There's a number floating around the US financial system that the Federal Reserve can't see. Credit card issuers can't see it. Mortgage lenders, auto lenders, every consumer credit model in the country - blind to it. It is growing at 8.5% a year. It sits entirely outside traditional credit bureau reporting for a huge chunk of its transactions. And the people racking it up? They're simultaneously carrying credit card debt, auto loans, and student loans that those other creditors also cannot fully see.

That number is the outstanding balance of Buy Now, Pay Later loans. The BNPL market hit $122 billion in US transaction volume in 2025, used by over 86 million Americans. The pitch to consumers is financial freedom - split any purchase into four easy payments, zero interest, approved in seconds. What it actually represents, increasingly, is a shadow credit layer that systematically blinds the financial system to how stretched the American consumer really is.

I've pulled data from Forbes, the Federal Reserve, LendingTree, Motley Fool, Consumer Edge, Bank of America Global Research, and CB Insights research for this piece. The goal is an honest picture of what BNPL is doing to the economy - and what it means for investors sitting on both sides of the ledger.

The Hidden Debt Layer

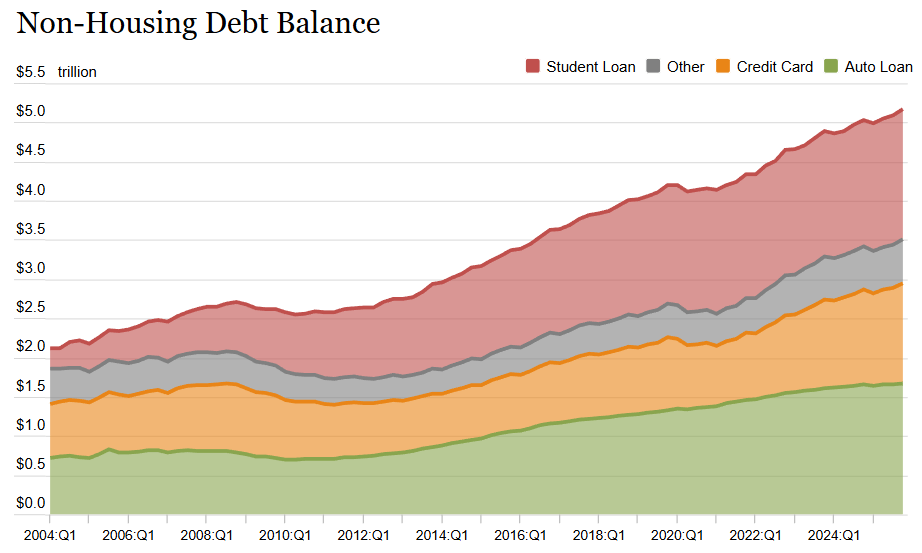

Start with the consumer debt picture most investors rely on. The chart below - from the New York Federal Reserve - shows the full stack of non-housing consumer debt in the United States: credit cards pushing toward $1.23 trillion, auto loans, student debt, and that residual "other" category that has crept steadily upward since 2004. Useful snapshot of consumer leverage. But it's incomplete in a way that wasn't true five years ago.

BNPL balances are largely missing from this picture. Credit bureaus have historically gotten little or no reporting from major BNPL providers. The three big US bureaus - Equifax, Experian, and TransUnion - only recently started receiving data from some providers, and even now the coverage has gaps you could drive a truck through. CB Insights research estimates total consumer debt figures are understated by at least 1% - roughly $40 billion - with BNPL balances growing at 8.5% annually. That hole is getting bigger, not smaller.

"BNPL is not simply another credit product competing with Visa and Mastercard. It is a parallel credit system with no shared information layer. Affirm does not know what you owe to Klarna. Klarna does not know what you owe to Afterpay. No single institution - not the banks, not the bureaus, not the regulators - can see the full picture. And consumers themselves increasingly cannot either."

This sets up a dynamic that echoes - in structure if not yet in scale - the pre-2008 mortgage market. A product being extended to consumers whose true total obligations are systematically hidden from each individual lender. Some BNPL firms argue that reporting would actually hurt their customers' credit scores, that bureau models are calibrated for conventional revolving credit and would overpenalize the frequent short-term loans BNPL involves. And frankly, there's some validity to that concern. But it is also, conveniently, an argument that shields the business model by keeping competitors from seeing borrower quality. Funny how that works.

