Every few years a new crop of investors stumbles onto the same argument and acts like they've just split the atom: "Why bother with bonds? Stocks always win over the long run." The logic feels airtight. Charts back it up nicely. And if you happen to be 30 with decades of compounding runway ahead, dumping everything into equities seems almost too obvious to question. So why would anyone voluntarily sign up for lower returns?

I've heard this pitch from people far smarter than me. Brilliant, genuinely thoughtful investors. I have also sat across from those same people during March 2020 - portfolios cratered 34% in five weeks, zero dry powder anywhere, not a single dollar free to buy anything at fire-sale prices. They were technically right about the long run. But they could not survive the short run. And that's the part that somehow never makes it into the pitch deck. The long-run average is correct, sure. Technically. But averages don't retire. You do. Your specific decades are what matter - your specific market environment, your income trajectory, the sequence of returns you happen to draw from the cosmic hat. That is what actually decides whether you're eating cat food at 72 or flying business class.

And here is what keeps nagging at me whenever this debate resurfaces: the research behind "stocks always win" is far shakier than most people realize. Professor Edward McQuarrie at Santa Clara University spent years piecing together 19th-century bond market data that earlier researchers had either botched or flat-out ignored. What he found blew a hole in a cornerstone assumption - stocks' historical dominance leans hard on a narrow, unusually favorable 20th-century window. Before that? Bonds held their own for decades at a time. Sometimes they won outright. Then in 2022, the bond-equity relationship that underpins most diversification theory broke down completely. And the 2025 tariff shock stress-tested it again in ways that lay bare just how conditional - not absolute - the whole bond-as-diversifier story really is.

What follows is the honest, messy, complicated version of why not 100% stocks. Not the textbook version. Not the version your financial planner recites from a script.

The Assumption We Never Questioned

The intellectual backbone of "stocks for the long run" traces mostly to Jeremy Siegel's book of the same name. Important work - genuinely. It reshaped how a whole generation of financial planners think about allocation. Siegel pulled historical data showing stocks crushing bonds from 1926 to present. The chart became famous. The conclusion calcified into dogma. And nobody - for years, for decades - thought to ask a pretty basic question: why does the data start in 1926?

That is the crack in the foundation. And it's a big one. What most investors have no idea about (and what I certainly didn't know until I went down this rabbit hole) is that the data before 1926 - everything before the standard starting point everyone leans on so confidently - paints a very different picture. Professor Edward McQuarrie spent years reconstructing actual US bond market returns from 1793 onward, using real bond prices and coupon payments from genuine market transactions. Not theoretical models. Not estimated yields. Prices people actually paid and coupons they actually collected. His findings, published in "The US Bond Market Before 1926: Investor Total Return from 1793," kicked a cornerstone loose from what most of us assumed was settled science. The floor shifted, and almost nobody in the retail investing world noticed.

Stocks Always Win Long-Term

Post-1926 data shows stocks dramatically outperforming bonds across every major long-term horizon. The takeaway looked simple: for long-horizon investors, equities dominate, period. Bonds just reduce volatility at the cost of expected returns. Clean story. Persuasive story. One problem though - and it's not small.

1926 to 2025 is a single data window. One sample. And it happens to capture the greatest period of US industrial and economic expansion in human history - powered by demographics, policy choices, and a global order that frankly don't exist in the same form anymore.

Stocks' Dominance Is a 20th-Century Phenomenon

McQuarrie found that in the 19th century, long-term bonds didn't just keep pace with equities - they outperformed over multi-decade stretches. After the Panic of 1837, through the post-Civil War deflationary era, and across other long periods, bonds delivered superior real returns. Not by a little, either.

Siegel's earlier datasets had leaned on synthetic or estimated bond returns, often borrowing New England municipal yields that came with unique tax privileges - systematically understating what bonds actually returned before 1926. The data was wrong. Plain and simple. The whole house of cards sat on a crooked foundation.

