Photonics has spent three decades as the quiet plumbing of the internet. Undersea cables. Long-haul fibre. Stuff consumers never thought about and investors rarely priced. That is changing in front of us, and this study is an attempt to pin down exactly what has changed, how permanent the change is, and which companies inside the industry are building something durable versus which are simply being lifted by the tide.

Trigger is narrower than headlines suggest. AI broadly is not the story. A specific engineering problem is - how do you get tens of thousands of GPUs to exchange data in lockstep without copper wiring between them overheating, losing signal, or running out of bandwidth? Copper breaks at the speeds a next-generation AI cluster needs. Light does not. And so a chunk of AI capex is now being redirected, quietly, into companies most investors had never looked at eighteen months ago - makers of indium phosphide laser chips, thin-film lithium niobate modulators, specialty fibres, photonic integrated circuit foundries, co-packaged optics roadmaps.

Nvidia confirmed the shift in cash in March. $2 billion into Lumentum. $2 billion into Coherent. A third $2 billion into Marvell. Ecosystem commitments across Corning, Celestica, and several silicon photonics foundries. Jensen Huang used GTC 2026 to name optical computing interconnects a core future technology - not as an aside, but as a central architectural claim. When a buyer with that much supply-chain leverage spends $6 billion on one layer of the stack in three weeks, markets have to take the layer seriously.

This study has three purposes. First, to map how optical networking actually works as a stack - who makes what, who sits where, how money flows through a value chain. Second, to test whether surging interest reflects a durable structural re-plumbing of AI infrastructure or a hype cycle that will wash out in the next capex digestion phase. Third, to separate genuine compounders - companies with defensible moats, supply tightness, and execution records - from names that are simply moving because tide conditions lift everything. Both kinds can print returns. Only one kind survives a correction.

Bottleneck Nobody Paid Attention To

Picture this. You are a hyperscaler. You have spent eighteen months convincing your CFO to approve $40 billion of GPU capex because the training clusters on your AI roadmap need it. Racks show up. GPUs go in. And then your network team walks into a meeting and explains, politely, that the training job is running at 58% of theoretical throughput because the interconnect fabric cannot keep up. Every. Single. Quarter. That conversation is happening in every major AI data center on the planet right now.

Mechanics are ugly. A modern training run is not one GPU doing work in isolation - it is tens of thousands of GPUs exchanging gradients, weights, and activations in lockstep. One rack waits for data - whole cluster stalls. Nvidia's Spectrum-X networking documentation puts it in engineering language, but the analyst translation is this: bandwidth demand per GPU has roughly doubled every eighteen months while the physical power budget per transceiver has stayed roughly flat. Copper cannot hit that curve. It cannot. Signal loss, heat dissipation, serialiser-deserialiser overhead - all of it breaks at the speeds a 72-GPU NVL72 rack needs to push.

That is why the industry has spent 2025 and now 2026 racing up the bandwidth ladder. 400G was the cloud standard in 2022. 800G became the AI-training standard in 2024. 1.6T per port - 1.6 terabits per second - is the target for Q3 2026 volume shipment, with 3.2T already on the whiteboard for 2028. A single 1.6T transceiver pushes roughly thirty 4K Netflix streams through a pair of fibres every second, continuously, in both directions, for years without a break.

For investors, what matters is simpler than engineering suggests. Hitting those bandwidth targets requires replacing copper wiring with light. Not in the backbone - that happened decades ago - but inside racks themselves, and eventually right next to the chip. That is a multi-year re-plumbing of AI compute, and whoever supplies that plumbing is now sitting on some of the tightest supply-demand dynamics in semiconductors.

"Conventional copper cables consume a great deal of power over long distances, while fiber is relatively more efficient. When tens of thousands of GPUs need to exchange data in real time, transmission speeds of 1.6 terabytes or more are essential. The optical-communications ecosystem will continue to expand."- Securities analyst, quoted in Korean industry coverage following Jensen Huang's GTC 2026 remarks on optical computing interconnects

How This Stack Actually Works

Quick orientation, because you need this to judge the names. Optical networking has four physical layers, and they have wildly different economics.

Laser. A tiny semiconductor chip that generates light at a specific wavelength. Indium phosphide (InP) dominates here because it lases efficiently at the infrared wavelengths fibre loves. This is the hardest part of the stack to manufacture. Coherent and Lumentum are the two Western companies that matter, and supply is genuinely tight. Coherent's decision to roughly double InP capacity over the last twelve months was not optional - it was survival.

