There is something almost perverse about what has happened to Dell's stock in recent months. The company just delivered its strongest fiscal year in history - $95.6 billion in revenue, 8% growth, non-GAAP EPS of $8.14 rising 10% year-over-year, a record $10 billion in AI server shipments, and a $9 billion AI order backlog that keeps expanding every single quarter. It returned $3.9 billion to shareholders via buybacks and dividends, raised that dividend by 18%, and authorised a fresh $10 billion in buybacks. And yet the stock, as of this writing, sits around the $XX–$XX range - a 9× forward earnings multiple - while the broader market has spent the better part of the past year repricing AI exposure at premium multiples.

I have been watching this name for months, and the disconnect has grown to a point where I find it genuinely difficult to construct a bearish case that justifies the current discount. This is not a speculative AI trade. This is a hardware infrastructure company with a growing backlog, expanding margins, and two distinct growth drivers working simultaneously. The Infrastructure Solutions Group - servers, networking, storage - is operating at record margins and growing at 22% year-over-year. The Client Solutions Group - PCs, workstations, peripherals - is quiet right now but sits in front of one of the most predictable upgrade supercycles the industry has seen in years: the Windows 11 migration, with the Windows 10 end-of-life deadline in October 2025 acting as a hard forcing function.

The market is pricing Dell as though one of these two engines doesn't exist. I think both work. I think the re-rating from a discount industrial to a rightfully valued AI infrastructure and PC platform company could produce returns of 50–65% in 9–12 months. The entry zone of $XX–$XX provides a margin of safety that I find rare at this stage of the technology cycle. This is the case.

(+8% YoY)

(+10% YoY, Record)

(+22% YoY)

(Q4, +480bps QoQ)

(Growing Every Qtr)

Shipment Guidance

Market Share (IDC)

(vs. Peer Premium)

Two Engines. One Discount.

The simplest version of the Dell thesis is this: the market is applying one multiple to a company that runs two separate and independent return drivers - and doing so at a time when both drivers are simultaneously improving.

