There is a company in Veldhoven, Netherlands, that builds machines so complex, so capital-intensive, and so irreplaceable that every leading-edge semiconductor chip on Earth - every AI accelerator, every 2-nanometer logic wafer, every HBM memory stack - must pass through its technology before it exists. That company is ASML. It does not compete. It enables.

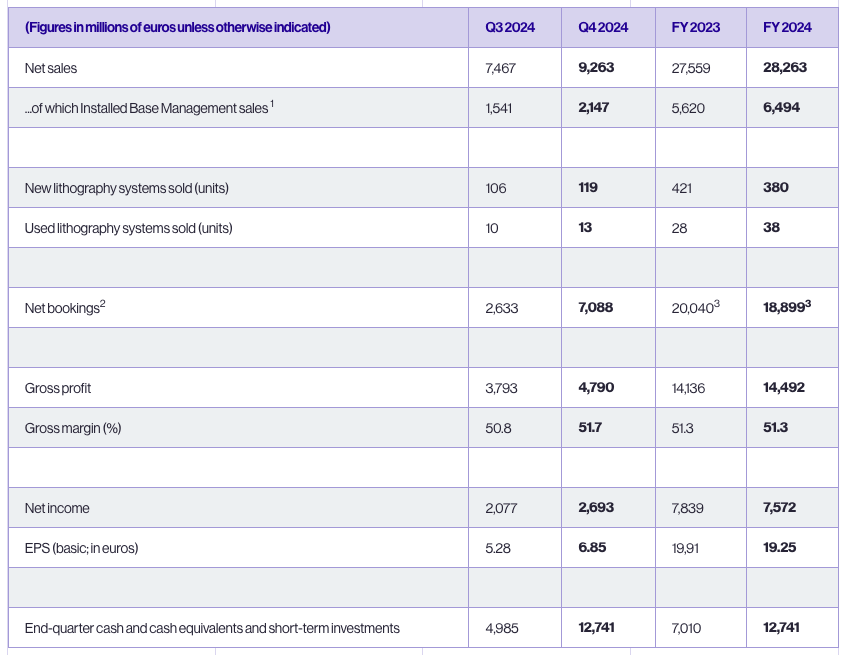

Two days ago, ASML reported Q4 2024 earnings that exceeded the high end of guidance, posted EUR 7.1 billion in net bookings against a consensus of EUR 3.5 billion, and confirmed a systems backlog of approximately EUR 36 billion. The stock sits at roughly $739, trading at 29.3x forward normalized earnings - precisely its long-term average since 2012. The question is not whether ASML is a good company. The question is whether the market has fully absorbed what the next three years look like when every hyperscaler on Earth is simultaneously building out AI compute capacity that depends entirely on ASML's machines.

We believe it has not. This is our thesis.

Start with the moat, because it is unlike anything else in technology. ASML holds a 100% monopoly on extreme ultraviolet (EUV) lithography - the technology required to manufacture chips at 7nm and below. There is no alternative supplier. There is no Chinese substitute. There is no startup in stealth mode threatening disruption. The barriers are not just high; they are, in any practical sense, impassable.

An EUV lithography system contains over 100,000 individual components, weighs approximately 180 tonnes, and requires multiple 747 cargo planes to ship. The light source alone - a CO2 laser that fires 50,000 droplets of molten tin per second, each struck twice to produce 13.5nm wavelength light - took Carl Zeiss SMT and ASML over two decades to commercialize. The mirrors inside the system are polished to atomic-level flatness; if scaled to the size of Germany, the largest imperfection would be less than one millimeter tall.

This is why ASML trades at a premium. A premium to the semiconductor sector median P/E of 31.65x, a premium to the sector median P/S of 3.37x (ASML's current P/S is 9.49x). But that premium is not valuation excess - it is the market's recognition that ASML's competitive position is closer to a natural monopoly than to a typical tech company. What the market has yet to fully price, we believe, is the volume and duration of the demand cycle now unfolding.

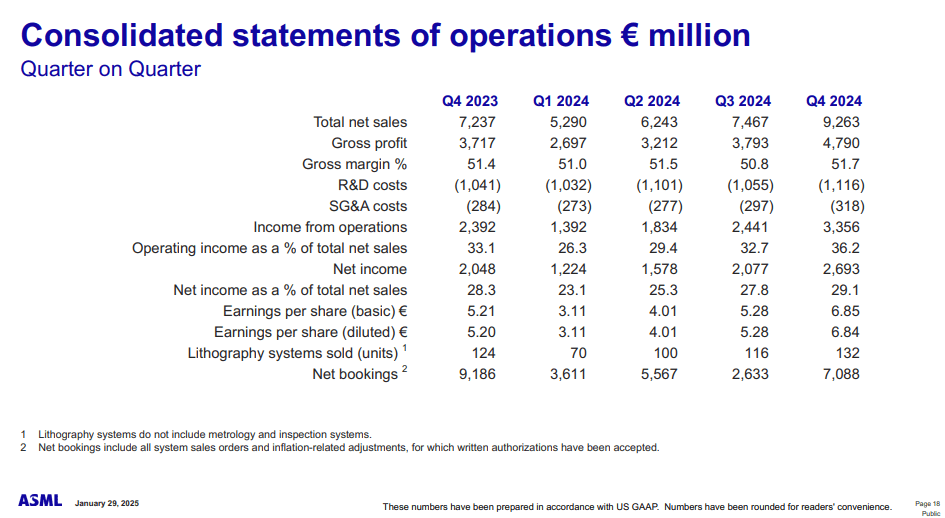

Context matters here. In Q3 2024, ASML posted net bookings of just EUR 2.6 billion against expectations of EUR 5.6 billion. The stock dropped approximately 20% in a single session - one of the worst single-day declines for a European large-cap in years. The narrative shifted overnight: the AI demand cycle was peaking, customers were pulling back, ASML's guidance range of EUR 30-35 billion for 2025 looked like a ceiling rather than a floor.

Then Q4 happened.

Net sales came in at EUR 9.263 billion, above the high end of guidance. That is not a marginal beat. It is a company telling the market "our numbers will be between X and Y" and then exceeding Y - in a quarter where installed base revenue contributed an outsized EUR 2.1 billion (reflecting upgrade business that exceeded internal plans). Gross margin printed at 51.7%, up from 50.8% in Q3, driven partly by lower-than-planned costs on High-NA system introductions - a signal that the new technology is maturing faster than ASML's own financial models assumed.

But the real headline was bookings. EUR 7.088 billion in net system bookings - EUR 3 billion of that in EUV, EUR 4.1 billion in non-EUV - against a consensus expectation of approximately EUR 3.5 billion. This was a 2x beat on bookings. The message from customers was unambiguous: they are ordering. They are building. The demand is real.

"Total net sales were EUR 9.3 billion, which is above the high end of our guidance primarily due to installed base revenue. Gross margin for the quarter was above guidance at 51.7% due to a combination of additional upgrade business and lower than planned costs associated with the new product introduction of High-NA systems in the field."

- Roger Dassen, EVP & CFO, ASML Q4 2024 Earnings CallFull-year 2024 revenue reached EUR 28.263 billion with a gross margin of 51.3%. Net income for the year was EUR 7.6 billion (EUR 19.25 per share), and free cash flow was EUR 9.1 billion. The company returned EUR 3 billion to shareholders through dividends and buybacks and declared a total 2024 dividend of EUR 6.40 per share.