Who Is Actually Using This - And How Often

The easy narrative says BNPL is basically a tool of the financially desperate - young consumers who can't get a credit card, subprime borrowers stretching for things they can't afford. Partially true. But the full picture is more systemic than that, and from a credit risk standpoint, considerably more unsettling.

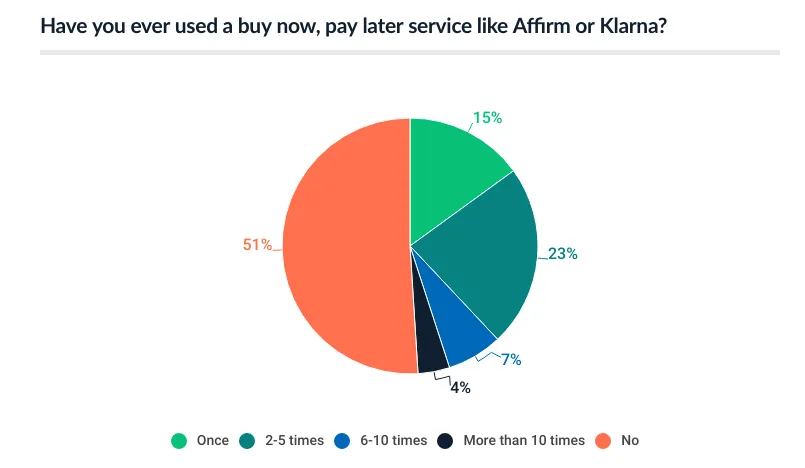

Almost half of Americans have used BNPL. About 10% qualify as power users - six or more active loan relationships. A 2025 Harris Poll for NerdWallet found 22% of consumers currently owe money to a BNPL provider, with 19% carrying multiple BNPL loans simultaneously over the prior twelve months. The New York Fed found 14% of adults used BNPL in 2022; the Philadelphia Fed found 20% by 2023. Usage is growing faster than the surveys can keep up with.

And here's what jumped out at me: the consumer base isn't confined to the financially marginal. As CB Insights research puts it - when something turns sour in the credit system, it needs to affect the middle class to matter. (See mortgages in the Great Financial Crisis.) BNPL usage spans all income cohorts on similar trajectories. Higher income shows slightly lower adoption, sure, but every band is growing. This is not a subprime problem. It is a structural credit system problem that happens to be most concentrated in lower-income cohorts.

The Global Context: America Is Behind the Curve

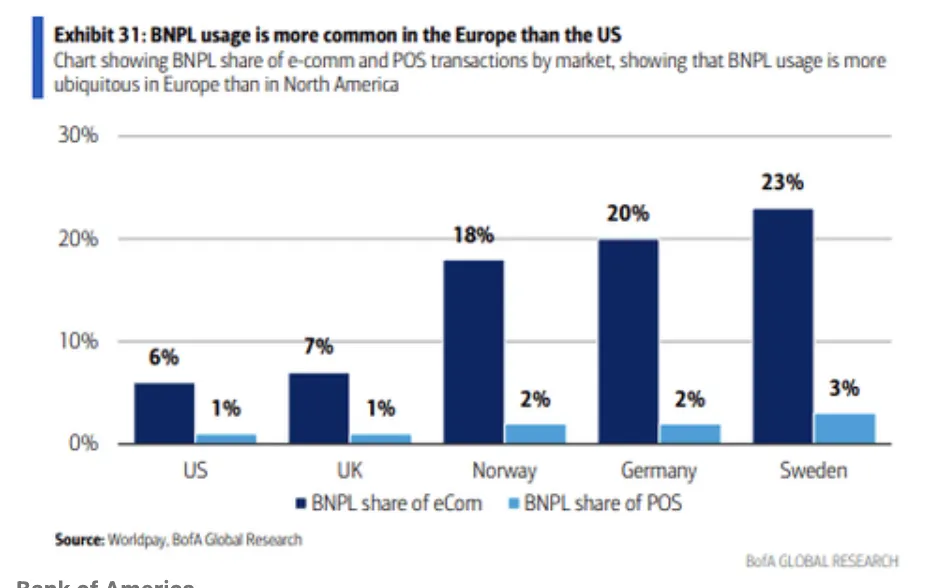

One thing that consistently surprises American readers: the United States is not where BNPL has dug deepest into the consumer economy. That would be Northern Europe, where the product has been normal for over a decade - and where the downstream consequences are now playing out in ways that should give US market observers serious pause.