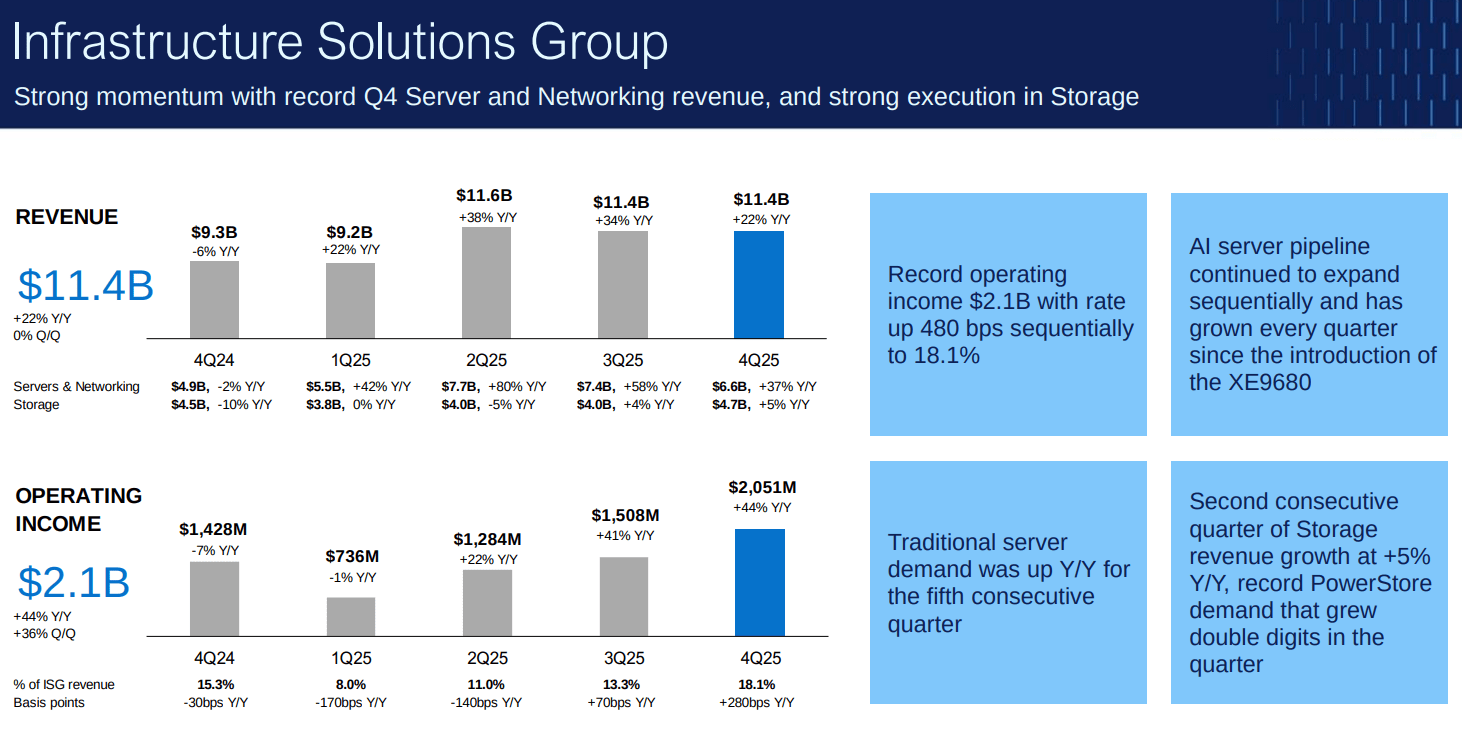

The first engine is the Infrastructure Solutions Group. This is the high-speed, high-margin business that supplies servers, networking equipment, and storage solutions to hyperscale cloud providers, enterprise data centres, and - increasingly - sovereign AI initiatives. ISG grew 29% for the full fiscal year FY25, produced record operating income of $2.1 billion in Q4 alone at an 18.1% margin, and carries a $9 billion AI server order backlog that its own CEO describes as growing "every quarter since the XE9680 was launched." This segment is a capital-light, demand-pull business with a customer concentration that reads like a who's-who of global infrastructure spending.