Modulator. A component that turns a steady laser beam into a binary data stream by shifting its phase, amplitude, or polarisation at multi-gigahertz rates. This is where exotic materials live - silicon (cheap, scalable, power-hungry), lithium niobate on insulator (fast, efficient, harder to manufacture), and newer barium titanate platforms that Lightmatter and a handful of start-ups are chasing. Bandwidth-per-watt is won or lost here.

Transceiver module. A pluggable package - laser, modulator, detector, control electronics - that slots into a switch or server port. Lumentum, Coherent, Applied Optoelectronics, and Innolight (private, Chinese) supply these to hyperscalers. Margins compress fast as volumes ramp, which is why every module maker is now talking about moving up-stack.

Fibre and connectors. Actual glass. Corning dominates global fibre. Its Meta contract alone - a multi-year, roughly $6B agreement - is a kind of deal that used to take a decade to produce. Now they are announced on quarterly earnings calls. Above these four physical layers sits switch silicon - Broadcom Tomahawk, Marvell Teralynx, Nvidia Spectrum-X - and the network architecture that wires it all together.

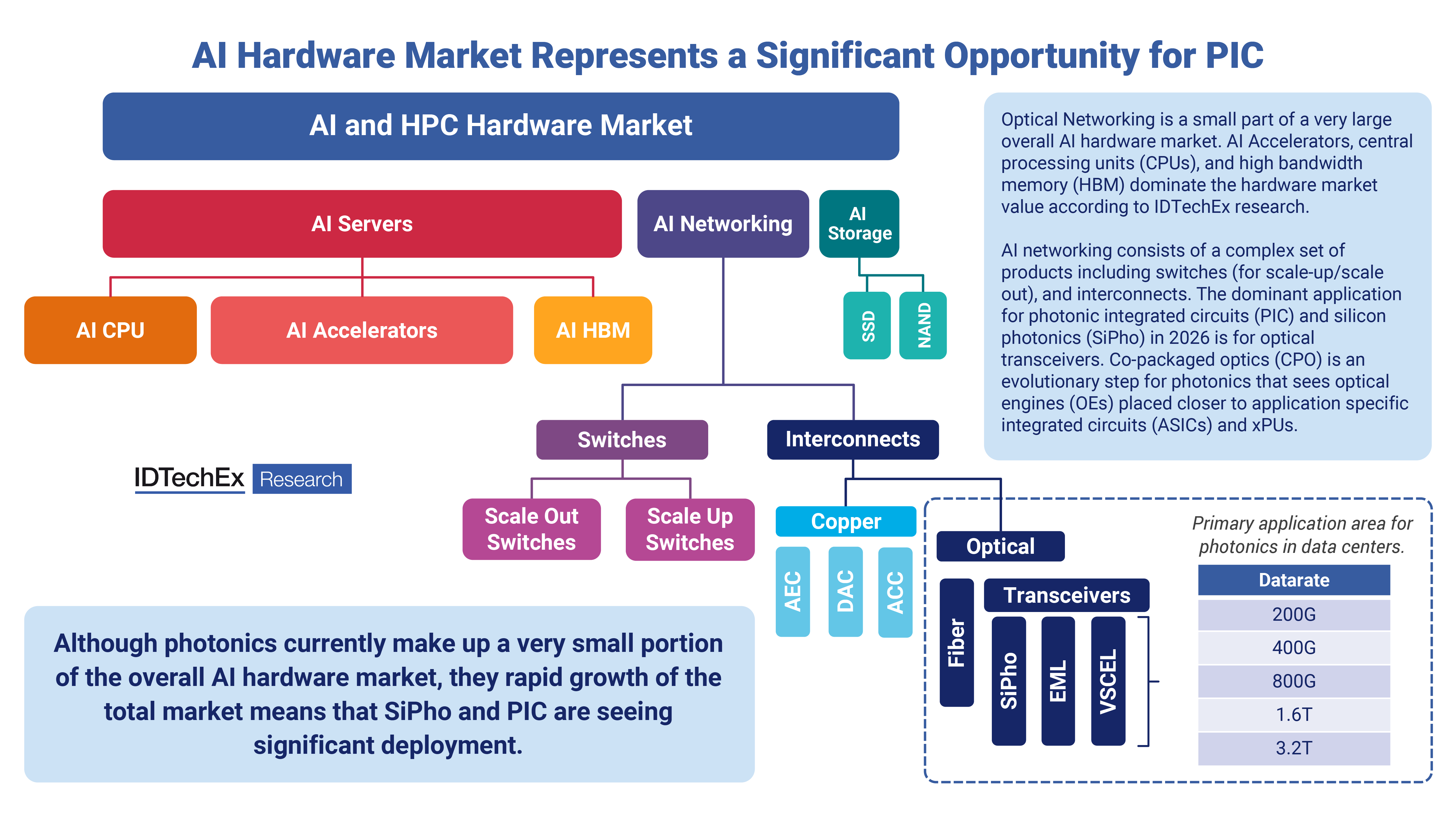

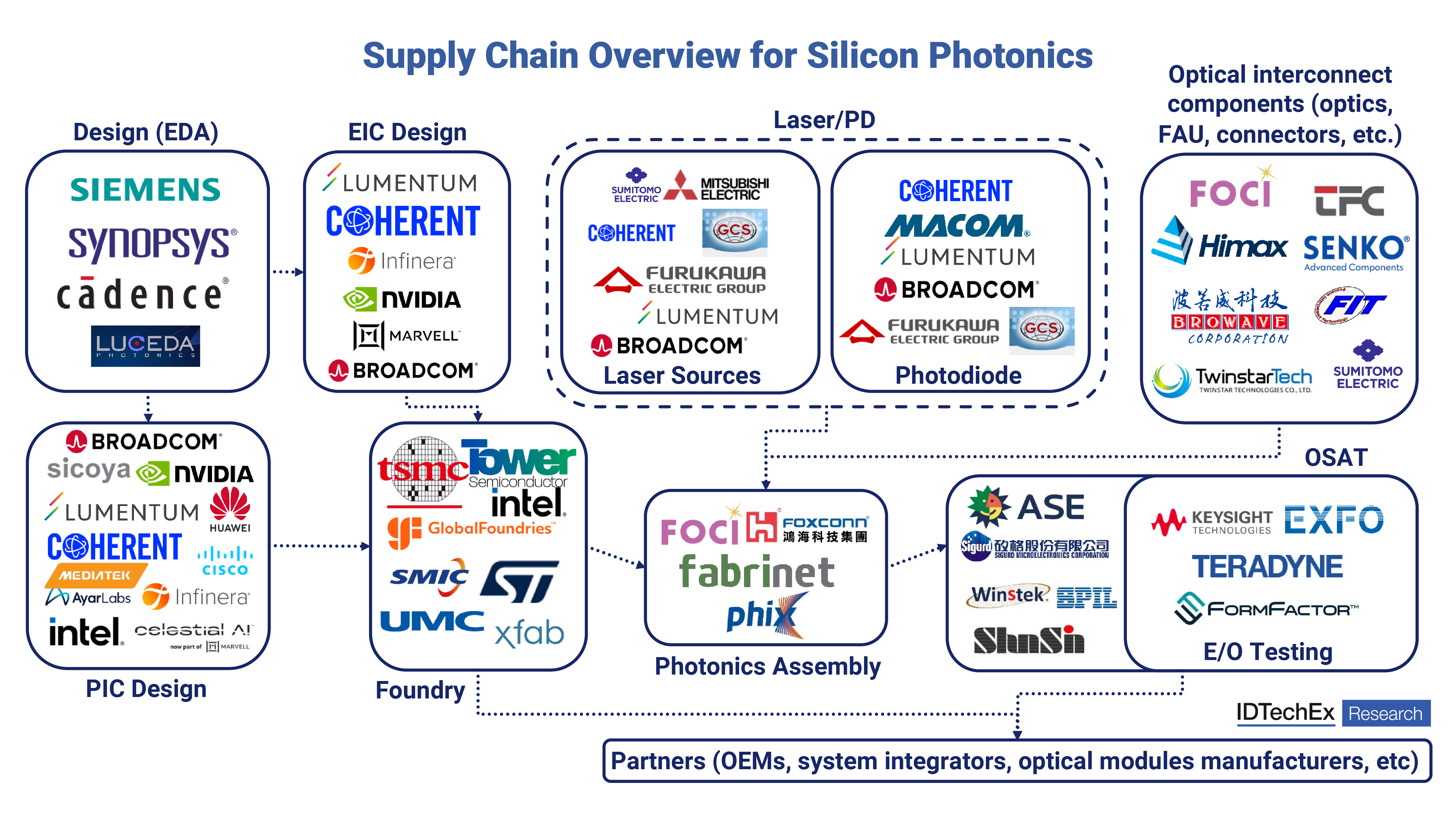

Two pieces of IDTechEx research are worth pinning to the wall before we go any further. One maps the broad AI-hardware market and identifies a specific slice - photonic integrated circuits - where optical spend is landing. Another shows the actual company-by-company supply chain for silicon photonics, laid out by layer. Investors who can read both of these have a meaningful edge over investors who are choosing names by press release.

Read these two maps together and the analyst takeaway is simple. Opportunity is real because AI hardware is structurally consuming more light. Supply is bottlenecked because the production network behind that light is dense, specialised, and capital-intensive. Western publicly-traded names sit at specific, identifiable nodes inside that network. Some of those nodes are defensible. Some are commoditising. Chapter VII will separate the two.