Sweden, Klarna's home turf, has seen BNPL absorb 23% of e-commerce transactions. Germany sits at 20%. Norway at 18%. The UK - which shares more cultural and regulatory DNA with the US - is at 7% and climbing. The US, currently at 6-7.5% of e-commerce, is tracking the exact same adoption curve, roughly five to eight years behind Europe. So what happened in Sweden? Widespread use, rising consumer debt stress, and now increasing regulatory attention. The UK's Financial Conduct Authority has already moved to regulate BNPL. US regulatory structures are only just beginning to ask the same questions.

What Are They Actually Buying?

The spending mix tells you something crucial about the underlying economic reality here. If consumers were mainly using BNPL to finance aspirational stuff - luxury goods, electronics, holidays - the "convenience credit" story would hold up better. But that is not what the data shows.

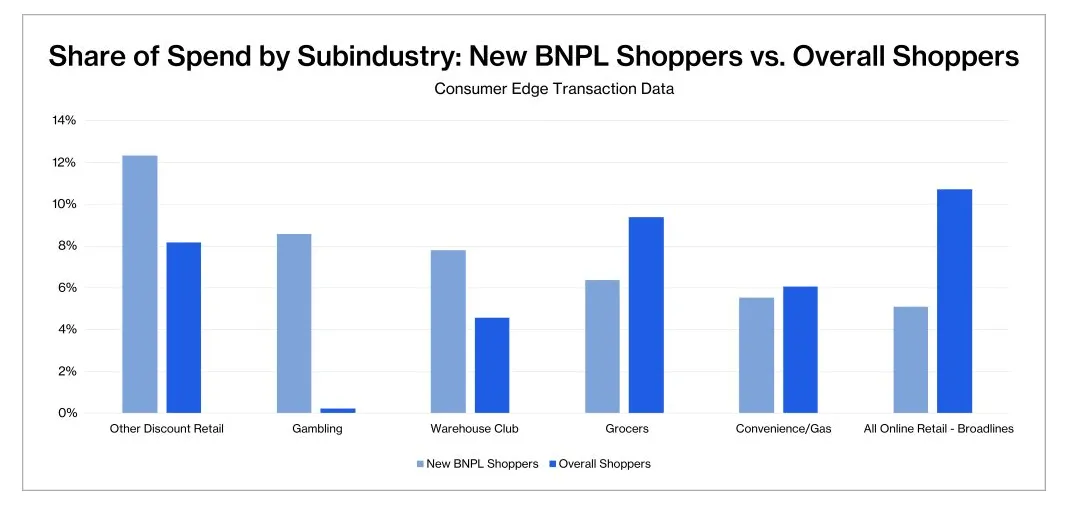

LendingTree data says a quarter of all BNPL spending goes to groceries, with food-related spending totalling roughly 54% of all BNPL transactions. Consumer Edge transaction data shows new BNPL shoppers dramatically over-indexing in discount retail (12% of spend vs 8% for overall shoppers) and warehouse clubs. Adobe estimates that the online value of BNPL loans during the Thanksgiving-to-Cyber Monday five-day window alone will top $20.2 billion - that's nearly 20% of the year's total - which tells you the product is deeply wired into essential and seasonal spending cycles. Not just discretionary luxuries.

Then there's the gambling category. I'll be blunt about it. BNPL shoppers spend a disproportionately large share at gambling platforms relative to the broader consumer population. This isn't incidental - it reflects a consumer profile comfortable with high-frequency, high-impulsivity spending decisions, often on borrowed money. For a meaningful subset of BNPL users, the product is literally providing gambling liquidity. That's not the kind of credit quality that builds sustainable repayment capacity.

The GDP Backstop Argument

There is a wholly valid counter-argument here. BNPL for groceries means people living paycheck-to-paycheck can go to the grocery store between pay cycles - when otherwise they might have to wait until payday. That is a real benefit for households with volatile income. The same argument applies to credit cards for consumers who pay on time. The question isn't whether BNPL provides value to some consumers - it clearly does. The question is whether the system-level risks created by opaque reporting are being adequately priced and regulated. Right now, the answer is no.