This is not some minor academic footnote you can wave away at a dinner party. If stocks' dominance is primarily a product of a specific 20th-century setup - post-WWII industrial expansion, baby boom demographics, accommodative monetary policy, the dollar's unchallenged reign as global reserve currency - then the confidence with which we project that dominance onto your next 40 years should drop. Considerably. McQuarrie isn't saying bonds will outperform going forward. He is saying the margin of certainty most investors carry around is dramatically wider than the data actually supports. There's a canyon between "stocks probably outperform" and "stocks always outperform." Most people live their financial lives in that canyon without realizing they're there.

Think about this for a second: you get one investment lifetime. One. The sample of truly independent 40-year periods in the modern data is essentially two. Two. Would you stake your retirement on a sample size of two? Because that is what going 100% stocks implicitly requires you to believe - that the next few decades will rhyme closely enough with the last century's charmed run to justify zero hedging. It's a bit like watching Lebron hit a half-court shot twice and concluding he'll nail it every time. Maybe. But would you bet the house on it?

The 2022 Wake-Up Call: When the Relationship Broke

Even investors who acknowledged some theoretical wobble in the long-run equity story still counted on one relationship with near-religious confidence: when stocks fall, bonds rise. This negative correlation was the load-bearing wall of modern portfolio theory. It powered the 60/40 portfolio. It sat behind every "safe" allocation recommendation advisors cranked out for twenty straight years. Nobody questioned it because the thing just kept working. Like a dishwasher you forget exists until it floods the kitchen.