Market Sizing - Whose Number, Measuring What

Four credible research houses publish four different market sizes for this industry, and all four of them are correct. They are measuring different things. Before picking a name, an investor should know which slice that company actually sells into - because slice-level CAGR matters more than universe-level CAGR.

| Source | 2024 / Base | Terminal | CAGR | What It Measures |

|---|---|---|---|---|

| Verified Market Reports | $18.35B (2024) | $37.82B (2033) | 8.6% | Optical networking equipment & services |

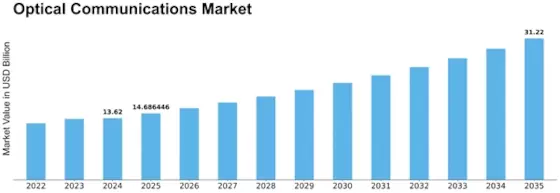

| Market Research Future | $13.62B (2024) | $31.22B (2035) | 7.83% | Optical comms gear; NA 40% / EU 30% / APAC 25% |

| IDTechEx - PICs | ~$5B (2025) | ~$50B (2036) | 21.9% | Photonic integrated circuits - the chip layer |

| IDTechEx - CPO | <$1B (2025) | Material by 2030 | ~50% | Co-packaged optics specifically |

| Maximize Market Research | $836.6B (2025) | $1.35T (2032) | 7.1% | Entire photonics universe (industrial, medical, lidar, AI, display) |

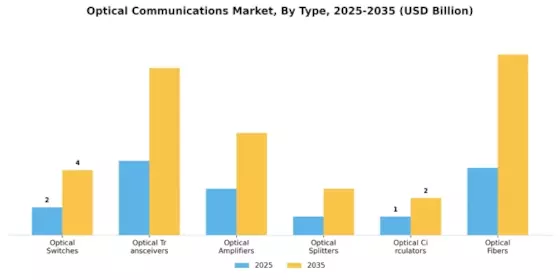

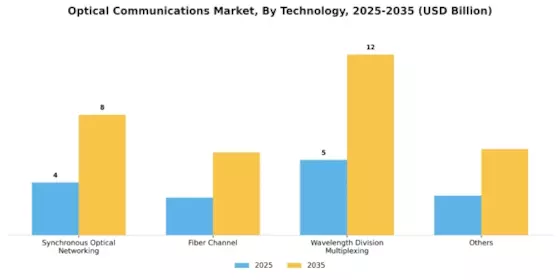

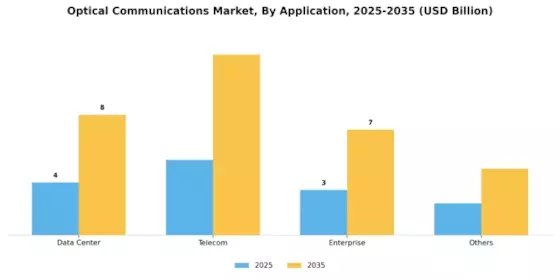

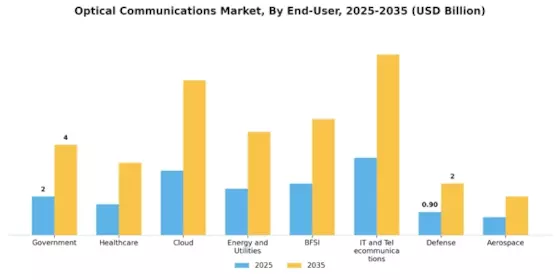

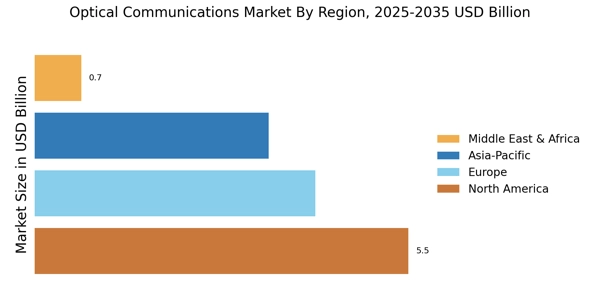

Market Research Future's dataset is worth spending time with, because it is the most granular of the optical-communications estimates and it breaks its market out along axes that actually matter for picking stocks - product type, underlying technology, end application, geography. Next six charts come straight out of that study, and each one tells an investor something useful about where inside this market the money flows.