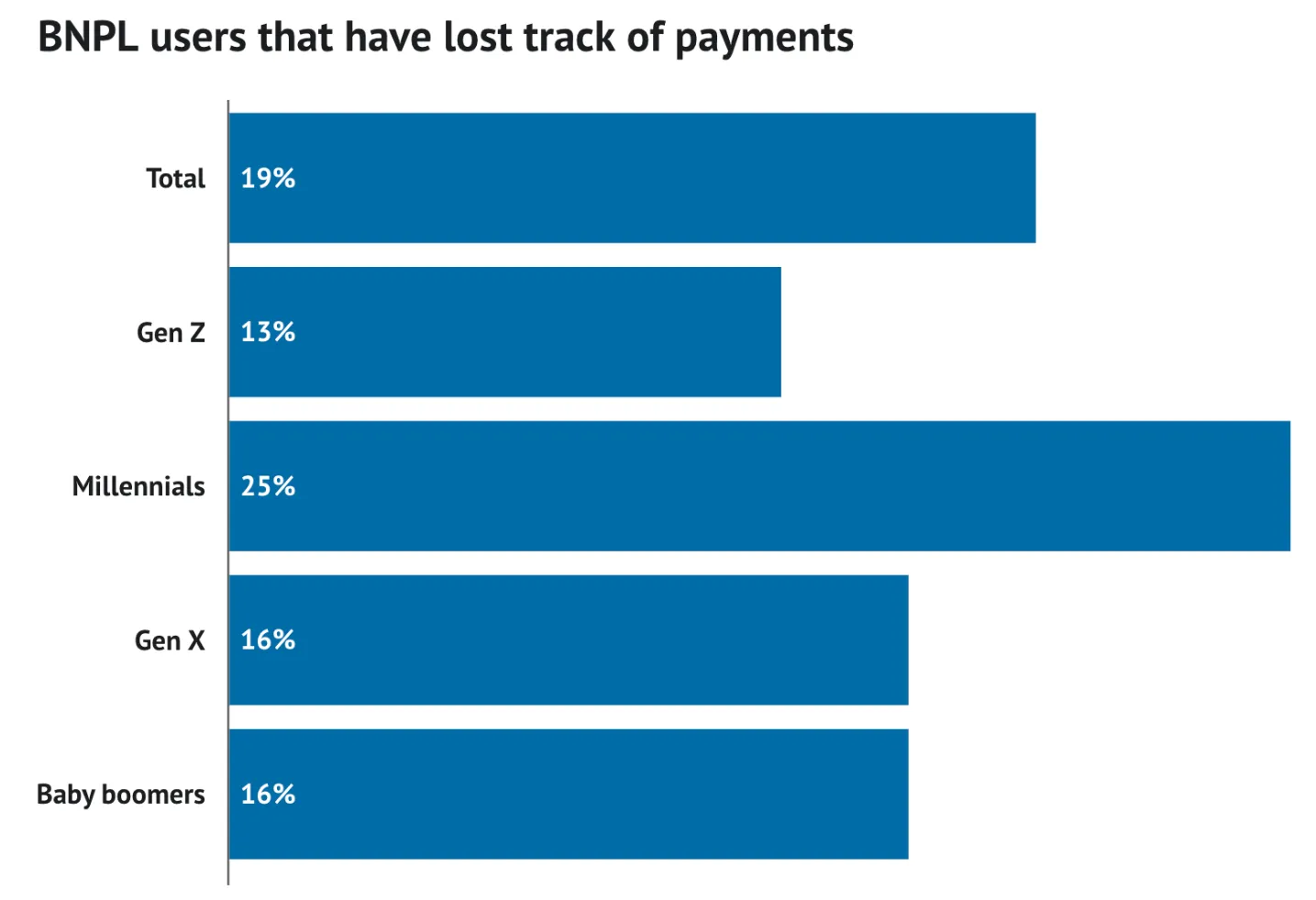

The Lost Track Problem

Here's a data point that should stop any analyst cold. No age cohort - not Gen Z, not Baby Boomers, not a single demographic segment surveyed - has below a 13% rate of having failed to keep track of all their BNPL payments. None of them.