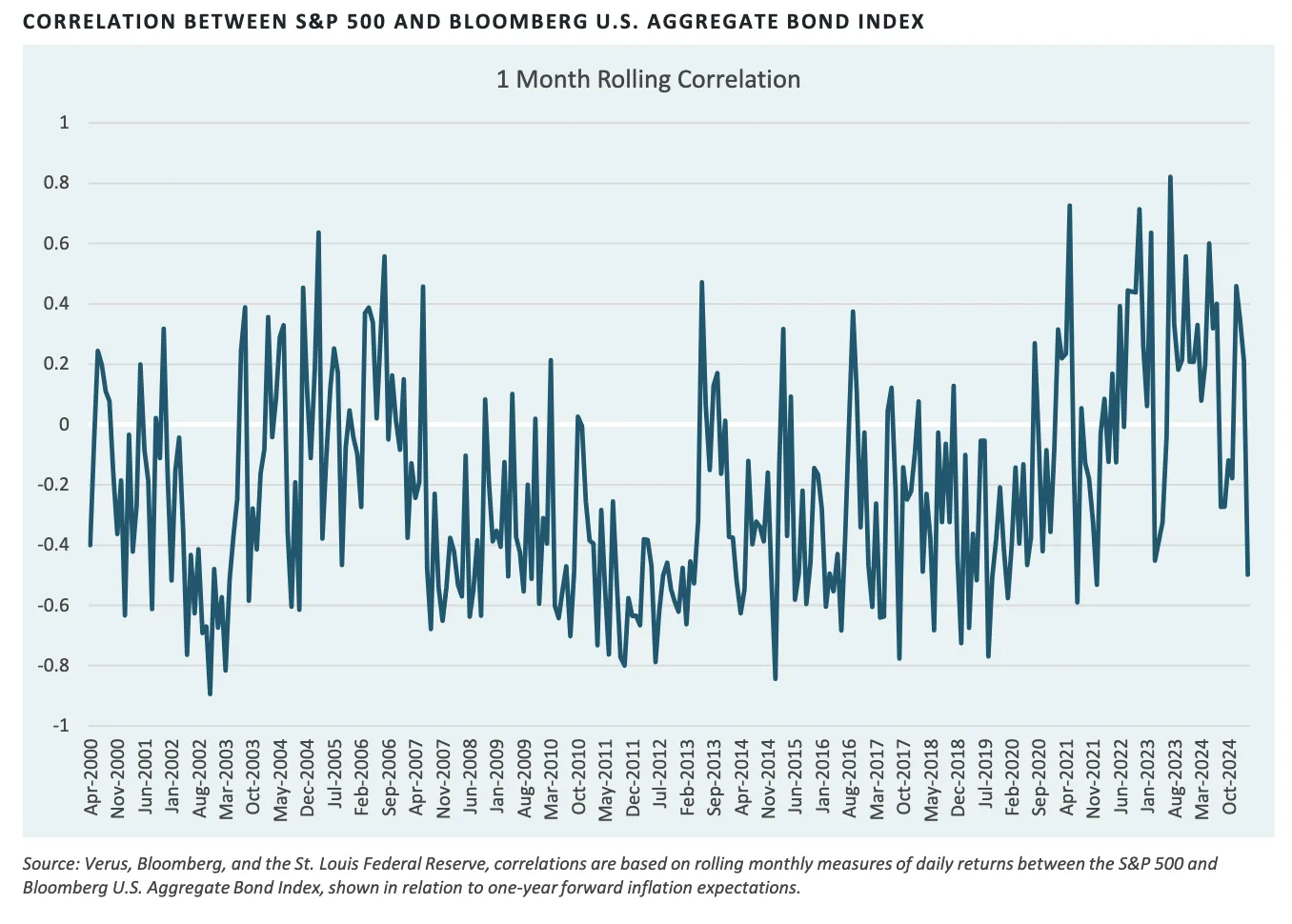

Then 2022 happened. The Fed launched the fastest rate-hiking cycle in four decades to wrestle down inflation that had been building since 2021. Bonds - which mechanically lose value when rates climb - got hammered. Stocks fell at the same time because rising rates and recession fears crushed equity valuations. Both asset classes lost money. Simultaneously. For the entire calendar year. The 60/40 portfolio posted its worst annual result since the 1930s. And that negative correlation everyone's retirement plan was banking on? Gone. Just gone. Two asset classes that were supposed to zig and zag in opposite directions zigged together, month after month, like two drunks leaning on each other stumbling down the same hill. I remember watching it unfold in real time thinking, well, so much for textbook diversification.

The chart tells that story better than words can. For roughly twenty years - 2000 through 2021 - rolling correlation between S&P 500 and bond returns stayed predominantly negative. Stocks dropped, bonds gained. And this was not a coincidence or some lucky streak. It reflected a very specific macro setup: low inflation, interest rates drifting lower over decades, and a Federal Reserve that reliably cut rates whenever equity markets wobbled. That environment made the bond-as-diversifier thesis not just theory but something mechanically reliable. You could set your watch by it.

What 2022 showed - and it showed this with zero ambiguity, with brutal clarity - is that the diversification relationship is conditional on the inflation environment. When inflation runs hot, the Fed tightens. Rates rise. Bond prices fall. Stocks fall simultaneously because higher rates shrink the present value of future earnings. Same driver hammering both at once. The negative correlation flips positive. The diversification you were counting on vanishes at the precise moment you need it most. (What good is an umbrella that dissolves in rain?) It is like finding out your home insurance carries a carve-out for the one type of disaster that actually occurs in your neighborhood.

Negative Correlation Era

Low inflation, falling rates, Fed cutting on equity stress. Bonds reliably rose when stocks fell. The 60/40 portfolio's golden era.

Both Fall Together

Fastest rate-hike cycle in 40 years. Inflation drove both stocks and bonds lower simultaneously. The 60/40's worst year since the 1930s.

Oscillating, Uncertain

Correlation unstable, regime-dependent. Some restoration of negative relationship as inflation slowed, but not the reliable pattern of pre-2022.

Tariff Shock Test

Treasury yields rose while stocks fell - the opposite of expected safe-haven behavior. A new driver: foreign selling of US Treasuries by China and Japan.

The 2025 Tariff Shock: A New Wrinkle

What happened in April 2025 genuinely spooked people who watch fixed income for a living. The tariff announcements hit, stocks sold off - and Treasury yields went up. That is backwards. When equities crash, money is supposed to pour into Treasuries, pushing bond prices higher and yields lower. That's the playbook. Instead, 10-year yields climbed from roughly 4.0% before the April 2 announcements to 4.5% by April 11. Bonds fell while stocks fell. For a brief, deeply unsettling stretch, neither asset class was doing its job.