A pattern holds across these six charts - the same shape every mature infrastructure market eventually shows. A large, slow base growing at mid-to-high single digits, with a narrow fast-growing segment inside it absorbing a disproportionate share of incremental dollars. An investor's job is to figure out which companies actually sell into that narrow fast segment versus which ones are just reported as being in the broader market. A 7.8% broad-industry CAGR and a 50% CPO CAGR describe the same universe. They do not describe the same investment.

That is the frame for everything that follows. When I talk about core long exposure later, I mean companies whose revenue mix tilts heavily to the narrow-fast slice - datacom transceivers, laser chips, CPO-ready modulators, AI-grade specialty fibre. When I talk about defensive exposure, I mean companies whose revenue mix is skewed to the slow-base - backbone switches, telecom fibre, carrier equipment. Both can be good businesses. They do not deserve the same multiple.

1.6T Race and CPO Question

Here is the single most important near-term question for this industry, and analysts are genuinely split on it. Does a 1.6T transition get solved with pluggable optics, a traditional transceiver form factor, or with co-packaged optics, where lasers sit directly on the switch ASIC?

Both are defensible. Nobody knows which is right yet.

My read. Pluggables dominate 2026 and most of 2027 because the install base is built for them, LPO extends their useful life, and the repair model matters. CPO takes material share from 2028 onward - not 80%, not even 50%, but probably 25-35% by 2030 in the highest-bandwidth tier. Both matter. Winners in each are different companies. Lumentum and Coherent benefit from both because they sell the underlying lasers into either architecture. Applied Optoelectronics is much more levered to pluggables - a feature or a bug depending on your time horizon.

Nvidia's $6 Billion Tell

In March 2026, Nvidia quietly did something that told you everything about where its priorities sit. Across a three-week span, it announced or confirmed roughly $6 billion of investment, partnership, and supply commitments into the optical layer. $2B into LITE, $2B into COHR, plus further ecosystem cheques - Marvell co-development, Celestica manufacturing capacity, a specialty-fibre roadmap alignment with Corning.

Not a hedge. A signal. Nvidia does not write $2 billion cheques to nice-to-haves. This is for companies sitting in the critical path of its next three product generations. Implicit message to the Street: we are supply-constrained on optics, and we are willing to use our balance sheet to fix that now, before the competition figures out what is about to happen.

"Datacom transceiver demand is the strongest we have seen in the company's history. We are running the InP fab at full utilisation and accelerating the capacity ramp."- Jim Anderson, Chief Executive Officer, Coherent Corp., Q4 FY2025 earnings call (sector commentary informed by Seeking Alpha and MarketBeat coverage)

Lumentum's guidance tells the same story. Roughly 77% FY26 revenue growth year over year, driven almost entirely by cloud and AI transceiver demand plus the Optical Circuit Switch product that slots directly into Nvidia's NVL72 reference architecture. Lumentum's 2023 CloudLight integration is paying off exactly as planned - more than paid for by a single product cycle.

And Applied Optoelectronics. A smaller, higher-beta name in this group, which confirmed a fresh $53 million hyperscale order on the same morning its sector sold off 14%. AAOI's pivot toward Linear Pluggable Optics has won it significant Microsoft volume, and Goldman's projection of 119% sales growth is the kind of number that, if it prints, retroactively justifies almost any entry point from here. If it does not print, that 14% single-day drawdown will look like a warm-up act.

What Institutions Are Actually Saying

| Name | Ticker | Desk View | Thesis in One Line |

|---|---|---|---|

| Coherent | COHR | Core Long | ~25% InP laser share. Indispensable. P/E 300+ today; cheap in hindsight if 1.6T ramp prints. |

| Lumentum | LITE | Core Long | FY26 revenue +77%. OCS is a direct Nvidia ride. Highest-conviction optics name on the sheet. |

| Marvell Technology | MRVL | Value Leg | Forward PEG ~0.7; $94B TAM with CPO + custom AI silicon. Cheapest way into both trades. |

| Corning | GLW | Defensive | Meta $6B multi-year contract. "Springboard" initiative. Lower beta, lower ceiling, materially lower floor. |

| Ciena | CIEN | Defensive | Backlog $7B, +45% YoY. Tailwind from AT&T's $250B, 5-year infrastructure programme. |

| Applied Optoelectronics | AAOI | High Beta | LPO ramp with Microsoft. 119% sales growth projected (Goldman). Wildcard - print or bust. |

| Fabrinet | FN | Supporting | The "TSMC of optical components." Precision contract manufacturer, benefits regardless of module winner. |

| Tower Semiconductor | TSEM | Supporting | Silicon photonics foundry - the upstream chip layer. |

| Nova | NVMI | Supporting | $514 / $881M 2025 revenue / +31%. PIC metrology - you can't yield a chip you can't measure. |

| IPG / nLight / MACOM | IPGP / LASR / MTSI | Supporting | Laser, photodetector, RF/mixed-signal specialists. Pull-through when primary names run out of capacity. |