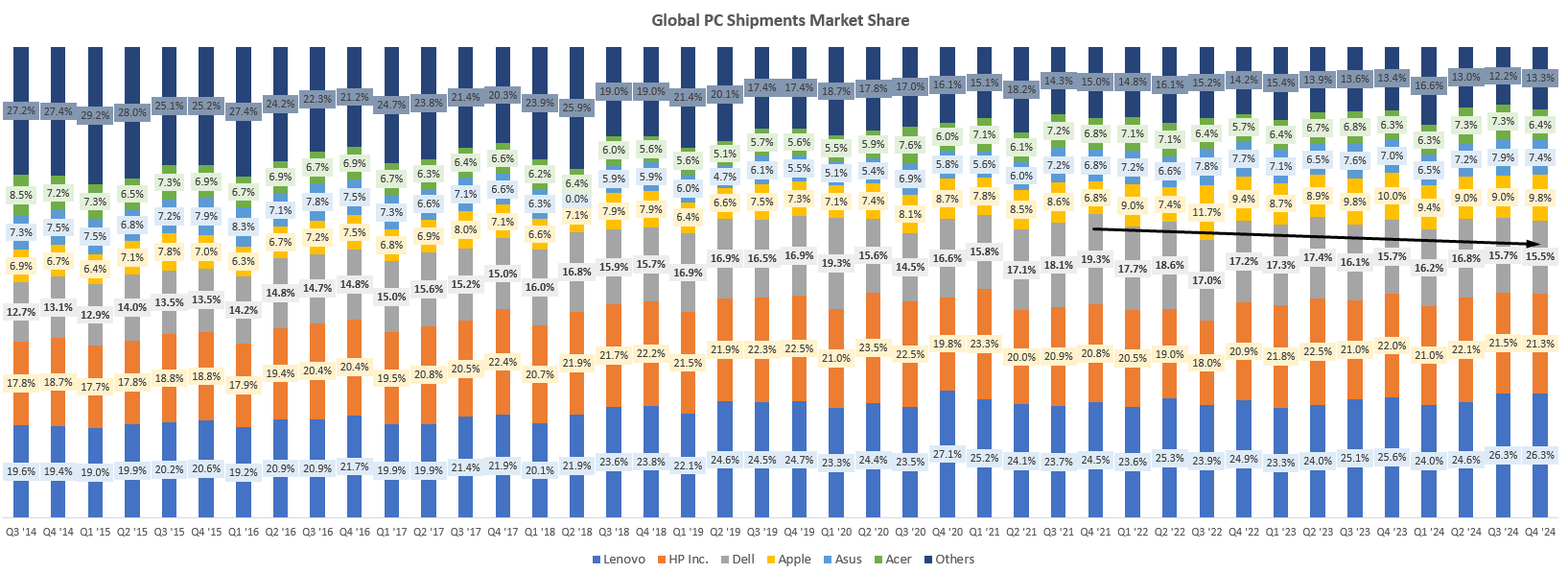

The second engine is the Client Solutions Group. This is the business that sells commercial PCs, workstations, laptops, and peripherals - primarily to enterprise customers. CSG has been a drag on sentiment because consumer revenues fell 12% in Q4 and overall CSG growth has been tepid. But the professional framing of CSG as a structurally declining business misses what is genuinely coming in the second half of 2025: the largest forced PC hardware upgrade cycle in over a decade. Windows 10 reaches end-of-life in October 2025. Microsoft has clearly stated there will be no extended consumer support. Hundreds of millions of enterprise PCs - many unable to run Windows 11 due to hardware incompatibility - will need to be replaced. Dell, with its 15% global commercial PC market share, captures a disproportionate share of that corporate refresh business.

- → Q4 revenue $11.4B, +22% YoY - fifth consecutive quarter of double-digit growth

- → AI server shipments $2.1B in Q4; full-year $10B; FY26 guidance $15B+

- → $9B backlog expanding every quarter since XE9680 launch

- → ISG operating margin 18.1% in Q4, up from 15.3% a year prior (+280bps YoY)

- → 30% mainstream server market share (IDC) - up 7 points since 2014

- → $5B xAI server deal (NVIDIA GPU-based cluster) announced February 2025

- → ISG now generates 76% of total segment operating income

- → Commercial revenue +5% YoY in Q4; demand "up double digits" per management

- → Windows 10 EoL October 2025 - enterprise refresh cycle beginning now

- → Windows 11 requires TPM 2.0 hardware - many enterprise PCs ineligible to upgrade

- → ~15% global commercial PC share; #3 globally behind Lenovo and HP

- → AI PCs launching mid-2025 - "Copilot+ PC" hardware adds $150–300 per unit premium

- → Consumer revenue decline (-12%) is not the core thesis - commercial is

- → CSG CAGR guidance of 2–3% conservative; refresh cycle could meaningfully exceed this

The Backlog Nobody Is Talking About

The number that I keep returning to - the number that strikes me as the most important single data point in the Dell story - is the $9 billion AI server backlog. This is not a soft pipeline figure. It is a firm order backlog: customer commitments, purchase orders, delivery schedules. And according to Jeff Clarke on the Q4 FY25 earnings call, it has grown every single quarter since Dell launched its XE9680 AI-optimised server platform.

To put that in context: Dell shipped $10 billion in AI servers across all of FY25. It is guiding to at least $15 billion in FY26. That $9 billion backlog - representing roughly 60% of the entire prior year's AI revenue - is already committed and queued. The revenue story for FY26 AI servers is not speculative. It is scheduled.

The xAI Deal. In February 2025, Bloomberg reported that Dell is set to supply $5 billion worth of NVIDIA GPU-based servers to Elon Musk's xAI for its artificial intelligence supercomputing project. That single deal, if confirmed in full, would represent approximately half of Dell's entire FY25 AI server revenue. It signals that Dell is not merely riding the AI infrastructure wave - it is operating as the preferred integration and deployment partner for some of the largest AI compute projects in the world.

What "AI Server" Actually Means for the P&L

One of the persistent bear arguments on Dell's AI exposure is that AI servers are lower margin than traditional servers - higher component cost (NVIDIA GPUs), lower gross margin percentage. This is true in isolation. But the argument misses the more important dynamic: the absolute dollar of profit per AI server is substantially higher than for a traditional rack server, because the average selling price difference is far larger than the margin percentage gap.

More importantly, what has actually happened to ISG margins tells a more optimistic story. ISG operating margin in Q4 FY25 was 18.1% - 280 basis points higher than a year ago, and 480 basis points higher than the previous quarter. ISG margins have improved as AI server volumes have scaled, because Dell benefits from a services, installation, networking, and storage attach-rate on each AI server deployment. The fuller the solution stack Dell sells, the better the blend. Management explicitly confirmed this dynamic on the earnings call, noting that FY26 AI server guidance of at least $15 billion includes attached services revenue.

Dell also commands structural advantages over pure-play competitors in the AI server market. Its 30% mainstream server market share - built over nearly a decade of consistent share gains from 23% in 2014 - gives it sales coverage, support infrastructure, and customer relationships that no start-up competitor can replicate. On storage, Dell holds 25–55% market share across all major categories. This installed base is the most durable moat in the enterprise infrastructure business.