Morningstar dug into this episode and their analysis is worth reading carefully. Several explanations surfaced: foreign governments - China and Japan specifically - appear to have been dumping US Treasuries, draining demand at precisely the moment domestic investors needed those bonds as a safe haven. Tariff-driven inflation expectations piled on top. So investors found themselves whipsawed between recession risk (which normally pulls yields down) and inflation risk (which shoves them up). The two forces partially canceled each other out and left bonds behaving erratically. Not the dependable ballast everyone's allocation spreadsheet assumed. More like a weather vane spinning in a hurricane.

The Crucial Context That Got Buried

Despite that yield spike during peak tariff uncertainty, the bigger picture is actually less scary for bond holders than the headlines suggested. Since market turbulence kicked off on February 19, 2025, the Morningstar US Market Index has lost nearly 13%. Over the same window, long- and intermediate-term Treasuries posted small gains. So the recent episode was a short-term disruption inside a longer-term pattern that largely held. And today's higher starting yields - the 10-year sitting at ~4.3% versus 1.76% at the start of 2022 - provide meaningful cushion against price declines. That is a materially different starting point from 2022, and it matters a great deal for anyone sizing up bonds' current protective value.

So are bonds broken? No. But here's what you need to actually internalize, not just nod along to: bond diversification is probabilistic and environment-dependent. It is not guaranteed. It's not some mechanical law of physics like gravity. Understanding the specific conditions where bonds fail as diversifiers - high inflation paired with foreign selling pressure on US Treasuries - lets you make better decisions about how much to hold and when plain old cash might serve you better. The key word in all of this is "conditional." Anyone who tells you bonds always protect against stock losses is either oversimplifying to the point of dishonesty or just hasn't been paying close attention since 2021.

The Battery Concept: Why Rebalancing Still Works

Even granting everything I just laid out - the shakier historical foundation, the 2022 correlation blowup, the 2025 tariff weirdness - there's still a powerful argument for holding bonds that has nothing to do with textbook diversification. It is the rebalancing argument. Market historians have called it the "battery concept." And frankly, I think this is the single most compelling reason to own bonds that nobody spends nearly enough time on.

Discharging During Crashes

When stocks fall hard, your bond allocation holds value while equities go on sale. Rebalancing means selling bonds and buying depressed equities - the exact trade every investor swears they want to make but almost nobody pulls off emotionally without a mechanical rule forcing it. The bonds fund the purchase. Without them, you'd need earned income to buy the dip. And earned income tends to be scarce during recessions - which are, of course, precisely when stocks are cheapest. The cruelest timing in all of investing. Like a fire sale at a store that only opens when your wallet is empty.

Recharging During Bull Markets

When stocks rally and your equity allocation drifts above target, rebalancing means selling some equities and buying bonds. You are systematically taking profits at elevated prices and restocking your reserve for the next downturn. This is selling high - literally the thing every investor claims they want to do. But without a rule forcing the trade, the gravitational pull of a rising market makes it almost psychologically impossible. "Why would I sell when everything's going up?" Because the battery needs recharging. That's why. Because euphoria is not a strategy.

People consistently underestimate the timing dimension here. Crashes don't politely show up when you're flush with cash and feeling great about your career prospects. They arrive during economic downturns - when bonuses evaporate, job security gets wobbly, emergency bills spike, and fresh investment dollars dry up completely. The 2020 Covid crash compressed 34% of losses into five weeks. So who actually bought the March 2020 lows and rode that extraordinary recovery? Not people who happened to receive a windfall in late March. It was the ones who had built reserves - bonds, cash, or both - during the fat years before. They had a battery. And they discharged it at exactly the right moment.