Overall, 19% of BNPL users can't account for all their outstanding loans. Among Millennials - the cohort most tied to the product's mainstream adoption - that number climbs to 25%. A quarter of Millennial BNPL users do not know what they owe. That's not a typo.

And this isn't some failure of financial literacy, like the easy take would suggest. It is an architectural failure of the product itself. Think about it: a consumer who uses Affirm for electronics, Klarna for clothing, and Afterpay for travel is now managing three separate loan schedules, three payment calendars, three sets of terms - while none of those three providers can see the other two. Each provider's incentive is to approve the next transaction and collect the merchant fee. The incentive to actually understand total borrower obligations? Structurally subordinated to volume growth. Every time. This is how credit systems develop fragility at the margin - not through some dramatic blowup, but through a thousand small approvals that nobody is aggregating.

The Delinquency Picture

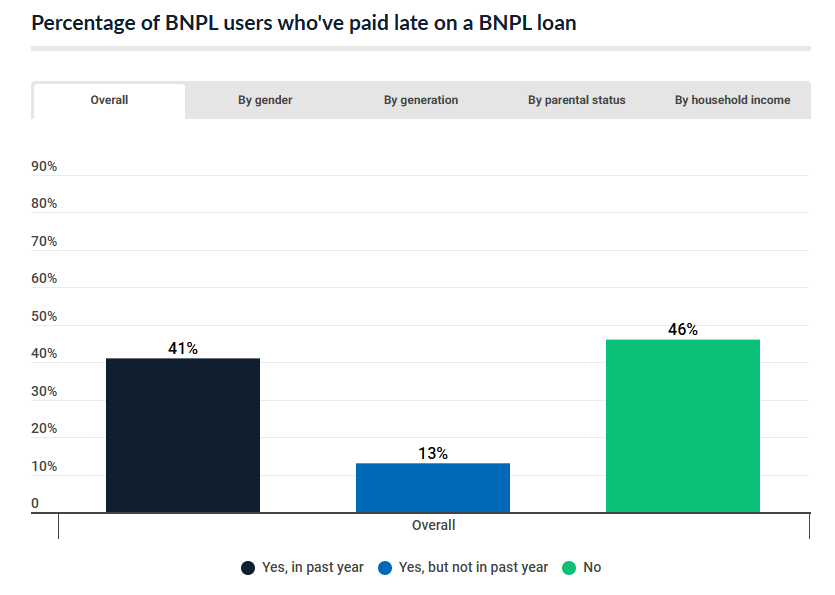

When 19% of users have lost track of their obligations, you'd expect late payment rates to be elevated. What I did not expect was how elevated. Or that the most financially stretched cohort wouldn't necessarily be where the headline numbers point.

LendingTree's April 2025 survey: 41% of all BNPL borrowers made late payments in the prior year. Among Gen Z, 57%. Among Millennials, 49%. The Federal Reserve Board, running its own separate analysis, pegged BNPL late payments at 24% - a figure that already spooked Federal Reserve Governor Michael Barr enough to label BNPL a "debt trap" at a July Fed conference on financial inclusion. "Delinquency rates have gone up to 25%," Barr said. "It's a growing area of concern and one we should all be paying attention to."

But here's something from the CB Insights analysis that complicates the simple narrative of BNPL as a subprime problem: high-income borrowers actually have a higher late payment rate relative to other income bands in some cohorts. Counterintuitive, right? It suggests that the behavioral dynamics of BNPL - the frictionless approval, the "buy now" impulse, the fragmented tracking mess - trip up affluent consumers too. If late payments were purely about affordability stress, you'd see a clean monotonic relationship between income and payment performance. The data does not consistently show that. Something else is going on.

Federal Reserve on Consumer Vulnerability

"Adults who report lower overall financial well-being and those who appear liquidity or credit constrained were among the most likely to use BNPL. Most of these consumers also indicated that they used BNPL because it was the only way they could afford to make the purchase." - Federal Reserve Board. The implication hits hard: a significant share of BNPL volume represents purchases that would not have happened without BNPL, made by consumers who could not have gotten them through conventional credit. That is, by definition, credit being extended to consumers at the margin of affordability.