What is useful about the current research cycle is that the sell-side has finally started publishing specific, attributable price targets - not just sector views - across the photonics basket. A few of the more-quoted calls, with attribution:

| Analyst / House | Ticker | Call | What They Said |

|---|---|---|---|

| Karl Ackerman BNP Paribas |

LITE | Buy - $1,040 PT | Late-March price target implies ~26% upside from an April 2 print near $827. Tied to the Optical Circuit Switch product slotting directly into Nvidia's NVL72 reference architecture. |

| Dan Buckley DayTrading.com (Chief Analyst) |

LITE COHR | Constructive | "Laser photonic technology matters right now because AI infrastructure is hitting what some in the industry call the 'Copper Wall.' Lasers through fibre can resolve that bottleneck by delivering more data at lower power consumption." Names Coherent's ~25% optical-transceiver share and the Nvidia $2B private placement as the structural bet. |

| Tore Svanberg Stifel |

MTSI | Buy - $255 PT (raised from $215) | Reiterated in mid-March. MACOM flagged as the hybrid semiconductor-photonics play tied directly to silicon photonics scale-up. |

| Gregory Shahnovsky Modcon Systems (CEO) |

Sector | Structural | "The broader investment case for laser photonics is strongly linked to its expanding role in high-value sectors such as energy, semiconductors, advanced manufacturing and environmental monitoring." Key point for investors: optics is not only an AI story. Industrial and sensing legs of the business compound independently. |

| Consensus Sell-side aggregate, per MarketBeat |

COHR | Buy (14 of 19) | Consensus PT $258.57 vs. current ~$327.37 - implying the Street is still catching up to the post-Nvidia re-rating. Revenue grew 17% YoY to $1.7B; EPS of $1.29 beat by $0.26. Next-quarter guide up to $1.84B, non-GAAP gross margin 38.5-40.5%. |

| Consensus Sell-side aggregate |

IPGP | Bullish - $148 PT (~30% upside) | "Picks and shovels" framing. Cyclical but diversified. Recent Düsseldorf AMB laser patent ruling against IPG is narrow - <1% of annual sales. |

| Consensus Sell-side aggregate |

LASR | Buy - $73 PT (~21% upside) | High-power semiconductor lasers for defense - directed-energy weapon and drone interception use cases. Locust laser system partnership with AeroVironment; beam-shaping deal with EOS metal AM systems. |

| Management guide Ciena Q1 FY26 |

CIEN | $5.9-6.3B FY26 rev guide | Analyst estimate $6.12B = 28% growth. Backlog compounding 45-46% YoY to ~$7B. Vesta 200 6.4T CPX (CPO-based) is a forward growth vector on top of the existing transceiver business. |

| Goldman Sachs Sector research |

AAOI | 119% sales growth projection | FY26 sales guide to $1B. Data centre segment expected to jump 3.6x to $700M. Customer concentration (Microsoft LPO, ramping Amazon) is the primary risk. |

| Management guide Marvell raised FY28 target |

MRVL | $15B FY28 revenue target | TAM expanded by 26% to $94B on custom-silicon + NVLink Fusion integration. Trades at 8.8x forward sales, 28x forward P/E, 0.7 forward PEG - unambiguously the cheap way into the story. |

Two things jump out of that matrix. First, price-target dispersion is still wide. Coherent trades above consensus PT because analysts have not yet caught up to a Nvidia-era earnings trajectory, while Ciena and AAOI have room to run before hitting their consensus ceilings. That dispersion is a signal of an industry in transition: sell-side models are still catching up to a re-architecting of the AI stack that happened faster than their research cycles. Second, every one of these analysts is framing the call around a physical constraint... Copper Wall, 200G-per-lane barrier, InP capacity ramp, CPO integration timeline...rather than around broad AI-TAM arithmetic. That is the tell of a sector being priced on engineering reality, not on narrative.

"Computing has fundamentally changed. In the age of AI, software runs on intelligence with tokens generated in real time by AI factories for every interaction and every context. With Coherent, Nvidia is pioneering next-generation silicon photonics to enable AI infrastructure at unprecedented scale, speed and energy efficiency."- Jensen Huang, Founder and CEO, Nvidia Corporation, announcing the $2B strategic investment in Coherent (March 2026)

One other name keeps showing up in research notes, and rarely in AI-infrastructure headlines, Nova Ltd. (NVMI). Nova is a PIC metrology company. It does not make chips. It measures them. And if you cannot measure a chip, you cannot yield it. Revenue is $881M run-rate on a 2025 quarter that printed $514M per-quarter, trading at 64x P/E against a $442 consensus PT vs. a current ~$514 print. Adjacent to this story in exactly the way ASML was adjacent to the semiconductor cycle a decade ago, highest-quality pick-and-shovel play on a manufacturing bottleneck every chipmaker in this industry has to solve. Worth knowing about, whether you buy it or not.