McQuarrie's research adds something else that tends to get overlooked. Bond yields tend to rise during economic expansions and fall during recessions. That creates a natural counterbalancing dynamic where bonds appreciate in value right when the rebalancing opportunity is juiciest - when stocks are cheap and you desperately want to be buying them. Not a coincidence. This is the mechanism through which bonds earn their seat at the table even when their standalone returns look boring. A 4% bond return sounds like watching paint dry. Until you realize it is what funded your ability to scoop up stocks at 2009 prices. Then it sounds like genius.

Not All Bonds Are Created Equal

Here's a mistake I see constantly after episodes like 2022 or the April 2025 tariff spike: someone throws their hands up and declares "bonds failed." But the bonds that behaved worst - long-duration Treasuries and high-yield corporate junk - aren't the same instruments that should be serving the battery function in your portfolio. This distinction is not some technical nitpick. It is the difference between diversification that actually works and diversification that's just a comforting illusion you're paying for with lower returns. You have to know which bonds sit where. And why.

Short-to-Intermediate Government & Investment-Grade

These are the bonds that actually do what people think all bonds do. Short duration keeps sensitivity to rate changes in check; high credit quality means they don't suddenly start behaving like stocks when credit stress hits. Morningstar specifically flags core and core-plus intermediate bond funds as the best equity ballast out there. This is where your battery should be built. Not the flashy stuff. The boring stuff that works.

Long-Duration Government Bonds

Fantastic in falling-rate environments - the most valuable bonds you can own during a 2008-style deflationary meltdown. But they carry enormous interest rate risk when rates are climbing. In 2022, long Treasuries fell 25%+. That's not a typo. Stock-like volatility in what is supposed to be the safe part of your portfolio. Better deployed as a tactical position when you have a genuine view on rates than as a permanent core holding. Know what you own and why you own it.

High-Yield / Junk Bonds

These are bonds in name only when it comes to diversification. During market stress, high-yield bonds act like stocks - credit spreads blow out, prices crater, and they tumble right alongside equities. The exact opposite of what you need from the bond sleeve. Sure, they pay more income. Looks great on a yield screen. But when the crash arrives they offer zero shelter. If you hold HYG or JNK and think you're hedged against equity risk, I don't know how to say this gently, but you're not.

Morningstar also raises a point I find increasingly hard to argue with: cash - specifically Treasury bills, the shortest-duration instruments out there - has been the best equity diversifier over the past three years. T-bills outperformed longer bonds precisely because they are immune to the interest rate risk that wrecked bond funds in 2022. For investors who need to spend from their portfolio within the next couple of years, individual bonds held to maturity or defined-maturity "bond ladder" funds eliminate price volatility entirely. You know exactly what you're getting at maturity, and the interim price fluctuations? Irrelevant. Because you aren't selling. Unsexy? Absolutely. But this kind of practical, boring, nobody-writes-articles-about-it strategy is the kind that actually works when you need it to.

The TIPS Case - Inflation Protection That Matters

TIPS (Treasury Inflation-Protected Securities) deserve their own spotlight here because they address the single most common objection to owning bonds: "inflation will eat my returns." TIPS adjust their principal value with CPI, so the real purchasing power of your investment stays protected. In a portfolio context, they behave like traditional Treasuries during deflationary stress while also shielding you against the exact scenario - high, persistent inflation - where both stocks and regular bonds get hammered at the same time. Morningstar specifically recommends TIPS as a complement to nominal bonds for anyone drawing income from their portfolio. Think of them as the one fixed-income instrument specifically engineered for the environment that breaks everything else. The financial equivalent of a generator that only turns on during blackouts.

The Practical Allocation Framework

So after all this - the wobbly historical case, the conditional nature of bond diversification, the real but imperfect value of the rebalancing battery - how should you actually think about allocation? Honestly? There is no universal answer. Anyone handing you a universal answer is selling something. (Probably a fund.) But there is a framework for working through the variables that matter for your particular situation, and that's what the table below attempts to lay out.