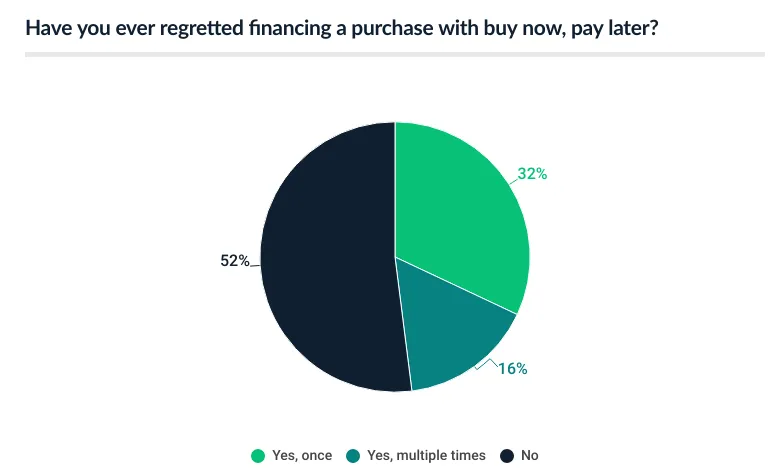

Regret and Buyer's Remorse

Beyond the delinquency numbers, there is a softer but analytically telling signal in how consumers feel about their BNPL usage after the fact.

48% of BNPL users have regretted at least one BNPL-financed purchase - 32% once, 16% multiple times. Nearly half the user base. That 16% who keep going back and regretting it again? Those are the habitual over-extenders - using easy credit to buy things that, on reflection, didn't represent genuine value. They're the ones most likely juggling multiple active loans, most likely to have lost track of their obligations, and most likely to miss payments the moment cash flow tightens.

A Bankrate survey found that among BNPL users who ran into problems: 25% said BNPL made them overspend, 16% missed a payment, 15% regretted the purchase, and 14% had difficulty making returns. And get this - PayPal reports that offering BNPL leads to a 91% higher average order value for retailers. Those two facts are directly connected. BNPL is remarkably effective at getting people to spend more. Whether those bigger purchases are genuinely affordable or just deferred regret is the whole question.

Regulatory Response: Too Little, Too Late?

The regulatory gap around BNPL has been an open secret for years. Until recently, BNPL existed as what some analysts called "phantom debt" - transacted, accumulated, defaulted on, all without touching any of the standard credit reporting infrastructure that the entire financial system depends on to price risk. That's started to change. Slowly. Incompletely.

The three major US credit bureaus have begun getting data from some leading providers, and the CFPB has stepped up its scrutiny of the sector. In a notable political signal, minority members of the Senate Banking Committee led by Senator Elizabeth Warren sent letters to seven leading BNPL providers demanding detailed data on their products, users, and economic role - explicitly citing concern about what the senators described as "opaque" BNPL products being used to pay for groceries and healthcare while the CFPB's enforcement priorities under the Trump administration have shifted away from consumer protection.

FICO Score 10: A Partial Response

In June 2025, FICO unveiled changes to its credit scoring models - FICO Score 10 now includes a BNPL component and tries to better capture signals of consumer behaviour by aggregating BNPL loans taken in quick succession. FICO says it worked with leaders in the BNPL industry to develop this. But: no specific provider names were confirmed, no widespread change in reporting volumes has gone public, and as of mid-2025, the majority of BNPL loans for most consumers are still not showing up in credit bureau data. A step in the right direction that does not yet touch the core structural problem.

The deeper challenge is this: BNPL firms have a commercial incentive that runs directly against comprehensive reporting. More complete reporting would expose their borrowers' total obligations to competing lenders - and vice versa - creating natural lending limits that would cut volume. Without regulatory mandates for comprehensive reporting, the industry's voluntary response will always be partial. (Why would it be otherwise?) The CFPB's current enforcement posture makes near-term mandatory reporting requirements unlikely. That protection gap is probably going to persist through at least 2026.

The Macroeconomic Implications

BNPL's relationship with the broader US economy is genuinely ambiguous. And I think that ambiguity deserves honest engagement rather than being shoved into either the bullish or bearish bucket prematurely.

The bull case for BNPL's economic function is real. Consumer spending runs approximately 70% of US GDP. Credit card rates are sitting between 18-30% for many borrowers. BNPL gives consumers cheaper access to credit that sustains consumption volumes which would otherwise contract - simple as that. PayPal reports a 91% higher average order value for retailers offering BNPL. Affirm, Klarna, and their peers collectively processed billions of transactions that expanded retail spending's reach to consumers who either lacked credit cards or wanted to avoid their interest rates. During a stretch of persistent inflation, this consumption support has arguably kept retail volumes higher than they'd otherwise be, contributing positively to GDP growth figures.

