US-China Tariff Truce

In late October 2025, the US and China announced a one-year trade agreement that reduced average tariffs to 47% - a 10 percentage point reduction from the previous level - and included the temporary removal of restrictions on exports of rare earth metals. For Vale and the broader commodity complex, this matters in two ways: it reduces trade uncertainty that had been freezing Chinese industrial investment plans, and it triggers a repricing of risk for emerging market exporters like Vale, increasing the flow of foreign capital into Brazilian assets.

Seasonal Restocking and a Monsoon Effect

The Lunar New Year cycle is one of the most reliable seasonal patterns in iron ore markets. Between November and January, Chinese steel mills systematically increase their ore purchases to build inventory before the holiday. This pattern has recurred for over a decade and is well-documented in the data - it is not a surprise, but it is real. Simultaneously, Brazil's monsoon season reduces shipments from Vale's northern ports, creating supply-side pressure on futures. That DCE January 2026 contract was already trading at approximately $110/t - a 3% premium to spot - reflecting this anticipated seasonal tightness.

We want to be honest about what comes after: the medium-term picture for iron ore in 2026 is less supportive. Chinese steelmakers' hot-rolled coil margins had fallen to breakeven levels by late 2025. China's Fixed Asset Investment in the first nine months of the year turned negative year-on-year for the first time in recent memory, largely driven by a real estate sector still contracting at -9% to -10% annually. Real estate consumes roughly 30–40% of China's iron ore demand. None of that resolves quickly.

But here is the key insight for this trade: Vale doesn't need iron ore to boom for this thesis to work. With C1/t at $20.7 and iron ore holding even at $85–$90/t - a scenario more pessimistic than current consensus - Vale still generates meaningful free cash flow and sustains a dividend yield of 6–8%. Upside scenario is simply additional leverage to iron ore holding at $100+.

Important Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. Past performance does not guarantee future results. All investments carry risk, including the possible loss of principal. Vale S.A. (NYSE: VALE) is subject to commodity price risk, emerging market risk, geopolitical risk, currency risk (BRL/USD), legal liability risk related to the Brumadinho and Samarco dam disasters, and general market risk. Iron ore prices are highly volatile and may not follow the seasonal or cyclical patterns described herein. Chinese economic policy, real estate activity, and steel demand are inherently unpredictable. Brazil's interest rate environment and regulatory framework may change materially. The 10% withholding tax on dividends for non-resident shareholders may reduce effective dividend yields; investors should consult a tax advisor regarding their specific situation. DCF valuation and FCF yield estimates are based on publicly available information and independent analytical models as of December 2025; actual results may differ materially. Always conduct your own due diligence and consult a qualified financial advisor before making any investment decision.