| Investor Profile | Suggested Range | Reasoning | Bond Type |

|---|---|---|---|

| 25–35, stable income, high risk tolerance | 80–85% stocks | Long horizon, recession recovery ability, steady contributions provide some natural rebalancing | Intermediate-term Treasuries / core bond fund for the 15–20% |

| 35–50, moderate income stability | 70–75% stocks | Rebalancing benefits are highest over this horizon; portfolio size makes drawdown recovery more consequential | Mix of intermediate bonds and TIPS; cash buffer for 1–2 years expenses |

| 50–60, approaching retirement | 55–65% stocks | Sequence-of-returns risk becomes material; a bad decade early in retirement has permanently impaired outcomes | Individual bonds / bond ladders for spending needs; TIPS for inflation protection |

| Retired, drawing from portfolio | 40–55% stocks | Preservation of spending power matters; bonds fund near-term withdrawals without forced equity sales | Short-to-intermediate Treasuries for 2–3 year spending needs; growth equities for the long tail |

| Any profile, guaranteed pension income | Can increase by 5–10% | Pension acts as a bond - reduces need for portfolio bond allocation proportionally | The guaranteed income stream functions as a very long duration bond in practice |

"The 100% stocks debate is almost always framed as a question about expected returns. That's the wrong framing. It should be about optionality and timing. Bonds aren't in a portfolio primarily to smooth out the ride - they're there so you have purchasing power available at the exact moments when buying equities is most valuable and your earned income is most scarce. Yes, 2022 was a genuine warning that bond diversification is conditional, not guaranteed. But the rebalancing mechanism - the battery - works regardless of what the bond-equity correlation is doing in any given year, as long as you're holding high-quality instruments that maintain value during equity stress. The lesson from 2022 is not 'avoid bonds.' It's 'hold the right bonds and size them for your specific situation.' There's a world of difference between those two conclusions."

Conclusion: One Lifetime, One Portfolio

The "stocks always win over the long run" argument has a fatal flaw baked right into its framing: the long run isn't some statistical average spread across millions of hypothetical investor lifetimes. It is your specific decades. Your market environment. Your income trajectory, your spending needs, your health scares and career detours and the thousand other things nobody puts into a Monte Carlo simulation. Japan's Nikkei took 34 years - thirty-four years - to claw back to its 1989 peak. An investor who retired in 1999 with 100% S&P 500 had negative real returns for their first decade of retirement. The stretch from 1966 to 1981 produced negative real returns for US equity investors. These are not obscure thought experiments cooked up by academics with an axe to grind. They happened. To real people. With real retirements to fund and real grocery bills to pay.

McQuarrie's work pushes the lens even further back, and the picture only gets harder for the "stocks always win" crowd. The data window supporting that conclusion is genuinely narrow. Bonds' historical performance before 1926 was substantially better than Siegel's reconstructed datasets suggested. We are more uncertain about the long-run equity premium than any textbook will admit. And that uncertainty alone - just the uncertainty, forget everything else I've written here - justifies holding some bonds. Not as a prediction that bonds will outperform. But as insurance against the possibility that the next 40 years won't look like the last hundred.

Key Takeaways

The historical case for stocks' superiority rests on less than 100 years of data and two fully independent 40-year periods. McQuarrie's work on pre-1926 bond markets shows bonds outperforming equities across multi-decade stretches in the 19th century. The confidence with which people state "stocks always win long-term" dramatically exceeds what the data actually supports. Be honest with yourself about that gap. It is wider than you think.

Bond diversification is conditional on the inflation environment, not guaranteed. 2022 proved this conclusively; the April 2025 tariff shock tested it again. If you want the battery function to work reliably across different regimes, hold high-quality, short-to-intermediate duration bonds. Not long-duration. Not high-yield. Those are completely different instruments doing completely different things, and confusing them is exactly how people end up saying "bonds failed me" when really they just owned the wrong bonds.

The most powerful argument for bonds isn't about juicing returns or smoothing volatility. It is about optionality at the moment of maximum opportunity - having purchasing power on hand when equities are dirt cheap and your paycheck is hardest to come by. Cash and individual bonds held to maturity complement bond funds for anyone with near-term spending needs. You get one investment lifetime. Size the insurance accordingly.

Research Desk, Bellwether Research, May 18, 2025