March 30th Sell-Off - What It Actually Meant

Three weeks ago, the sector gave back a meaningful chunk of its year-to-date run in a single session. AAOI -14.2%. LITE -9.4%. GLW -6.8%. Morning news was the opposite of bearish. AAOI had announced a $53 million hyperscale order, Nvidia had confirmed its strategic investments, 1.6T was on track. And yet tape still sold off. Why?

Two things were happening at once. First was generic. A broad semiconductor de-risking event driven by concern that AI capex might enter a short "digestion phase" between major product cycles. Any high-beta name got sold. Nvidia itself gave back several percent. Optics, being higher-beta than Nvidia, gave back more.

Second was specific. Optical names had, quite simply, run too far too fast. When a stock is up 1,500% in twelve months, even excellent fundamental news at a single company is not enough to sustain a multiple that assumes everything keeps breaking bullishly. Valuation starts to bite. You need not just good news but news better than what the multiple already prices in. A much higher bar.

My idea: March 30th action was just healthy correction. Not pleasant to be long through, but healthy. Comparable events happened in the 2021 run-up to the 400G transition - consolidations that felt terrible in the moment and look, in hindsight, like obvious buying opportunities. Key question is whether this consolidation is a 2021 analogue or something more sinister. I lean toward the former. If I am wrong, it is at this single hinge. If AI capex really is entering a multi-quarter digestion phase, the optical names will underperform for longer than most holders are positioned for.

Quality Compounders vs. Wave-Riders

This section matters most for capital allocation. An industry in a structural wave lifts almost every ticker inside it. That is obviously what has happened in optical networking over the last twelve months - Lumentum +1,575%, Daehan Optical +3,517%, Coherent +67%. But a wave eventually recedes, and when it does, the companies that were carried by the tide get handed back to earth while the companies with genuine structural moats keep compounding. Separating the two requires looking past the returns and into the business models.

My framework uses three tiers. Quality compounders are companies whose competitive position is defensible independent of the current AI capex cycle - irreplaceable supply, vertical integration, decade-plus customer relationships, proprietary technology that takes years to replicate. Hybrids are companies with real business quality but where the current valuation has been pulled forward by the wave and requires flawless execution to sustain. Wave-riders are companies with credible near-term demand but thinner moats - customer concentration, narrower product, higher execution risk - that are benefiting disproportionately from tide conditions. None of the three is a recommendation to buy or avoid on its own; they are three different return profiles that an investor should allocate differently.

Coherent. ~25% share of the optical-transceiver market, vertically integrated InP supply (the raw material for the laser chips), 2x capacity expansion in FY26 with another 2x planned for FY27. A 20-year relationship with Nvidia. This is the optical-networking name most analogous to TSMC in semiconductors - the one the whole industry actively needs to exist.

Lumentum. CloudLight integration paid off exactly as planned. EML chips already inside Nvidia's Quantum-X800 and Spectrum-X800 Photonics switches. Optical Circuit Switch product slotting directly into the NVL72 reference architecture. 77% FY26 revenue growth is not hype - it is backlog conversion. Added to the S&P 500 in March.

Corning. Dominant global fibre producer. Meta contract (~$6B multi-year) is the kind of specialty-fibre deal other manufacturers physically cannot service. Lower beta than the transceiver names, but backed by an irreplaceable production base.

Marvell. TAM expanded 26% to $94B on NVLink Fusion integration. $15B FY28 revenue target implying ~35% growth. 0.7 forward PEG ratio. Cheapest quality name in the group.

Nova. PIC metrology. Pick-and-shovel play on a manufacturing bottleneck - if PIC output doubles industry-wide, Nova sells more measurement tools regardless of which module maker wins.

Ciena. Backlog compounding 45-46% YoY to ~$7B. Vesta 200 6.4T CPX as a forward CPO vector. But the stock trades at 10x forward sales and 73x forward earnings - the richest valuation of the group relative to forward growth. Business is good. Entry point matters.

Fabrinet. "The TSMC of optical components." Precision contract manufacturer, benefits regardless of which module design wins. Quality business; valuation has tracked the basket up.

MACOM. Hybrid semiconductor-photonics play. Stifel's $255 target (raised from $215) reflects the structural read. Stock up ~130% trailing twelve months and ~39% YTD. Real story; re-rating largely complete.