The bear case is equally grounded in evidence. Senator Warren's letter to BNPL providers noted that consumers with a BNPL loan had, on average, $871 more in credit card debt in the month of origination than a consumer of the same age and credit score who did not take a BNPL loan. So BNPL users are not replacing credit card debt - they are stacking on top of it. When retail sales appear "flat" or GDP consumption holds steady despite deteriorating consumer confidence data, how much of that stability is actually BNPL-financed spending masking genuine demand weakness? It's borrowed demand from the future. And the repayment schedule arrives whether or not economic conditions improve.

"The whole BNPL process has potential disaster written all over it. And that's for the retailers accepting BNPL and the consumers using it. Tempting consumers into financial trouble isn't a sustainable business model - it's a ticking time bomb."

- Warren Shoulberg, Industry AnalystInvestment Framework: The BNPL Sector

| Company / Exposure | Bull Case | Bear Case | Key Watch Metric |

|---|---|---|---|

| Affirm (AFRM) | Largest US pure-play; high merchant diversification; growing repeat usage | Charge-off rates sensitive to consumer stress; high cost of capital; no consistent profitability | Delinquency trends, GMV per user, funding costs |

| Klarna (KLAR) | European market dominance; IPO optionality; strong brand in younger demographics | European regulatory tightening; US market still unproven at scale; pricing pressure from incumbents | Active merchant count, credit loss provisions |

| PayPal (PYPL) | BNPL embedded in existing payment infrastructure; massive existing user base | BNPL is a small share of total revenue; competitive pressure from dedicated players; margin pressure | BNPL transaction share, take rate trends |

| Retail Sector (BNPL-reliant) | BNPL increases basket size and purchase completion; customer acquisition at no upfront cost | Higher merchant fees than card networks; customers with poorest long-term profiles; revenue at risk if BNPL tightens | BNPL as % of revenue, customer repeat rates |

| Credit Card Issuers | BNPL delinquency may drive card users back to traditional credit; issuers developing own BNPL products | BNPL balances invisible to card issuers when setting limits; spillover default risk; share loss | Card delinquencies, BNPL product launches |

| Consumer Staples / Discount Retail | BNPL for groceries signals structural shift toward value retailers benefiting from trading down | BNPL consumption is borrowed demand - when it unwinds, discount staples see it first | Same-store sales, traffic per cohort |

Our Conclusion: Lifeline, Liability, or Both?

Analytical Conclusion - August 2025

BNPL is neither the consumer empowerment tool its proponents sell nor the unambiguous debt trap its critics warn about. It sits in genuinely messy middle ground - a financial product that creates real value for some consumers while systematically building information asymmetries that make the broader credit system less safe for everyone.

The structural problem isn't the product itself. It's the reporting architecture. A world where Affirm, Klarna, Afterpay, and every credit card issuer could see a consumer's total BNPL obligations would be a world where credit is appropriately priced and extended. We do not live in that world. We live in one where consumers can stack loans across apps with no single institution seeing the full picture - and where FICO Score 10, while a positive development, hasn't yet produced the comprehensive reporting change the market actually needs.

From an investment standpoint, I approach BNPL-exposed firms with caution rather than enthusiasm. The 41% late payment rate in the past year is not a marginal signal - it is the majority of the borrower base experiencing payment stress. The fact that 25% of Millennials cannot account for what they owe is not a financial literacy failure. It is a product design consequence that will eventually show up in credit losses. The delinquency data already visible is almost certainly understated, because unreported loans that go bad simply vanish from the statistics without ever appearing as formal defaults.

The economy-level question - whether BNPL is propping up consumption that masks genuine demand weakness - doesn't have a clean answer yet. But when retail sales flatline, consumer confidence craters, and GDP consumption numbers remain weirdly resilient, the possibility that BNPL-financed spending is papering over weakness deserves serious weight. Watch Q4 2025 and Q1 2026 GDP consumption components carefully. If the unwinding of borrowed demand comes, it won't be gradual.

Bellwether Research, Research Team, August 21, 2025