Tower Semiconductor. Silicon photonics foundry - the upstream chip layer. Defensive moat; customer concentration in the foundry layer creates incremental execution risk.

Applied Optoelectronics. Most interesting of the wave-riders. Vertically integrated, LPO pivot winning Microsoft volume, and a fresh $53M hyperscale order. But customer concentration is real - this stock moves on single-quarter data-centre shipments - and Goldman's 119% growth projection either prints or it does not. That -14.2% single-session move on March 30th is the risk profile in one line.

nLight. Defence-laser exposure via AeroVironment's Locust system and directed-energy programmes. A credible niche, but the moat is smaller than the quality tier; the 60% YTD move is earned by catalysts, not by compounding fundamentals.

IPG Photonics. Industrial fiber lasers. Genuinely a picks-and-shovels play, but the Düsseldorf AMB patent ruling is a reminder that the industrial-laser market is competitive and contested. Consensus $148 PT (~30% upside) gets earned in an industrial recovery; it is not AI-levered.

Daehan Optical (KOSDAQ). A +3,517% return is the industry's most extreme wave-rider story. A Korean lens and optical-component maker re-rated almost entirely on AI-adjacency narrative. Western investors have no direct vehicle; worth knowing only as a leading indicator of sentiment extremity in the basket.

Practical allocation implication is that these three tiers belong in different portfolio buckets. Tier 1 gets core weight because those positions are owned for multi-year compounding through a full cycle. Tier 2 gets opportunistic weight, sized on entry discipline - names to add on a de-rating event, not on a single-session rally. Tier 3 gets tactical weight only - positions correctly sized at a fraction of what you would put into Tier 1, because payoff distribution is binary and downside from any execution miss is severe. An equal-weight basket across all three tiers would be mechanically lazy. Right exposure is heavily skewed to Tier 1, lightly spiced with Tier 2, and only a small allocation to Tier 3 - sized to whatever risk budget an investor is willing to burn.

Is Hype Sustainable

For an industry study on a sector that has moved this far, this fast, only one question really matters...is what markets are pricing in structural reality, or narrative momentum? Below are seven tests I use to judge whether this photonics re-rating survives twelve to twenty-four months, scored honestly against evidence as it stands today.

Five yes, two mixed. That is an honest scorecard. Photonics sits on genuine engineering drivers, real capital commitment, and tight supply. Two mixed lines are both about risk concentration - customer-side (hyperscaler dependency) and valuation-side (multiple compression). An investor can build a durable multi-year thesis on the yes columns. Mixed columns are why position sizing matters. They are not a reason to avoid this industry; they are a reason to allocate within it selectively.

A useful historical analogue is 2021's run-up into the 400G transition. Optical names ran, then consolidated hard through 2022 as hyperscaler capex paused, then resumed a structural climb once 800G established itself. That consolidation looked, at the time, like a thesis break. It was not. It was a pricing event. Same shape is highly plausible again between now and 2028. Structural story and share-price story are not the same story...investors who forget that get shaken out at exactly the wrong moment.

Analyst's Bottom Line

Photonics and optical networking are in the middle of a genuine structural re-plumbing of AI infrastructure. Copper cannot hit the bandwidth and thermal targets next-generation clusters require. Light can. Whoever supplies that light...indium phosphide laser chips, thin-film lithium niobate modulators, photonic integrated circuits, specialty fibre, co-packaged optics...is sitting on some of the tightest supply-demand dynamics in the whole semiconductor ecosystem. Call it the structural claim. Evidence backs it.

Valuations, though, have run ahead of cash flow across the basket. Call that the cyclical claim. Both can be true at the same time - and usually are, at the peak of a capex wave. For an investor looking at this sector today, the right question is not "is this real?" Evidence on that is clear enough. A sharper question is which companies are doing the compounding and which are being carried by the tide. That distinction is what Chapter VIII was built to answer.

AI infrastructure as a story has not ended. It is migrating down the stack - from compute, where Nvidia dominates, to interconnect, where a handful of specialised photonics companies dominate. Recognising that migration early is the analytical move. Separating quality compounders from wave-riders is the allocation move. Both are harder than recent tape has made them look, and both will matter more over the next twelve months than they did in the last twelve. That is the learning.

"Optical communications have already become a major trend in the AI industry. Nvidia's next-generation Spectrum-X network uses optical-communications technology to push beyond previous limits in data transmission and reception."- Industry coverage of Jensen Huang's GTC 2026 remarks, following Nvidia's identification of optical computing interconnects as core future technology

Research Desk, Bellwether Research, April 16, 2026